This note was originally published at 8am on November 20, 2014 for Hedgeye subscribers.

“In the end, if you build it, they may not come.”

-Jim Rickards

Whether it’s the Japanese burning their currency, a demigod named Draghi “saving” Europe, or the Fed’s perpetual Policy To Inflate asset prices, I often wonder if Rickards is right – now that markets have built these expectations, will the growth come?

So far, the long-end of the bond market says no. On growth that is… but what are markets telling you about the centrally planned illusion of growth (i.e. inflation expectations)?

And “what happens when you manipulate markets using price signals that are the output of manipulated markets?” (The Death of Money, pg 86) Never forget that the biggest risks to markets are the critical answers to the toughest questions.

Back to the Global Macro Grind…

I spent all of yesterday seeing Institutional Investors in Greenwich, CT. The meetings, as always, were tremendous learning opportunities. And there was one moment in one of the meetings that I’ll never forget.

As I was sitting across from a Portfolio Manager, the Federal Reserve’s “Minutes” (from their last meeting) were released. So, I sat there and watched Liesman @CNBC spew his interpretation of what he thought the Fed said… and the seasoned PM just giggled.

Even at the most sophisticated funds, whether they like it or not, this is modern day “macro” – where you have to not only think about what you think… but seriously consider what everyone else was told they should think…

Here’s what I think was incremental in those Fed Minutes:

- Inflation expectations are falling

- The Fed only has one move to address that newfound concern

- In the next 3-6 months, as US inflation falls, the Fed will get more dovish, because of that

Since our “Bad #Deflation” view is not yet consensus, it’s really hard for consensus to get why this is bearish for bond yields (and bullish for the Long Bond, TLT, EDV, etc.). But markets almost always front-run consensus – and that’s already in motion.

After our interlude with the English-major turned pretend macro savant (who has never traded a market in his life), the Portfolio Manager asked me a very simple question that I get asked a lot: “what things should I look at to monitor your #deflation view?”

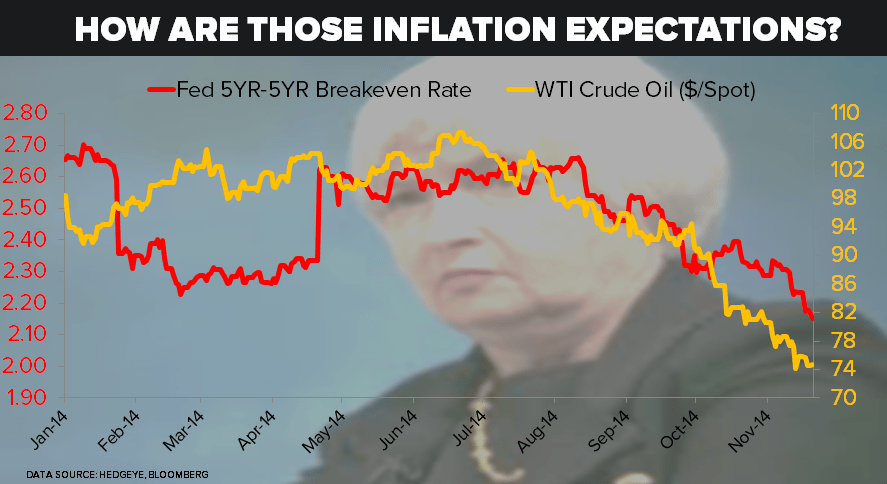

I answered by referring him to exhibit 15 (the slide in my #Quad4 Deflation Macro deck) that shows #InflationExpectations:

- TIPs (5 year Breakeven Rate)

- Fed 5Y-5Y Forward Breakeven Rate

Then I said:

- The price of Oil relative to my bearish TREND view

- CRB Commodities Index (TREND resistance = 281)

- Russell 2000 relative to my bearish TREND view

The price of Oil ($74.20/barrel) continues to crash this morning (-31% since June); the CRB Index is trading at 267 (-4.6% YTD); and after having another horrendous day (both absolute and relative to US Equities yesterday) the Russell 2000 is DOWN (again) for 2014 YTD.

Back to real economic growth expectations, I told investors yesterday what I’ve been telling them all year long – my catalyst is the cycle. As the growth cycle data slows, whatever these “bullish surveys” are telling you will look wrong.

That’s what’s happening from China to Europe this morning (they release Producer Manufacturing and Services data for November). Literally all of the growth data slowed.

While China’s PMI print of 50.0 wasn’t as bad as France’s (47.6 NOV vs. 48.8 OCT), that’s not saying much. Bond Yields are falling because the rate of change in global growth is slowing.

When both growth and inflation data slows, expectations for asset price inflation in those things slow. So BUY slow-growth-yield-chasing assets (TLT, EDV, MUB, XLV, XLP, XLU) and keep SELLING growth and/or inflation expectations (IWM, KRE, XOP, EWQ, VWO).

And that’s all I have to say about that.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.29-2.36%

SPX 2005-2055

RUT 1141-1173

France (CAC 40) 4139-4281

YEN 116.02-118.64

WTI Oil 73.01-76.13

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer