Updated levels (BEARISH TREND/TAIL)

TRADE DURATION RISK RANGE: $60.48-$65.38

TREND RESISTANCE: $83.83

TAIL RESISTANCE: $92.97

After the Thanksgiving frenzy, the market failed to recover any ground last week. WTI finished down 80bps, and the selling has continued this week:

- BRENT -6.4% WTD

- WTI -6.9% WTD

Now the question becomes when will the wave of downwardly revised cap-ex plans in the E&P space for 2015 hitting the tape from Halcon, Continental, Conoco Phillips, Miller, Oasis Petroleum, etc. provide support for prices? If you’re a small-cap, over-leveraged E&P company, your cap-ex plans were predicated on the existence of the cheap funding in capital markets that has existed over the last several years in the energy space.

The shale surge has been unarguably fueled by cheap access to capital markets, and this source of leverage is now much more costly. High yield spreads in the energy space are touching record levels above 9%. We outlined the spread risk in the high yield space in our Q4 macro themes deck. Feel free to reach out for access or have a look at Darius Dale’s Macro Playbook from this morning.

With debt capital markets virtually un-accessible as of today, the sell-off in small and mid-cap E&Ps also crushes capital raising alternatives on the equity side (shareholder dilution constant). The small/mid-cap wildcatter's E&P index is down ~-60% from its June 2014 highs.

The cap-ex slowdown will eventually flow through to actual production numbers, but it won’t happen until your book is closed for 2014.

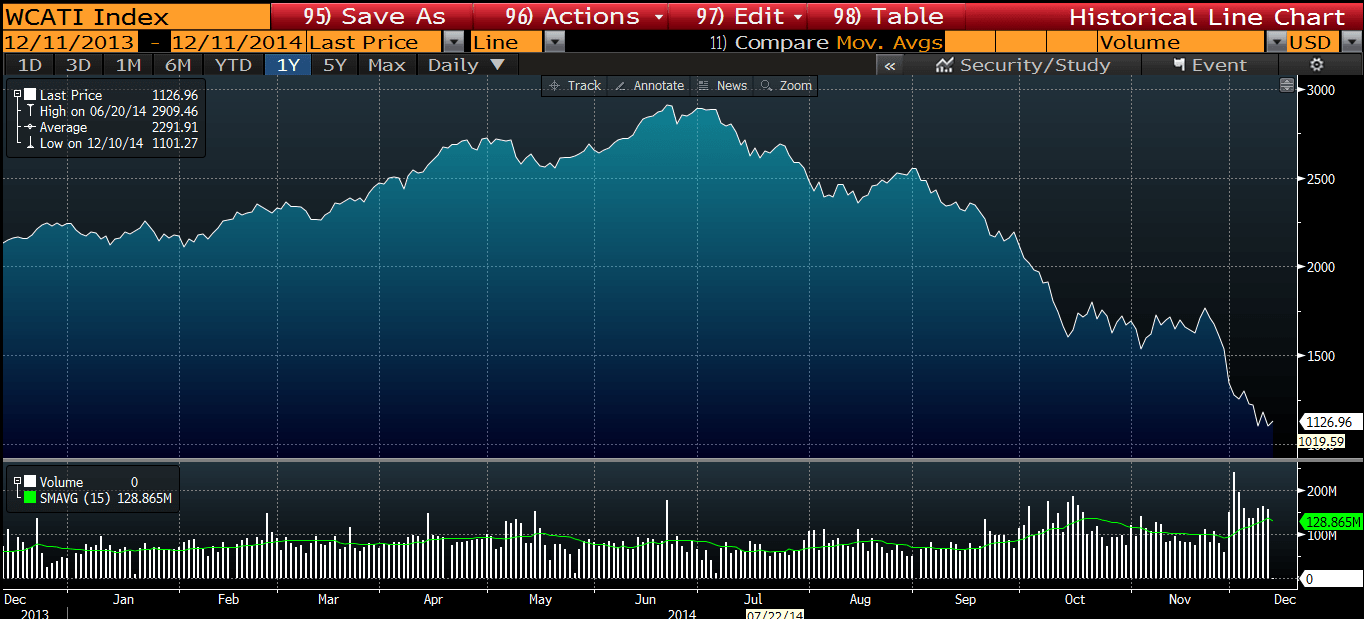

Over the short-term, our process for contextualizing daily market activity continues to indicate there is a risk of further downside into year-end. WTI and BRENT finished sharply lower yesterday with the kind of momentum we would want to observe as an indicator for more downside:

- Price: -4.0%

- Volume: +35/+27/+19/+28% above 5-day/1/3/6-month averages

- Open Interest (short-term indicator): higher vs 5-day and 1-month averages

- Implied Volatility in spot contracts: +7/15/32/69% above those same durtations

While we have been in front of the downside risk in oil in Q4, the expectation for lower prices (from here) is certainly becoming a psychological and consensus expectation, which we will fade when the time comes. The expectation for future volatility is blown-out. The commitments of traders report from the CFTC shows that the sum of aggregate positions in futures and options markets is between 1-2 standard deviations shorter than it has been over the last year. As a contra-indicator should work, the longest market positioning of 2014 was at the June highs in WTI.

