Conclusion: This is a binary set-up for RH and the market knows it. The company needs to put up a significant reacceleration in its top line. With 31% of the stock held short, there are plenty of people betting it won't. But we think the unit growth, category expansion, comp, and margin opportunities are coming together for RH, and will be apparent this quarter. RH remains our favorite name in Retail.

FULL DETAILS

We feel good about the RH earnings event on Wednesday after the close. Revenue should accelerate meaningfully as RH has finally hit the inflection point (after 7+ years) where square footage starts to enhance as opposed to shrink the top-line algorithm. We’re also seeing great strength in the brand’s online momentum, and should see a catch up from revenue that was delayed by problems with the sourcebook in 2Q. All-in, we’re looking for 24% growth, which is over 1,000bp better than the (unacceptable) 13.5% we saw in 2Q. The Street is straddling guidance at about 20-21%. On the EPS line, we’re at $0.52, which compares to the Street at $0.47 ($0.46-$0.48 guidance).

While the EPS beat should be nice, we think that there’s a binary nature to this quarter. Why? RH has never missed EPS, and it’s not going to start now. But it missed 2 of the last three quarters on the top line by an average of 4%. Even though the trendline growth rate (2-yr) remains well above 20%, the fact is that we’re arguing that RH will add $700mm in revenue next year alone (31% growth) and another $2.4bn over the following 3-years. We’re the first to call out that while the company undergoes its real estate build-out, there will be ongoing volatility in its’ top line on a quarter to quarter basis – that should last another 2-3 years. But weakness in 2Q needs to manifest itself in the 3Q revenue line. To be clear, we think that will happen. But if it doesn’t – timing or not – it will be very tough to argue a big multiple for RH over the near-term.

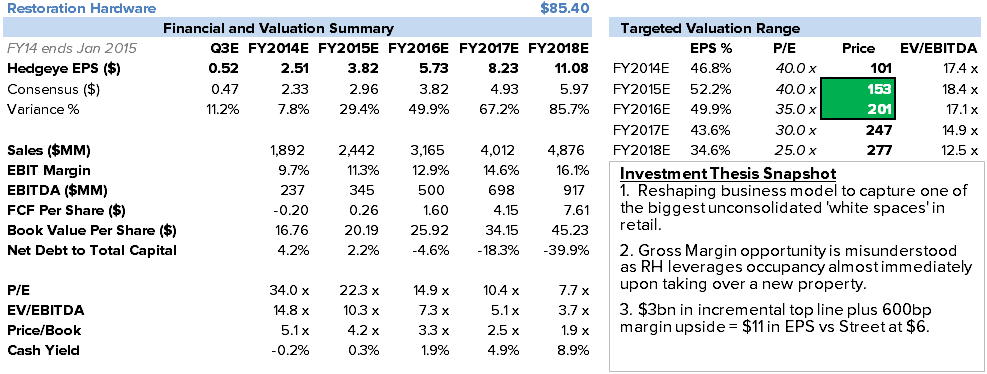

Details of Our Thesis. The way we see it, we think that RH will ramp from $2.50 in EPS this year to $11 in 2018. It’s an ambitious model, but completely achievable. The biggest barrier to getting there is RH itself. We think a few factors remain misunderstood – 1) The degree to which the high-end home furnishings market can be consolidated – not unlike what Ralph Lauren did to high-end apparel in the 1980s. 2) Our view that there are over 20 markets that could sustain a 50,000+ foot Design Gallery at a productivity rate of $1,200/foot. 3) The impact that occupancy leverage will have on Gross Margins, ultimately pushing GM% to 40%. Our key modeling assumptions are in the table below.

With Growth Comes The Multiple. If our model is right, then the company will be growing EPS at a CAGR of over 40% for the next four years. What kind of multiple is fair for a high-end category leader with a low-cost advantage that’s growing EPS at over 40%? We hate to just make-up multiples. But there are businesses growing at lower rates that carry a much higher multiple. UnderArmour grows at 25-30%, and yet it trades at near 70x earnings. Perhaps UA is grossly overvalued, and perhaps the market likes that someone came first and paved the way (Nike) showing what UA could look like when it grows up. With RH, people will have to use their imagination. But using 40x 2015 and 2016, we get to $150 and $230, respectively.

Why Revenue Should Accelerate In 3Q

Here’s a few supporting points for why we think revenue will accelerate.

