KEY POINTS

- GMV DRIVES BABA’S MODEL: Marketing & Commissions represent ~80% of BABA’s revenues. Both are driven off its GMV, which we expect to decline precipitously through F2017 as weaker consumer pressure average spending. See link below for more detail.

- MODEL FACING SECULAR PRESSURE: Slowing GMV growth naturally bodes poorly for commissions. The bigger issue is Marketing Revenues (~60% of total), which is facing secular pricing pressure as a weaker consumer pressures ad conversions and ROI. We’re already seeing this in BABA’s financials today.

GMV GROWTH TO SLOW PRECIPITOUSLY

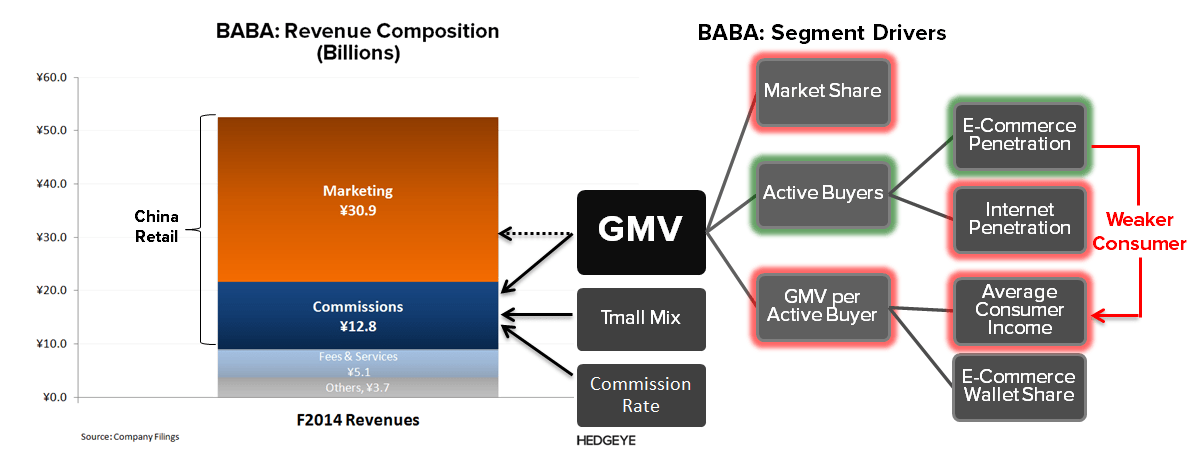

Below is a quick review of BABA’s core segments and drivers. In short, GMV drives roughly 80% of its model.

- Marketing Revenues (~56% of total): sourced from vendors on BABA’s sites advertising to BABA’s consumers, vying their GMV. Roughly 75% of BABA’s marketing revenues come from P4P ads, which require users to click the ads for BABA to get paid. BABA’s ad prices are determined through on online auction platform, which means its vendors set the price based on expected ROI. In short, the same factors that drive GMV also drive its marketing revenues.

- Commission revenues (~23% of total): generated as a percentage of the GMV transacted on its Tmall platform specifically settled through Alipay (BABA’s equivalent to Paypal). The commission rate ranges between 0.3% and 5.0%.

We expect GMV to decline precipitously through F2017. The key theme is that user growth will come from a much weaker consumer who can’t afford to spend as much. In turn, GMV will grow at a disproportionately lower rate than user growth since average spending/GMV will be on the decline; reversing what was a considerable tailwind into a headwind. We detailed our GMV analysis in the note below.

