China is not a communist state. China is an autocracy --one with a governmental system that incorporates communist philosophical roots and social policies combined with a unique experiment in state managed capitalist economics, but an autocracy nonetheless. The entire nation is ultimately overseen by an unelected politburo selected through a process of patronage and nepotism.

Tomorrow’s celebration of the victory over the Nationalist forces and founding of the People’s Republic will provide the country’s leaders the opportunity to embrace the exploded myth of the socialist workers’ state while in the background the wheels of rapid private sector development continues at a frantic pace. In short, tomorrow’s parades, with displays of cold war nostalgia like missiles on trailers as well as thoroughly modern features such as female soldiers decked out in chic pink uniforms with white boots and tights, will be a national exercise in delusion.

The fundamental failure of the state founded 60 years ago was brought home during the cold war as the economic might of the US and its western allies provided technological and military development that the communist nations could simply not keep pace with. Although the introduction of economic reform began in the late 1970’s when Deng Xiaoping began the painful process of recovery from the madness of the cultural revolution, it was the collapse of the Soviet Union under unrelenting pressure from the west that heralded the end of economic isolation as the Communist party leadership acknowledged the new reality of competing on the global stage.

The system that was ultimately adopted could be described as an attempt at having one’s cake and eating it as well. Beijing continues to control every aspect of life and ultimately owns all property while embracing the economic clout and prosperity brought by private enterprise. The bubbles of social discontent that have been amplified in international media coverage in recent years are a constant reminder to the party of the golden rule of benevolent despotism: the people will only be content to surrender personal freedom if the social contract (universal employment, steadily improving living conditions, social justice etc.) is fulfilled. The global economic crisis could have disrupted internal harmony, and this threat spurred Beijing into pouring massive amounts of money into the system in an attempt to buy growth. Buying growth is the most expensive thing that a government can do short of war and, to date, it appears to be working and to have been worth the cost.

MOTORING AHEAD

Last night the HSBC PMI Index for September was released with a level of 55.1, showing that manufacturing expanded for the 6th consecutive month and demonstrating that the stimulus policies adopted by Beijing last year to spur internal demand are continuing to reverberate through the system.

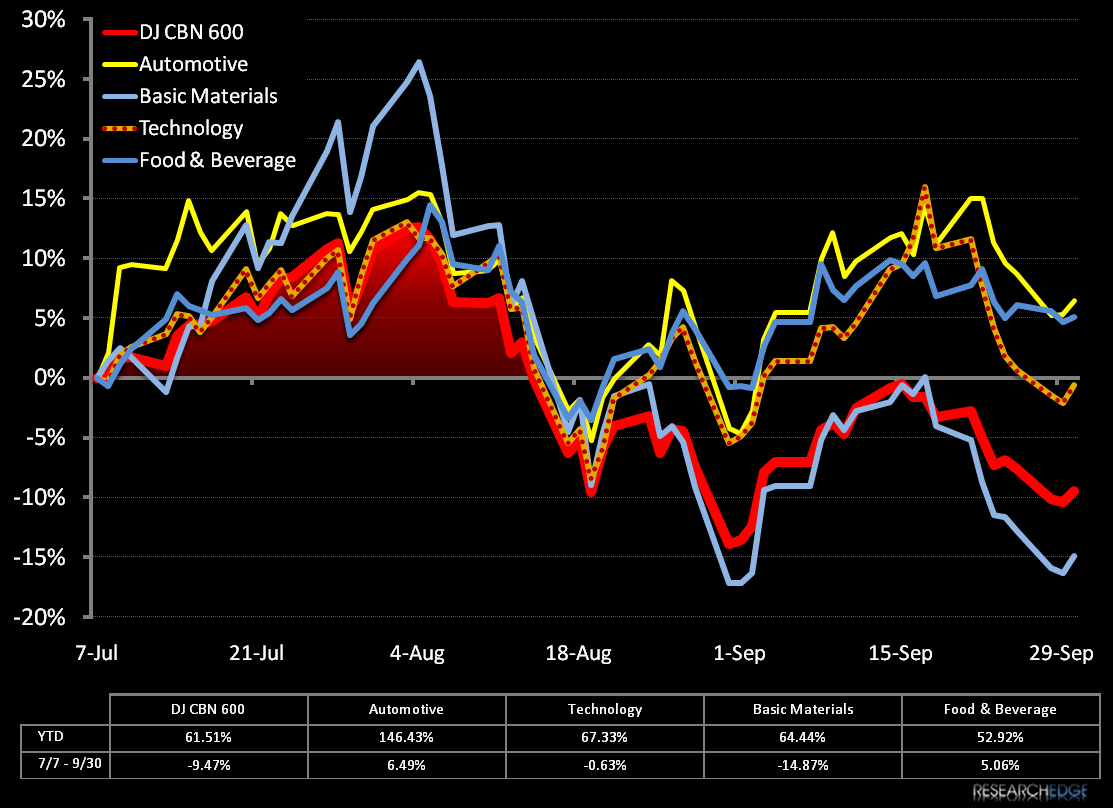

When we issued our call on Chinese equities in July, we wrote that we anticipated that the market was due a correction, and that specific sectors and industries would outperform. Of our four picks, three--Automotive, Consumer Staples/Food & Beverage and Technology Stocks--have handily beaten the broad indices while Basic Materials have lagged under deflationary pressure. In the chart below, we have broken out these components from the CBN 600, an index comprised of the 600 largest equities by capitalization on the Shanghai and Shenzhen exchanges.

We continue to be bullish on the developing internal demand: with CAAM recording more than a million new cars monthly since March, increasing evidence of demand for nutritional diversification and the continuing transition to a society of internet surfing smart phone users, our outlook has not changed. We anticipate that the massive amount of infrastructure improvement needed in Central and Western regions will ultimately drive Basic Materials, aided by our expectations for returning global inflation in the coming quarters.

Andrew Barber

Director