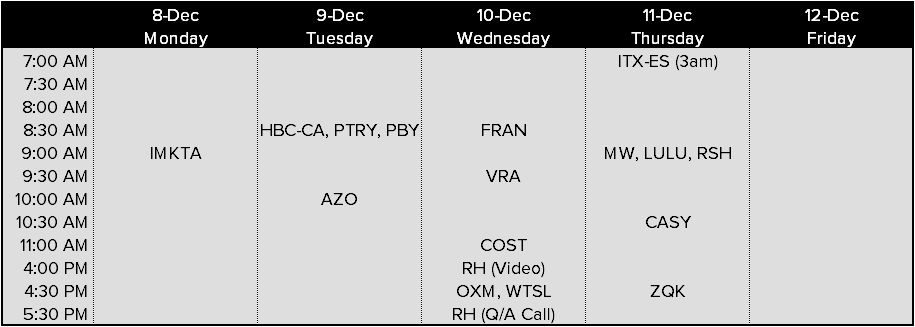

EVENTS TO WATCH

COMPANY HIGHLIGHTS

KSS - 10Q: e-Commerce

Takeaway: KSS released its 10Q on Friday. The most notable takeaway is 31.6% growth in the online channel. Despite the big jump we still saw a sequential deceleration on the 2yr because of the replatform during 2Q13. Specifically, when we look at the quarterly comp composition (chart 2), we see that after backing out the e-commerce growth, it implies that the store comp was -4%, matching new lows. Juicy and Izod aren't really having the desired effect for the bulls. KSS remains our top short.

Black Friday Weekend Online Shopping

Takeaway: There's nothing investable about this chart, but we find the content to be fascinating. This shows the hourly trend in shopping online over the Black Friday weekend. Three takeaways…

- The holiday shopping season appears to being in earnest online at about 8pm on Thanksgiving night.

- The notion that Cyber-Monday is being 'pulled forward' to Black Friday does not appear to be true. Yes, there is a step-up from Thanksgiving Day levels, but still nowhere compared to the spike we saw on Monday.

- Notice the huge drop-off from Cyber-Monday to Tuesday. Is that because people all of a sudden don't want to shop? Absolutely not. That's when the online promotional spigot all but shuts down -- at least relative to what had been in place the preceding four days. This is the 'tail wagging the dog', in that consumers will shop when the promotions are there. When the deals go away, so do shoppers.

OTHER NEWS

DLIA - Teen Clothing Retailer Delia’s Files for Bankruptcy

(http://www.bloomberg.com/news/2014-12-08/teen-clothing-retailer-delia-s-files-for-bankruptcy.html)

BEBE - Bebe confirms data breach hit U.S. retail stores

(http://fortune.com/2014/12/05/bebe-data-breach/)

AMZN - Instacart Is Raising North Of $100 Million At A $2 Billion Valuation

(http://techcrunch.com/2014/12/05/instacart-2b-kleiner/)

Black Friday’s momentum sees slowdown with Canadian shoppers

AMZN - Amazon Gets $5 Million From N.Y. to Bring 500 Jobs to Manhattan

Nintendo Heads for Best Holiday in Years as Profit Seen Triplin

FIVE - Five Below names COO and retail veteran Joel Anderson as CEO

(http://www.chainstoreage.com/article/five-below-names-coo-and-retail-veteran-joel-anderson-ceo)