This note was originally published at 8am on November 18, 2014 for Hedgeye subscribers.

“If at first you don’t succeed, then skydiving definitely isn’t for you”

- Steven Wright

Every November for the last decade, my high school buddies and I gather ahead of Thanksgiving to toast our respective, eclectic journeys into grown up’ness.

Every November for the last half-decade, domestic inflation expectations have crashed in an acute, seasonal de-crescendo.

Every November, Global Central Bankers meet in the collective effort to arrest economic gravity.

Every December, the Macro Muchachos of Hedgeye toast to the profit opportunities borne of the unique pervasiveness of this-time-is-different’ness

Back to the Global Macro Grind…

In mid-October, Fed researchers documented Residual Seasonality in the reported Inflation data whereby in 8 of the last 10 years consumer price inflation has tended to be higher in the first half of the year than in the second half – a pattern evident even in the seasonally adjusted data.

The research doesn’t really offer a supporting theory for the serial seasonality but the publication of the research suggests the Fed is, at least, aware of the seasonality and may (partially) discount the magnitude of sub-target inflation reported in the 3rd and 4th quarters.

Notably, the paper also fails to identify policy itself as a contributing factor in perpetuating that phenomenon.

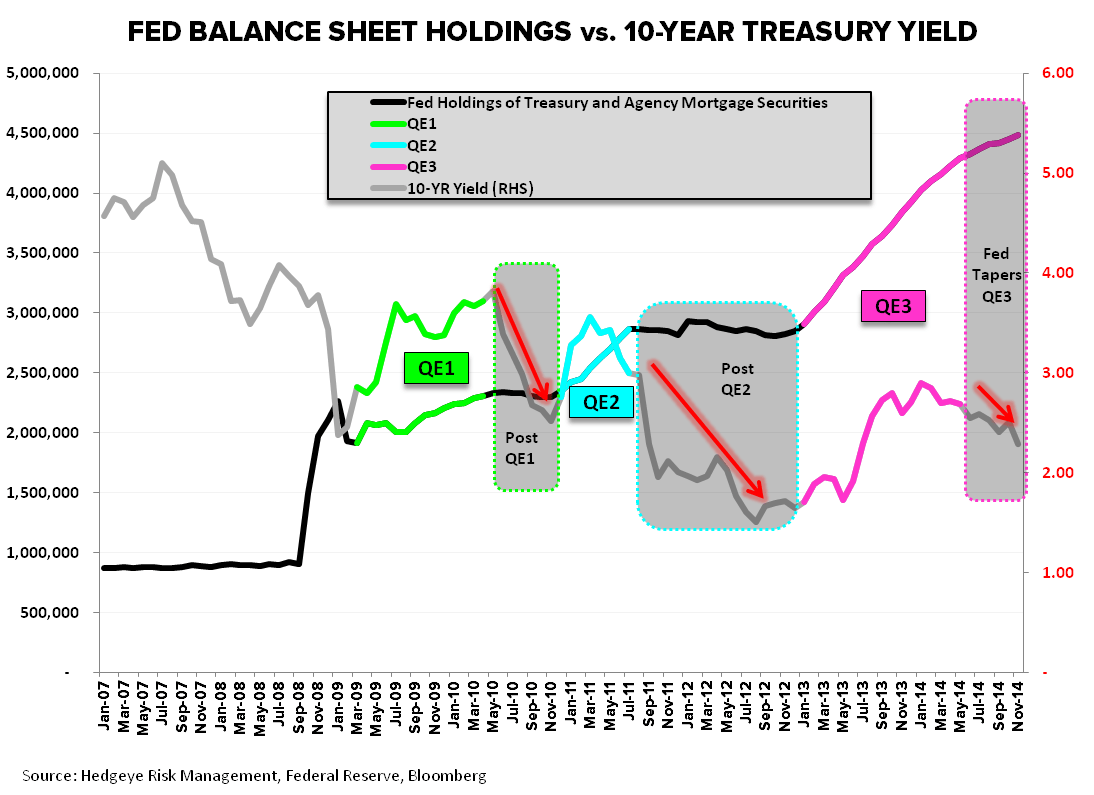

As can be seen in the 1st Chart of the Day below, policy initiatives have, in recurrent fashion, been implemented circa November in the wake of crashing growth expectations.