We have a simple back-test model that tracks 60-day price performance in oil markets once contract positioning becomes +/- 1 standard deviation extended over different trailing durations. The result is that market positioning that chases price is a very obvious indicator to fade.

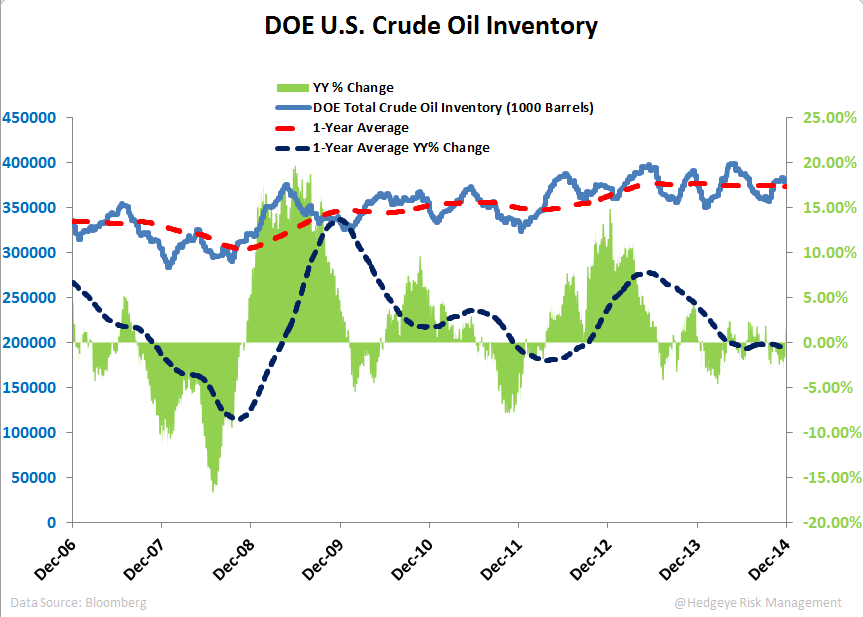

The psychological consensus bias towards lower oil prices from here can be observed in fundamental-form with the release of DOE oil and gas inventory data yesterday which surprised to the upside sending energy prices lower:

- DOE U.S. crude oil inventories 1454K vs. -3689K prior (-2625K estimated)

- DOE Cushing, OK Crude Inventories 1020K vs. -694K estimated

- DOE Gasoline Inventory 8197K vs. 2141K prior (2450K estimated)

With so much attention on the sell-off in energy, the event of this weekly DOE stockpile release has induced volatile market activity followed by the narrative of global "OVERSUPPLY." In reality, aggregate crude oil inventories in the United States have been constant over the last year. DOE inventory data also has no real credibility as a directional indicator that we know of. On a y/y delta basis, crude inventories have actually declined.

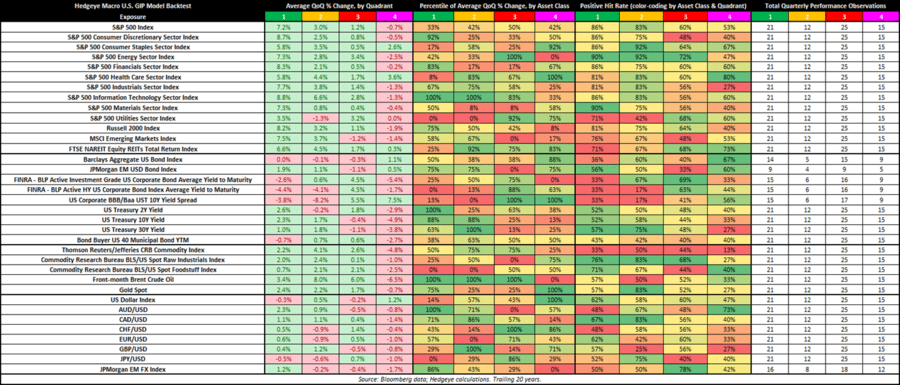

With that being said, timing is important and with Draghi sitting on sovereign QE/Euro devaluation the dollar strength could continue over the intermediate-term. With our economy CURRENTLY still positioned in #Quad4, the returns by asset class in the table below would not suggest that it’s a good time to "buy value" in the energy space.

While demand is clearly slowing globally and the top-down signals we use suggest further downside risk, should prices remain here, we expect a decline in production in the first quarter of 2015 should prices stay put. Efficiency in extracting North American energy sources is undoubtedly improving, but cheap leverage on top of leverage is not.

Ben Ryan

Analyst