Current Ideas:

Key Takeaway:

From a risk management standpoint, we remain very focused on the rising risk of a Russian banking crisis. In a nutshell, Western sanctions are driving capital out of the country causing the Ruble to weaken. Falling oil prices are compounding the problem. The CEO of Sberbank, Russia's largest bank with 46% deposit share, said back on November 14th that if the Russian economy were to decline by more than 1.2% in 2015 Sberbank would need the State to bail it out. Sberbank's CDS tacked on another 97 bps over the week, rising to 503 bps this week.

Russia's GDP was most recently growing at 0.7% Q/Q annualized. Energy contributes between 20-25% of GDP and oil prices are down by ~30%. This implies a drag on GDP of -6-8% as we roll into 2015. In other words, if sanctions aren't removed and oil prices don't bounce, the Ruble should continue to lose value and Russia will need to bail out its banking system at a time when it's already hemorrhaging cash ($100bn/year) from falling oil prices. That makes for a nasty mix with US equities at/near all time highs.

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 3 of 12 improved / 3 out of 12 worsened / 6 of 12 unchanged

• Intermediate-term(WoW): Positive / 6 of 12 improved / 4 out of 12 worsened / 2 of 12 unchanged

• Long-term(WoW): Negative / 2 of 12 improved / 3 out of 12 worsened / 7 of 12 unchanged

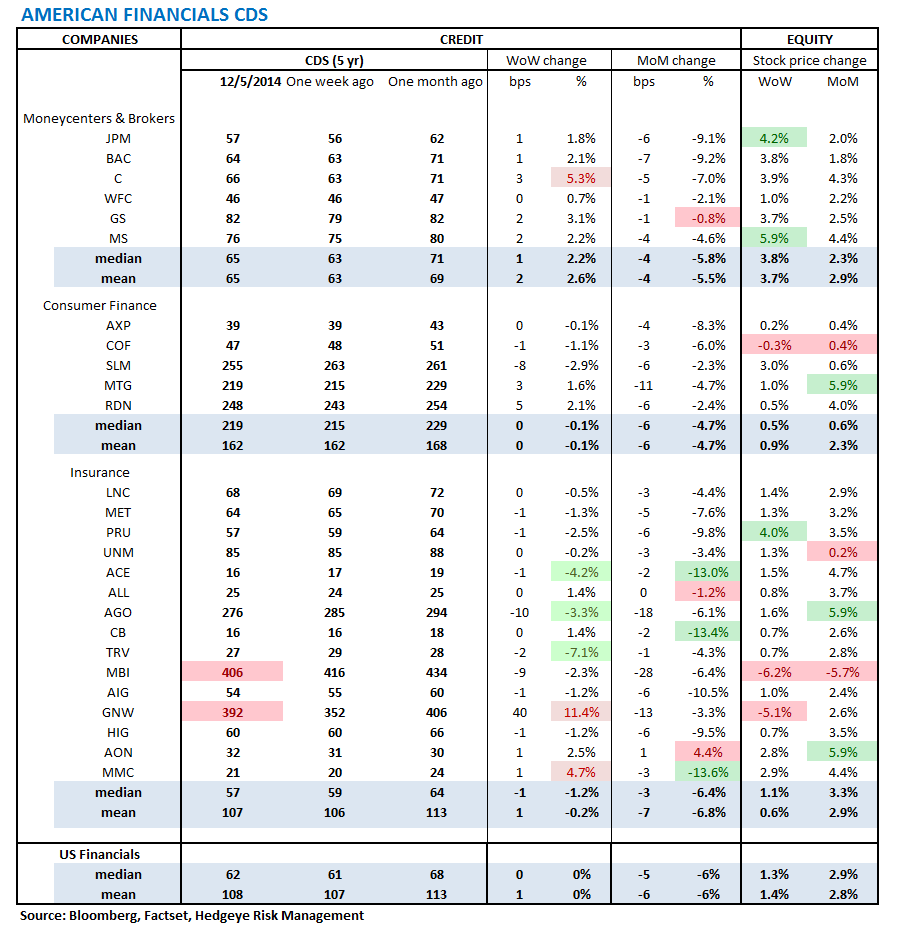

1. U.S. Financial CDS - Swaps widened for 13 out of 27 domestic financial institutions. Genworth Financial widened the most, continuing to exhibit volatility after the company's early November announcement that a review of its claims reserves and goodwill would result in a combined charge of over a billion dollars pre-tax. Travelers tightened the most.

