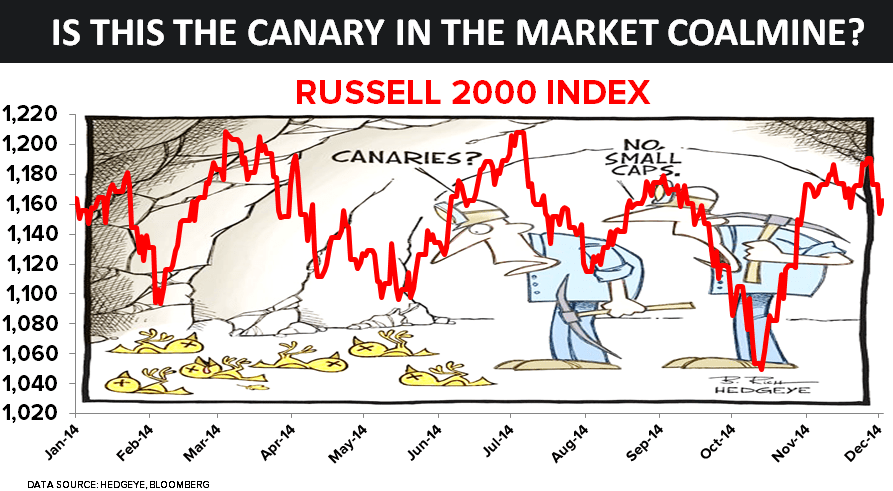

After doing nothing in November (it was literally flat for 4 straight weeks), the Russell 2000 dropped -1.7% yesterday in a straight line. It's back to down -0.9% for 2014 and down -4.5% since July.

Bull market? Or still a #bubble popping?

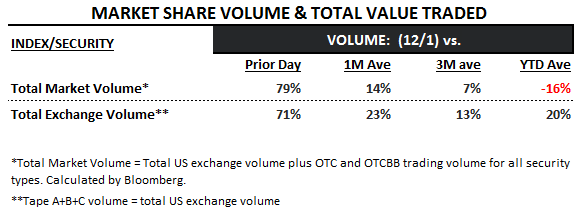

On a related note, Total U.S. Equity Market Volume was up +14% vs. its 1 month average yesterday as stocks fell.

In other words, the TREND of U.S. equity volume accelerating only on DOWN days continues to signal that the #LiquidityTrap (especially in small caps) remains.

Editor's note: This is an excerpt from Hedgeye morning research. For more information on how you can become a subscriber click here.