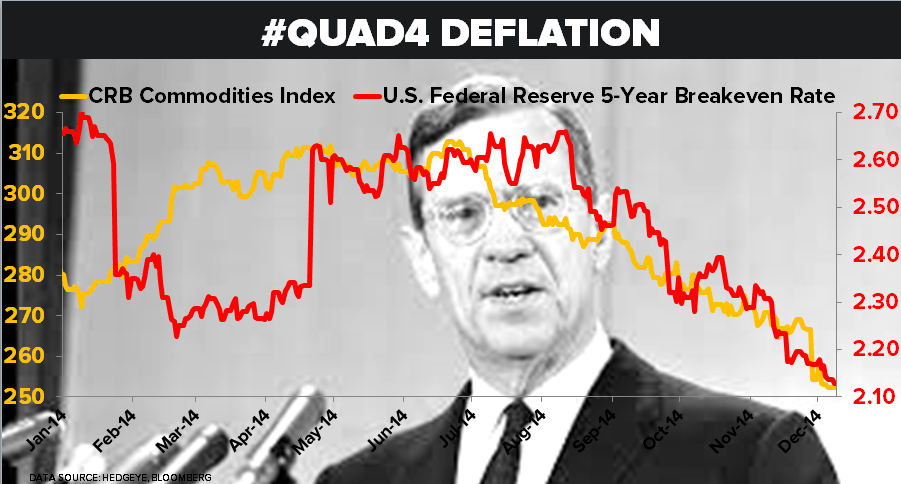

Here's a little snapshot of our Q4 Macro Theme #Quad4Deflation: 1) US 5yr Breakevens dropped another -4 basis pts on the wk to 1.36% (crashing -26%, or -47bps, YTD) 2) CRB Commodities Index deflating another -0.8% last week to -9.9% YTD

Here's a little snapshot of our Q4 Macro Theme #Quad4Deflation: 1) US 5yr Breakevens dropped another -4 basis pts on the wk to 1.36% (crashing -26%, or -47bps, YTD) 2) CRB Commodities Index deflating another -0.8% last week to -9.9% YTD

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.