Tightened the most WoW: TRV, ACE, AGO

Widened the most WoW: GNW, C, MMC

Tightened the most WoW: MMC, CB, ACE

Widened the most/ tightened the least MoM: AON, XL, GS

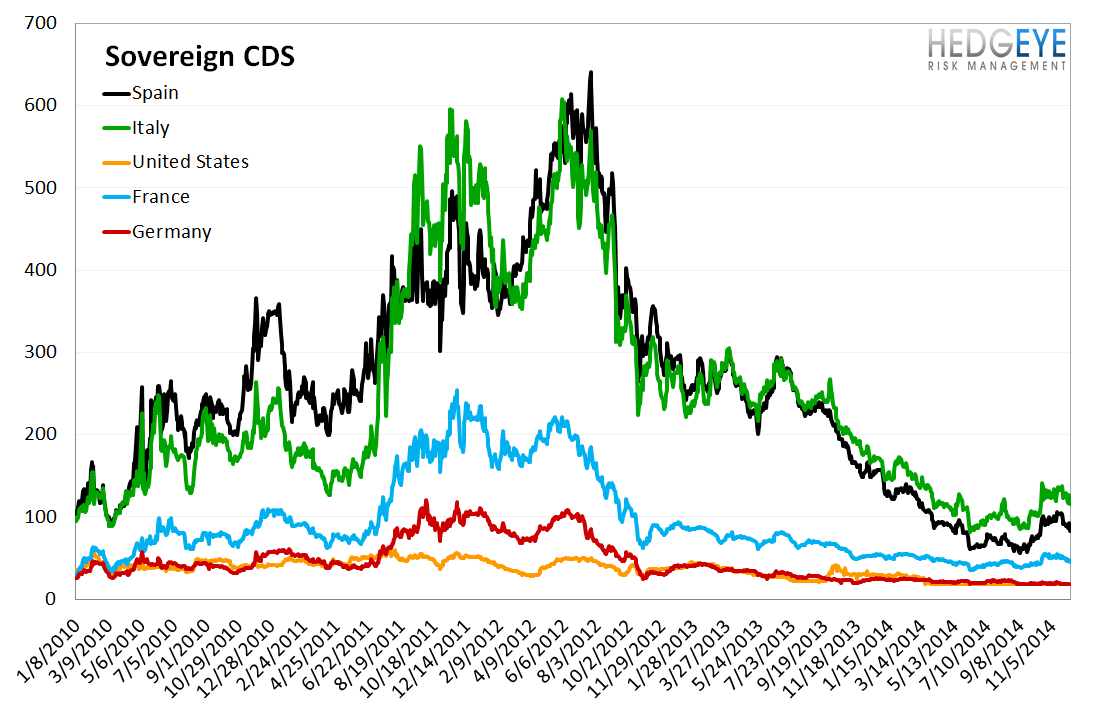

2. European Financial CDS - Swaps mostly tightened in Europe last week with an average -4.7% move. There were a few extreme movers in the region. Russia continued to show extreme widening WoW: +97 bps, +23.9%. Sberbank's CDS at 503 bps flag reflects the rising risk in the Russian economy. Portugal's Banco Espirito Santo tightened to most last week (-88 bps, -17.8%) as Portuguese authorities near a sale of a few of the collapsed bank's parts.

3. Asian Financial CDS mostly widened last week with a median 2.9% move. Significant tightening in India skewed the average move down to -0.4%.