- Square Footage Turns Decidedly Positive. We’re looking for 3.5% growth in square footage this quarter. That might seem like it falls into the ‘who cares’ category. But this is a company that has largely been shrinking its store base since before the last recession. This quarter it turns positive, and should be up roughly 30% by the end of next year. Note that the Atlanta Design Gallery that opened on November 20 falls into 4Q, and should account for about a 6% pop in consolidated square footage.

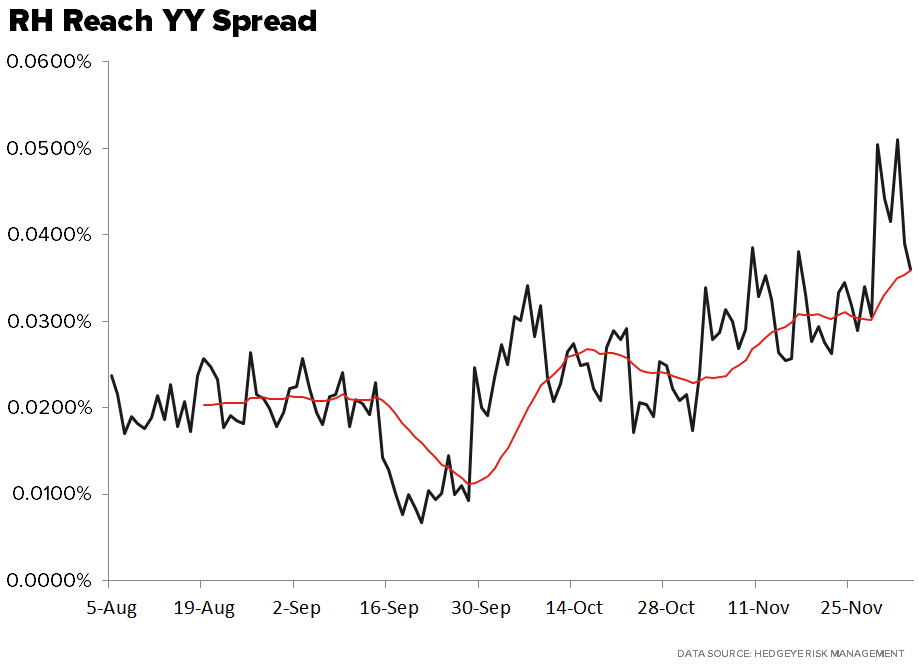

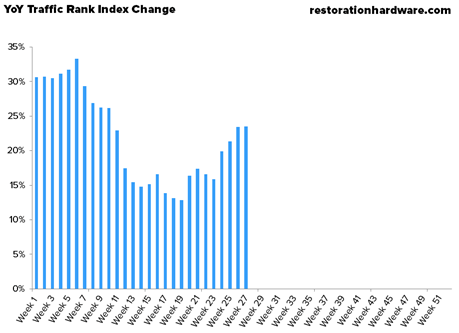

- RH Online Presence Has Strong Momentum. There are several tools that we use to track the online momentum for consumer brands, including RH. The chart below shows the spread in ‘reach’ versus last year. The percentages are irrelevant – as they show the percent of all internet users that visited www.restorationhardware.com. What we care about is the direction of the line. Up is good, and RH has been increasingly up.

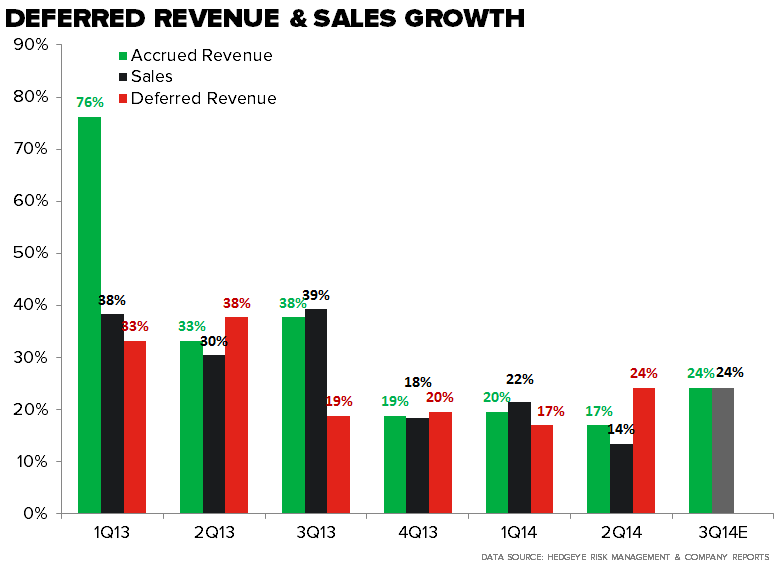

- Deferred Revenue Buildup. Every quarter, RH books deferred revenue, which represents product that has been ordered but is not yet delivered (RH gets paid when the consumer takes final delivery). There’s an exceptionally strong relationship between deferred revenue, and the upcoming quarter’s realized revenue. That is, except for 2Q. That’s when revenue stalled due to timing associated with a Friends and Family promotion, as well as what we think are miscues in its Sourcebook (ie 3,300 pages at once was a mistake). The deferred revenue alone synchs with our 24% revenue growth forecast.