BABA: What the Street is Missing

11/26/14 08:03 AM EST

model facing secular pressure

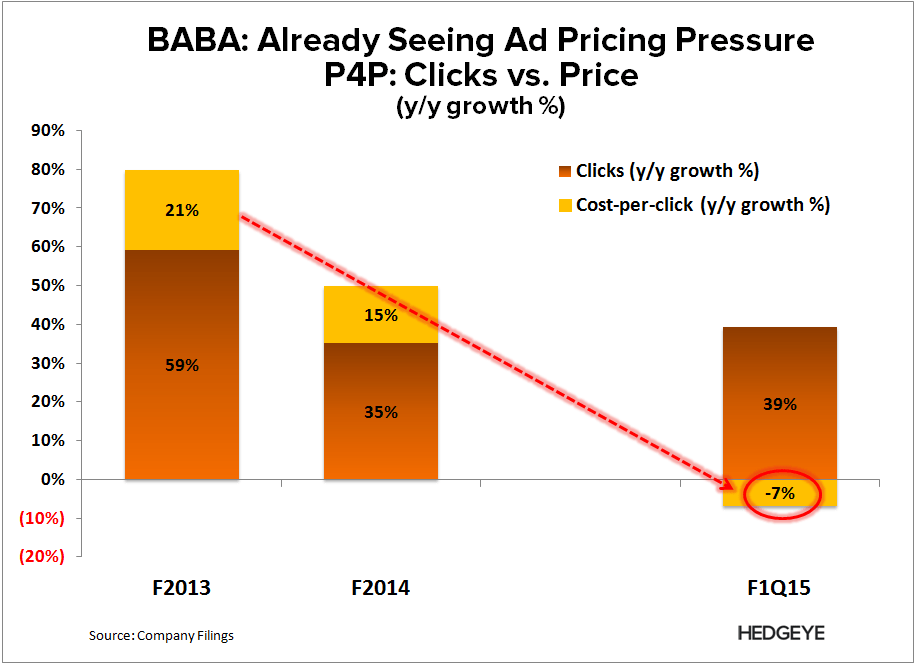

Naturally, slowing GMV bodes poorly for commissions. The bigger issue is BABA’s Marketing revenues (~56% of total). Our concern here is secular pricing pressure. BABA’s new user growth will come from less-affluent consumers who must be more selective with their purchases. Ultimately, that means that a vendor’s advertising ROI will decline as ad conversions (transactions) are inhibited by the average user’s waning ability to spend on its platform (as measured by average GMV).

In essence, the value of advertising on BABA’s platforms is directly linked to its average GMV, which we expect to decline through F2017, pressuring ad rates along the way. We already saw signs of this in its F1Q15 quarter ending 6/30/14 (comparable data isn't available for its most recent quarter). BABA attributed the F1Q15 decline in cost-per-click to a higher proportion of mobile marketing services, "for which our vendors currently pay a lower cost-per-click"

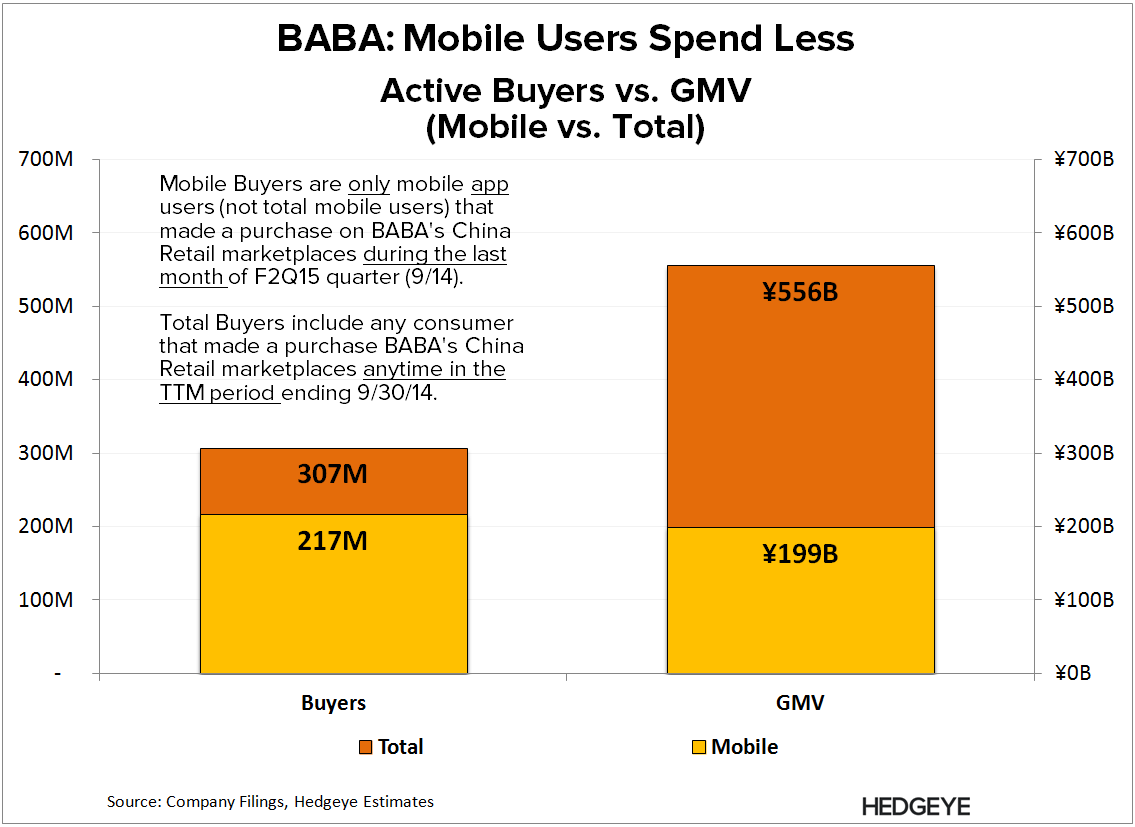

BABA’s ad prices are determined through on online auction platform, which means its vendors set the price. We suspect the reason why mobile rates are lower is because mobile is the low-cost vehicle for internet access in China. Put another way, mobile is how China’s less affluent access the internet. BABA’s reported metrics suggest as much, given that its mobile users spend less on average (mobile represents the majority of its shoppers, yet the minority of its GMV).

Mobile will likely remain the primary source of both new internet users and new BABA shoppers moving forward. New user growth will come a progressively weaker consumer moving forward; meaning the pricing pressure that BABA is already seeing in its marketing business is actually as secular headwind.

<chart5>

See the link below for a broader summary of our thesis. Let us know if you have any question or would like to discuss in more detail.

BABA: Leaning Short, But...

10/21/14 07:02 AM EDT

Hesham Shaaban, CFA

@HedgeyeInternet