TODAY’S S&P 500 SET-UP – December 2, 2014

As we look at today's setup for the S&P 500, the range is 48 points or 1.19% downside to 2029 and 1.15% upside to 2077.

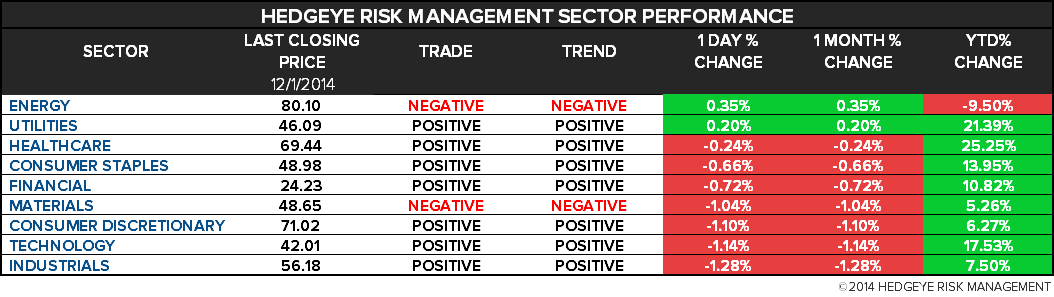

SECTOR PERFORMANCE

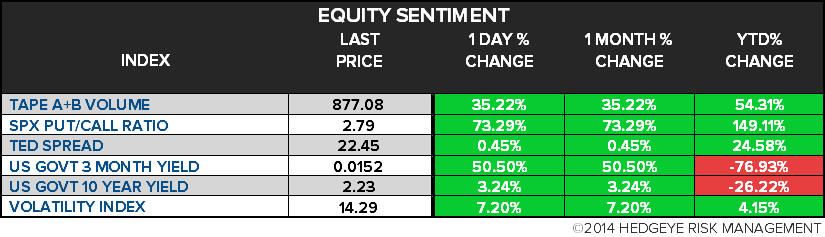

EQUITY SENTIMENT:

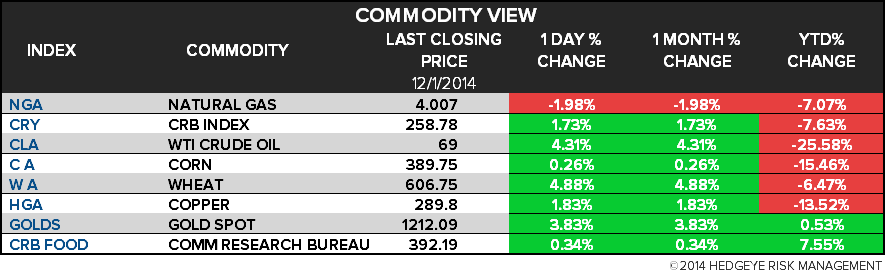

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.72 from 1.74

- VIX closed at 14.29 1 day percent change of 7.20%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: ICSC weekly sales

- 8:10am: Fed’s Fischer speaks in Washington

- 8:30am: Fed’s Yellen speaks in Washington

- 8:55am: Redbook weekly sales

- 9:45am: ISM New York, Nov. est. 55 (prior 54.8)

- 10am: Construction Spending, Oct., est. 0.6% (prior -0.4%)

- 11:30am: U.S. to sell 4W bills

- 12pm: Fed’s Brainard speaks via video to conf. in Los Angeles

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- 8:30am: Blood Products Advisory Cmte meets on whether ban preventing gay, bisexual men from donating blood should be partially ended

- 9am: House Homeland Security Cmte hears from Homeland Security Sec. Jeh Johnson on immigration executive order

- 9:30am: Health, Education, Labor and Pensions Cmte considers nomination of Lauren McGarity McFerran to serve as member of National Labor Relations Board

- 2:15pm: Senate Environment and Public Works Cmte hearing on “Super Pollutants Act of 2014”

- 2:30pm: Senate Commerce, Science and Transportation Cmte hearing on domestic violence in professional sports

WHAT TO WATCH:

- Japan’s Otsuka Agrees to Buy Avanir Pharma for $3.5b, or $17/shr

- GIC to Buy Blackstone’s IndCor Properties for $8.1b

- Cypress Set to Acquire Chipmaker Spansion for $1.6b

- Nov. U.S. auto sales: Chrysler ~8am; Ford ~9:30am; GM ~9:30am

- Web Consumers Stretch Out Holiday Shopping Beyond Cyber Monday

- Russia Scraps Proposed EU Gas Link in Favor of Turkish Delivery

- Russia Sees First Recession Since 2009 With 0.8% Slump Next Year

- Boeing’s Dreamliner Battery Fire Caused by Design, Probe Finds

- EU Said to Face Basel Committee Rebuke on Bank Capital Standards

- Ebola Crisis Will Cause Economies to Shrink, World Bank Says

- Wanda Holds Talks to Acquire Lions Gate, MGM in Hollywood Push

- Highland Seeks $250m From Credit Suisse Over Appraisals

- New York Times Gets at Least 85 Buyout Applications by Deadline

- Takata to Expand U.S. Air Bag Recall Nationwide, Nikkei Says

- Apollo Global Mgmt Leads in Bidding for PetSmart, NY Post Says

AM EARNS:

- Bank of Montreal (BMO CN) 7:30am, C$1.68 - Preview

- Vince Holding (VNCE) 6am, $0.33

PM EARNS:

- Ascena Retail (ASNA) 4:02pm, $0.26

- Bazaarvoice (BV) 4:01pm, ($0.09)

- Bob Evans (BOBE) 4:01pm, $0.33

- Guidewire (GWRE) 4:08pm, $0.03

- OmniVision (OVTI) 4:18pm, $0.51

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Saudi-Venezuelan Split Plays Out Behind Closed Doors in Vienna

- Gold Retreats After Rally as Stronger Dollar Reduces Demand

- Hedge Funds Add to Copper Bear Bets on Growth Risk: Commodities

- Andurand Fund Sees Oil Slump to $50 in 2015 as OPEC Steps Back

- What Will World Weather Do in ‘15? Forecasters Say El Nino Looms

- Steel Rebar in Shanghai Rises as China Inventories Decline

- Rubber Gains From 3-Week Low as Producers Seen Withholding Sales

- Funds Cut Bullish U.S. Crude Wagers Before OPEC Price Rout

- Palm Oil Rebounds From Biggest Drop in 16 Months as Crude Gains

- Port Hedland Engineers Approve Agreement, Ending Strike Threat

- Junk Backing Shale Boom Facing $8.5 Billion Loss: Credit Markets

- Putin Scraps South Stream Gas Pipeline on European Pressure

- Societe Generale Cuts 2015 and 2016 Brent Forecasts to $70/Bbl

- Iraq-KRG Government Reach Accord on Oil Exports: Al Mada Press

CURRENCIES

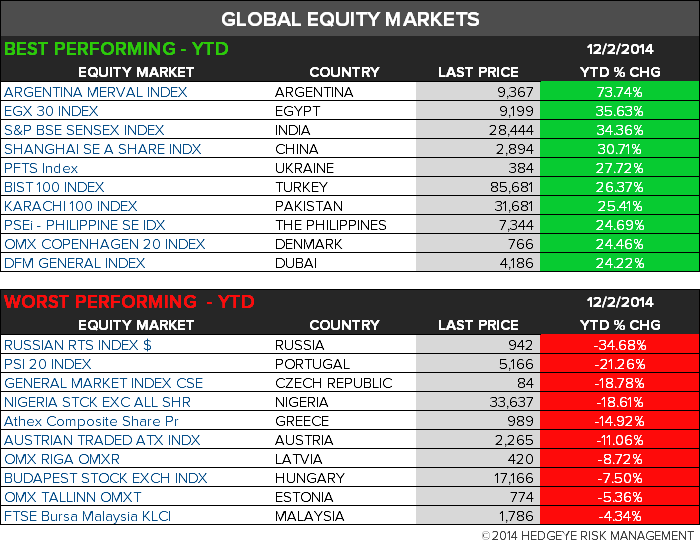

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

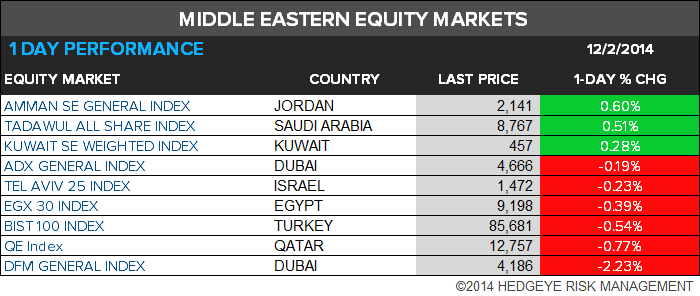

MIDDLE EAST

The Hedgeye Macro Team