Conclusion: We’ll take the market reaction, but this was actually a really lousy quarter – especially considering the pain it is lapping vs last year. The irony is that victory can be achieved by simply running this company like how it should be – not what it was built to be. The management team that exists today can likely never earn over $2.50 without a lot of luck. We think that the Board dynamics are such that the pending CFO hire will be a game changer, raising the profile of the Finance Organization at LULU – even if it means eventually getting rid of the ‘new’ CEO. That’s when we can talk about $3-4 in earnings and a $100+ stock. We’re still Long, but with a short leash.

FULL DETAILS

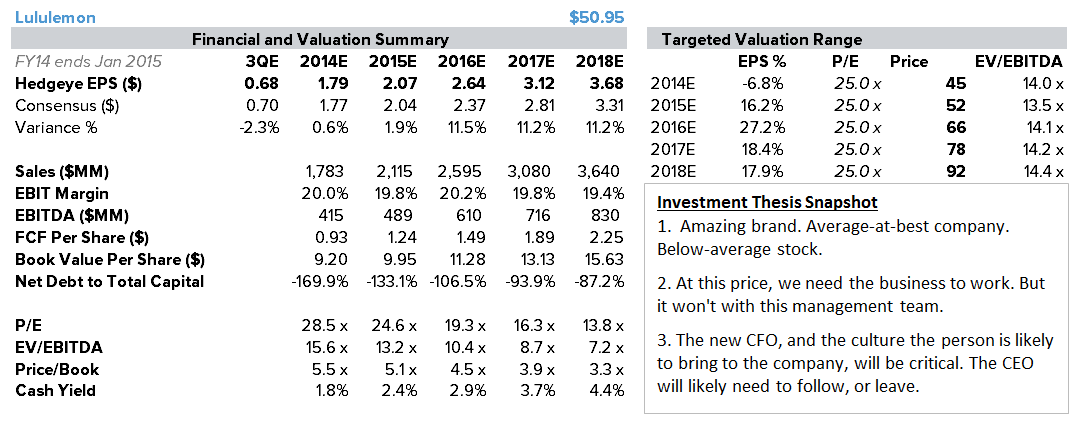

We’re not as excited about this LULU print as the market is. Don’t get us wrong – we’ll take the upside, as the name has been on our Best Ideas list on the Long side since June 15 of this year. And for now it’s staying there. But let’s face reality – the stock was up because business is ‘less pathetic’ than it had been. Comps were +3.0% (Constant $), new store productivity was stable at 63%, and revenue was +10.4%. That’s all good. But from that point, the growth algorithm pulls a sharp 180. Gross profit was up only +3.2%, and EBIT was down -12.1%, and EPS off by -6.9%. Can we celebrate progress? Yes. But make no mistake, the financial model remains broken.

A few more thoughts on the print.

1. Why Aren’t Numbers Better, Sooner? We’re seven quarters removed from the Luon (see thru pants) debacle, and 4 quarters removed from the last of the ensuing PR problems that plagued the company. Numbers should, without fail, be getting better.

2. Questionable Risk Management. The West Coast port issues have been lingering in the news since July, yet this is the first consumer company we heard that actually adjusted revenue guidance because of inventory delays at the ports. Either it has very poor risk management processes to divert freight away from Long Beach, or it simply planned very poorly. We’d argue that it is both as a) this is not a process-driven company that places a priority on risk management, and b) with all the new employees hired in product planning over the past quarter, LULU simply didn’t have enough people in place when it mattered (that’s likely why they hired).

3. We’re mixed on the Gross Margin erosion (-353bps). When all is said and done, we think that LULU will be sitting here in 2-3 years with a 48% Gross Margin vs 51% today. It can either get there offensively, or defensively. We prefer offense.

a. Offense means that the company invests proactively in its R&D platform and innovation agenda, its ability to flow product more accurately throughout a multi-channel distribution platform, while maintaining price integrity, and its premium brand status. It accelerates sales at a premium merchandise margin, but does so through appropriately investing in the areas needed to win (like Nike and UnderArmour).

b. Defense means the exact opposite. It means that the company does not have the product engine to grow the brand, nor can it flow product down the price curve as a season progresses through an increasingly unmanageable number of doors. The best example of this is Coach. The company has been married to its Gross Margin for so long, and it ultimately cost Coach’s top line all hope of doing anything other than going straight down. When Laurent talks about returning to a mid-50s GM% on the conference call, we wish he could see half of his investor base grimace. Our strong sense on this one is that nobody will pay for Gross Margin improvement. They will pay for sheer growth – even if it comes at a lower gross margin than what the company is churning out today.

4. Still no convincing plan to fix the company. That’s actually one of the things that attracts us to the story. The brand, despite its problems, remains very relevant. As hard as Chip’s organization seemingly tried, it did not kill the brand. There is almost zero chance that there is a well-articulated plan internally that we’re simply not hearing. Trust me, if Laurent had rock solid strategic and financial models, we’d know about them. You don’t let your CFO go (or push him out) because ‘the financial model is just too good’. When JC Penney has articulated a better growth plan than you, then you should probably rethink a few things.

That Brings Us to Why We Still Like LULU.

No, we don’t like the lack of a financial model, we didn’t like the growth algorithm, or the inability of the company to accelerate growth at the precise time when it is anniversarying problems from last year. In sum, we simply don’t like management. They’re nice people, but we think that Potdevin (CEO) is punching far above his weight. This was Currie’s (CFO) last conference call, and it sounds like a new CFO will be on the next call. We almost never get too upbeat about a single individual in an organization. But we think that this role is the exception. Why?

For starters, the Finance function at LULU has always been extremely weak. Currie was appropriate to be Chip’s numbers guy in the early days of the company, but Chip purposely kept the entire function at bay as the company grew up, as he thought it would hurt the culture of the company.

At the same time, the Chairman of the Board is now split between Mike Casey (former CFO of Starbucks) and David Mussafer (Advent/new to the Board). The new CFO will not be hired by Laurent, he/she will be hired by Casey and Mussafer, who both know the caliber of person needed to get this company back on track. Our sense is that this person will be tasked with rightsizing the company. If Laurent wants to follow, then great. Everyone wins. But if he resists, then the new CEO will soon be the old CEO.

So What Does this Mean for the Stock?

The risk/reward definitely is not what it was 35% ago. LBO is off the table at this valuation, as is a sale of the company. Now we have to bet on an actual rebound in the business. If we had to make that bet on the team that’s in place today, it’s pretty clear that they’d get a vote of no-confidence, and we’d be out. At a price, we’d actually go the other way and short the stock.

But, we’re very interested to see the caliber of the individual that the company hires. It’s odd…in our conversations with investors, people agree that Currie had to go, but don’t necessarily think that there’s a problem with the finance organization being so weak at LULU. We think that people will only realize how problematic this has been once it is fixed.

There’s a lot of extremely competent leaders out there in or around retail finance that have proven that they can run businesses far bigger than LULU. Consider Nike, for example – which is a mere 300 miles South of LULU. It has at least eight divisional CFOs who run businesses at least 2x as big as LULU (and Nike North America is over 10x). The point is that the talent is out there, and our sense is that Casey and Mussafer are taking their time for a reason. This hire could be a game changer.

It will be painful along the way, but how we’re modeling it, we get to a 20% EPS CAGR, and earnings back above $3.00 by FY17. The stock is trading at about 24x next year’s number ($2.17), and if we hold that multiple – which is not a ridiculous assumption given accelerating growth to 20%, then we’re looking at $64 and $75 1 and 2-years out, respectively. Not a huge return, but we’ll take it.