The direction of causality is (perhaps) open to debate but given that QE initiatives (generally announced in late 3Q) drove recurrent bouts of commodity price inflation & ‘escape velocity’ optimism into the New Year and that inflation expectations, in regular fashion, collapsed subsequent to cessation of QE initiatives is certainly suggestive.

The 2nd chart of the day, first published by our Financials team early in the year, shows that the end of QE1 & QE2 were both followed by sharp drops in 10-year treasury yields as the bond market priced in slowing growth and the inability of the private sector to successfully take the hand-off from the Fed. We’re inclined to interpret the current weakness in the 10Y as a protracted version of this recurrent cycle. Essentially, it's the same selloff seen in the last two iterations, but in slow-motion, over the duration of the taper instead of all at once.

The Fed wants to get out of QE if only to afford themselves the opportunity to get back in and the cost-benefit balance in terms of policy spillover to financial market (in)stability has shifted in favor of policy normalization, but established patterns/habits and embedded (dovish) ideologies are hard to break…. particularly with the Quad#4 scourge of disinflation and slowing growth becoming an increasingly tangible threat.

In physics, Constructive Interference describes the phenomenon of wave propagation and the propensity for two, in-phase waves to meet and produce a resultant wave larger in magnitude than either of the individual waves. Conversely, destructive interference, describes the propensity for two, out of phase waves to cancel each other out.

How does that relate to global macro risk?

A host of individual economies have traversed through Quad #4 over the last 5 years. However, the preponderance of G7/G20 economies have been at different points along the economic cycle at any given time – effectively in a state of destructive interference with the collective effect being a global economy oscillating above and below middling growth.

One benefit from being “out-of-phase” is that a rotate-the-QE model among DM central banks was a viable strategy and the race to the currency war bottom could proceed in a more-or-less orderly fashion.

At present, however, the global Macroeconomy is experiencing a constructive interference of sorts whereby individual country cycles are converging to an in-phase wave of disinflation and decelerating growth. The expedited collapse in major currencies and the discrete rise of $USD correlation risk is symptomatic.

Growth, domestically, was almost 5% in 2Q. The first revision to 3Q GDP will show a negative revision down to ~3%. The early estimate for 4Q from the Fed’s GDPNow model is pointing to +2.6% growth.

The U.S. has been a source of relative strength but the late-cycle data is cresting alongside persistent, negative revisions to global growth and inflation estimates. With bonds leading asset class performance YTD and the canonical defensive trio of XLV/U/P leading the 2014 rise in sector variance, the market has been discounting some measure of the current reality for some time.

Personally, I’m getting bored of being long the long bond and would welcome a shift back into early-cycle, high growth/high beta exposure but neither the quant nor the fundamental data are supportive of that, yet.

In other physics 101 news, Work still = Force x Distance.

Here, distance actually refers to displacement, so, if your net change in position is zero you didn’t technically do any work. On a physics score, the Russell 2000, having round-tripped in price, hasn’t done any work for two weeks….technically, with the S&P 500 up ~0% on an inflation adjusted basis since mid-2000, we haven’t done any work in nearly two decades.

Yup…all the collective speculation, all the sunken search and research costs, all the spurious activity = zero work done when measured in SPX price terms.

To Tuesday morning existentialism and bull markets in (economic) #gravity.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr yield 2.29-2.35%

RUT 1149-1181

CAC40 4149-4262

VIX 12.53-16.01

Yen 114.04-116.94

WTI Oil 74.05-76.99

Gold 1130-1203

Christian B. Drake

U.S. Macro Analyst