“When your enemy is making mistakes, don’t interrupt him.” – Billy Beane

This week I had the pleasure of presenting the state of Hedgeye’s Research engine to nearly 60 of my colleagues throughout our Firm. There were about a dozen key conclusions, followed by a spirited dialogue (which is part of our DNA). But there was one key component of our discussion that I believe is relevant to not only our own team internally, but also to our customers, without whom Hedgeye would not have had such a banner year in 2014. That component is how our business model is structurally different, and how it allows us to think, act, and produce money-making ideas in ways that are dramatically different from the #OldWall.

The Model: WallStreet2.0

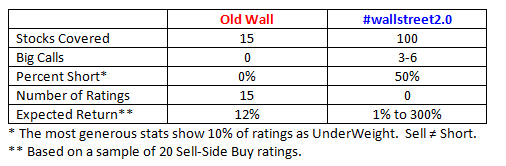

Before understanding how we generate ideas, it is important to understand the structure that allows us to do what we do – on a repeatable basis. Consider the table below. I compared an OldWall model against Hedgeye on some key operating metrics. The #OldWall could be your typical bulge bracket ibank, a regional research firm, or pretty much anyone else who is in the business of selling research. Let’s compare and contrast…

1) Stocks Covered: A typical #OldWall analyst will have a fixed coverage universe between 12 and 18 stocks. It takes an average of one month per company to ‘initiate coverage’ on a new name (been there, done that). If you ask that person about a name on the fringe of their coverage, they’ll likely answer “sorry, I don’t cover that”. They’re not allowed to have an opinion without an ‘official’ rating. Note: if an analyst at a Hedge Fund told his/her PM that “I don’t cover that”, they’d soon be out of a job. At Hedgeye, the typical Sector Head has about 100 names under coverage. In Retail, the sector I have the privilege of covering, there’s about 130 names I track regularly. No one at Hedgeye will ever utter the words ‘I don’t cover that’. They might say something like “I’m not familiar with it right now – can I get back to you in a day?” But “I don’t cover it” is not in our vernacular.

Does that mean that I have a ‘call’ on 130 names? Absolutely not. But I have a tremendous playing field from which to source big ideas. I hold myself responsible – as do the other Sector Heads at Hedgeye – to have a repeatable process in place to consistently fish where the fish are. By the time a company works its way through our vetting process, we’ve checked enough risk management boxes such that it’s like a batter stepping up to the plate with a 3 and 0 count. Chances are grossly in favor of that player getting to first base – at a minimum.

2) Big Calls: The way I see it, if I can’t find at least three big longs and three big shorts at any given time out of a group of 130 stocks, then I don’t deserve my seat. Plain and simple. If I were to look at those 130 charts (which I do every weekend) I can assure you that there’s a heck of a lot more than three names that doubled last year, and three that got cut in half.

Let’s add another dimension to the concept of a Big Call. Actually, let’s add two more. Now I’m talking Keith’s language -- TRADE, TREND and TAIL. We’re asked so often why we don’t have ratings. The answer is that the concept of a ‘rating system’ is broken. What if there is a name that we think will double in 18 months, but is going to miss the upcoming quarter by 20%? It might be a short for a more nimble investor, or a long for someone with a 3-year duration that looks through quarterly earnings oscillations (admittedly not many of those people exist, but you get the point). It’s our job to help customers navigate the duration curve.

3) Percent Short: Roughly half of our calls are short. And I’m not just talking about TRADE positions. Each of our Sector Heads has about half of their respective calls on the short side. Heck, our Energy and Internet Analysts have nothing BUT shorts – and they have an enviable track record (check out Kaiser’s call on LINE). The reason why I note in the table above that 0% of Sell-Side calls are Short is that I have yet to see an #OldWall report that actually uses the word ‘short’. About 10% of ratings in an informal check were either Sell or Underweight. But none made an outright short call, and the average price decline was only 5% (which is hardly shortable in today's liquidity environment).

4) Expected Return: The average expected upside for Buy ratings on the Sell side is about 12% for Retailers. If I’m investing real money, I’m probably not going to get too excited about something that gives me a 12% return, unless there is zero potential for downside (which is impossible). In my little world, I’d point out Restoration Hardware, which is a name we’ve liked since $32 (it’s $84 today), and we still think it’s a winner. For those that like it on the sell side, the debate seems to be whether it will be a $90 stock or a $100 stock. From where I sit, the bigger question is whether it is a $200 vs $300 stock. Will it get there tomorrow? No. But by 2018 I think RH will earn $11/share. The consensus is at about $6. It looks expensive today if you believe the Street. But it’s extremely cheap if I’m right. I can guarantee you that if I were at my former (sell side) employer, I literally would not have been allowed to go out with estimates and a resulting equity value that was so far outside of the mean.

One of the inherent challenges to having such a broad coverage approach is that we’ll miss some big moves. With a list of 130 stocks, I can guarantee I’ll miss some big longs and shorts in 2015. I’m not happy about that one bit, but as long as I’m right on the names I pick and help our customers make money, then that’s a win from where I sit. As long as we stick to our process and keep stepping up to the plate with a 3-0 count, I’m downright excited about what 2015 has in store.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.16-2.30%

SPX 2037-2079

RUT 1148-1190

Nikkei 16,098-17,930

VIX 11.71-14.38

WTI Oil 62.99-70.64

Get on base,

Brian McGough

Managing Director and Retail Sector Head