- Inventory Supports Revenue Growth. One of the only times that deferred revenue will not accurately accrue to the upcoming quarter would be when there is not enough inventory on hand to fulfill orders. Then RH has a problem. That is absolutely not the case this time around, as RH ended 2Q with inventories up 35% -- and ready to ship to fulfill 3Q deliveries.

Some More Detailed Modeling Considerations

Square Footage:

- RH added one new store during the quarter on Melrose Ave. in Los Angeles. That equates to 10% growth in selling sq. ft. year-over-year and the addition of 9K sq. sequentially as the new 23,000 sq. ft. Design Gallery replaced the now idle 13,800 sq. ft. Beverly Boulevard location.

- With the opening of the first 2nd Generation Design Gallery in Atlanta during the opening weeks of 4Q, square footage growth is now done for the year.

- For the year the square footage growth algorithm looks like this: Design Gallery square footage +77%, Legacy Store square footage -6%, total selling square footage growth +9%, and total average selling sq. ft. growth +8%. *Note we model NYC store as a Full Line Design Gallery.

- Initial guidance for 2015 implies 4 to 6 openings and 30%-40% sq. ft. growth. Those will be heavily weighted towards the back half of next year.

Retail Comp:

- This may be the hardest line on the entire P&L to model as the store additions/subtractions and remodels make for a lot of moving pieces. For the quarter we are at 18%.

- Additional details

- Boston and Indy entered the comp base during June of this year. This will be the first full quarter where those two properties show up in the consolidated comp number.

- New York was removed from the comp base after the 17,000 sq. ft. remodel during the 2nd quarter. This is the most productive store in the entire fleet.

- The 13,800 sq. ft. store on Beverly Boulevard exited the comp base once Melrose opened at the tail end of the quarter. This store was operating in excess of $2,000/sq. ft.

DTC comp:

- On the last call, management indicated that DTC growth would outpace Retail growth until the real estate transformation catches up to fit the expanded product assortment. For the quarter we’re at 25% growth in the DTC channel. Up 700bps sequentially on the 1yr trend line and 1000bps on the 2yr.

- Visitation statistics were solid for the quarter. Up over 65% in every month during the quarter and 77% for the quarter in aggregate (+48% on the 2yr). The company was comping against a visitation suppressed 3Q13 when the company eliminated the fall source book. That coupled with the late shipment of the Source Book this year and prospecting efforts are the main drivers of the growth.

Combined Brand Comp:

- Putting the two pieces together, 25% DTC growth and 18% Retail comp, equates to a 22% combined brand comp for the quarter.

Revenue:

- Guidance of $475-$485 implies 20%-23% growth. An acceleration of 1000bps sequentially on both the 1 and 2yr trend line.

- The Source Book timing issue caused books to arrive in homes about a month later on average compared to last year. Some of those sales were lost forever especially in seasonal categories like outdoor. But, given the company’s extended shipping window and strong traffic trends in the DTC channel we believe there was a healthy backlog headed into 3Q.

- Stores in Greenwich and New York were open for the entirety of the quarter. And, there was very little interruption caused by the shift from Beverly Boulevard to Melrose Ave. in Los Angeles with the late October opening.

Gross Margin:

- We’re modeling 100bps of Gross Margin expansion in the quarter. Here’s a quick look at the headwinds and tailwinds for the quarter…

- Headwinds

- Promotions: Margins were up 230bps in 2Q. Part of that was due to reduced promotional selling during the company’s Friends & Family event in July. Some of that may have been pushed into the early October Friends & Family sale. Which we should note was the exact same timing as last year.

- Dead rent: The company started to feel a drag from new properties scheduled to open in ’15 in the quarter. That will be more pronounced in 4Q due to the back-half weighting in the opening schedule next fiscal year and the companies 6-12 month buildout schedule. But, it’s something that we are aware of.