4. Sovereign CDS – European Sovereign Swaps mostly tightened over last week. Italian sovereign swaps tightened by -10.7% (-14 bps to 115 ) and American sovereign swaps widened by 10.3% (2 bps to 18). American CDS displayed a divergence from the stock market's (S&P 500) flat performance for the week.

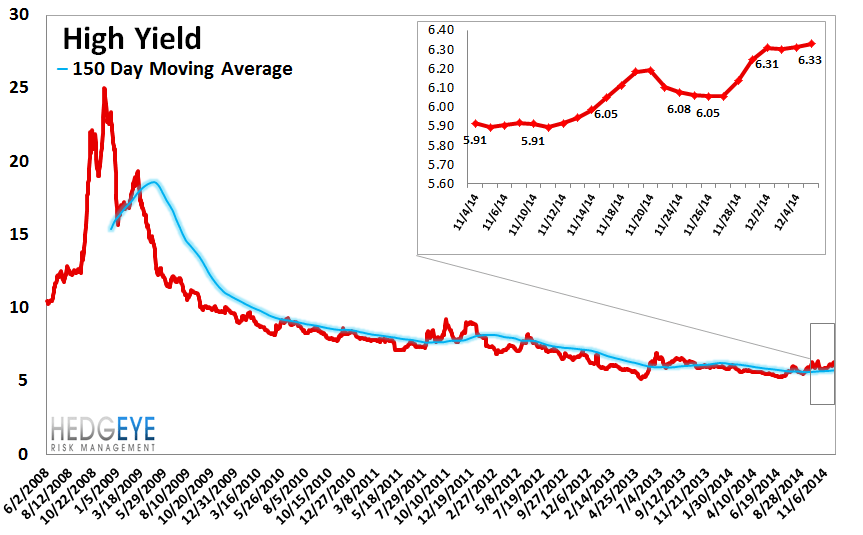

5. High Yield (YTM) Monitor – High Yield rates rose 19.3 bps last week, ending the week at 6.33% versus 6.14% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 10.0 points last week, ending at 1872.

7. TED Spread Monitor – The TED spread rose 0.2 basis points last week, ending the week at 22.3 bps this week versus last week’s print of 22.06 bps.

8. CRB Commodity Price Index – The CRB index fell -5.4%, ending the week at 252 versus 267 the prior week. As compared with the prior month, commodity prices have decreased -6.2% We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

