DRI remains on our Investment Ideas list as a short.

Knapp Data Discouraging

Wednesday night, Malcolm Knapp released sales results for November, estimating that same-restaurant sales increased +0.3% as guest counts decreased -2.1% versus a year ago. On a two-year average basis, same-restaurant sales increased +0.9% as guest counts decreased -1.3%.

Importantly, November signified a period of widespread sequential declines in the restaurant industry, as both same-restaurant sales and guest counts declined -160 bps and -230 bps, respectively, on a sequential basis.

Recall that earlier this week we provided detail on November data from Black Box, which showed a similar pattern that of the Knapp estimates. Despite both sources suggesting sales increased as traffic decreased during the month, the Knapp data paints a gloomier picture of the industry.

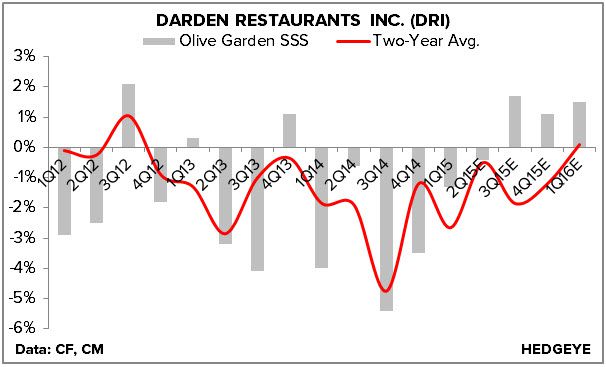

DRI Is a Short Into Earnings

To us, this suggests that Darden (which isn’t included in Black Box estimates) had a difficult November. With the company set to report earnings next Tuesday, December 16th, after the close, we find it prudent to reiterate our short as the recent move in the stock has been premature. Although there is a chance the company hits 2Q15 estimates, full-year expectations remain too aggressive and will likely be guided down at some point.

Our bearish bias is predicated on the struggling Olive Garden business, which the street assumes will recover quite nicely from an anemic FY14. Unfortunately, we haven’t seen anything would indicate a recovery is underway. The Brand Renaissance laid out by the prior management team was underwhelming and we expect the results moving forward to be a reflection of this.

We need to see management name a CEO and unveil a new strategic plan before we get excited about the Darden story moving forward. This plan would need to include the following:

- A new strategic direction for Olive Garden

- A plan to improve LongHorn’s relatively low AUVs and below average returns

- Significant changes to capital allocation strategies (limited new unit growth, potential sale of non-core assets/real estate, etc.)

- Strategic priorities for improving the entire cost structure of the enterprise

Darden’s stock price and valuation will be driven by the Olive Garden business in the future and, quite frankly, we don’t have much faith in management’s current plan to resurrect the brand.

The Street Is Blindly Assuming A 2H15 Recovery at og

Howard Penney

Managing Director

Fred Masotta

Analyst