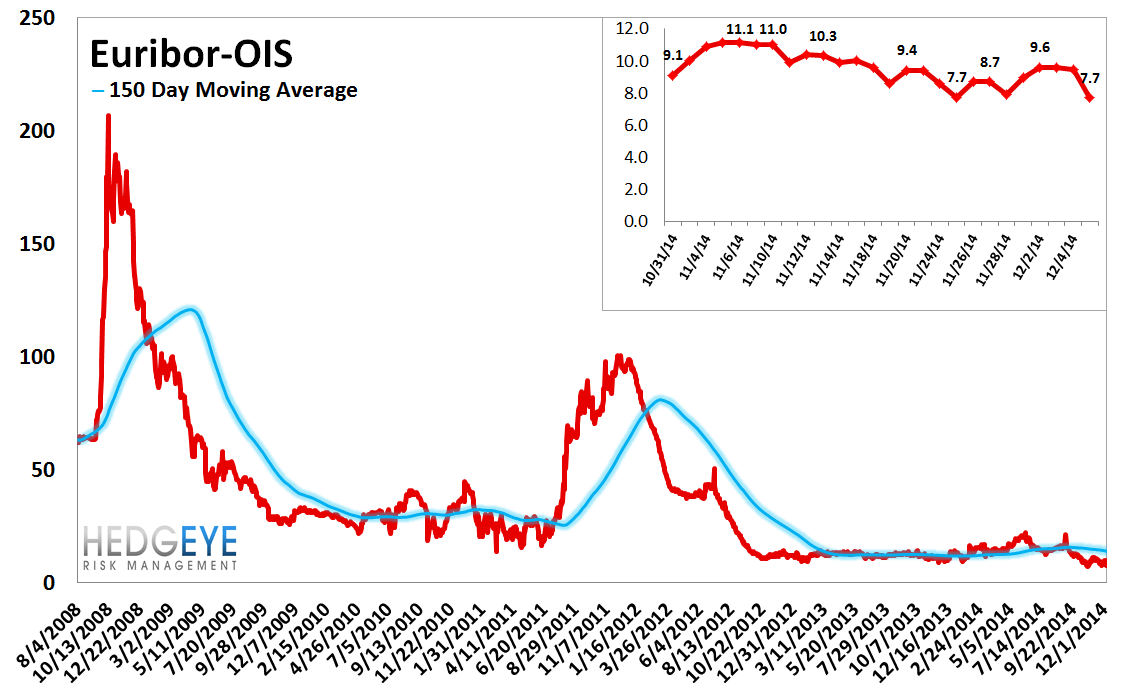

9. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 0 bps to 8 bps.

10. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 2 basis points last week, ending the week at 2.632% versus last week’s print of 2.608%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

11. Chinese Steel – Steel prices in China fell 1.1% last week, or 33 yuan/ton, to 2915 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

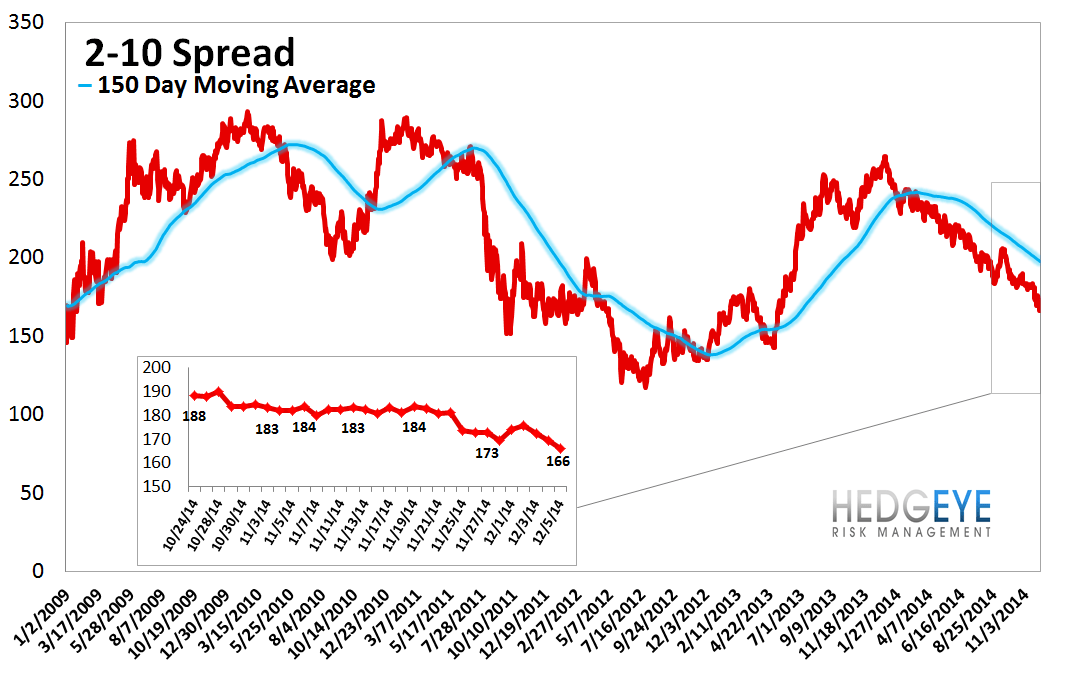

12. 2-10 Spread – Last week the 2-10 spread tightened to 166 bps, -3 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

13. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 0.3% upside to TRADE resistance and 3.3% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT