Below are Hedgeye analysts’ latest updates on our six current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

*We also feature a special market commentary from Hedgeye managing director Moshe Silver.

Our team is grateful for your continued business and trust and wish you and yours a Happy Thanksgiving weekend!

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

Sure... when you compare the Dollar to its peers in this global #CurrencyBurning gong show, the greenback looks pretty good.

IDEAS UPDATES

TLT | EDV | XLP | MUB

Slow-Growth, Yield-Chasing Update: More of the Same

In last week’s Investing Ideas update, we highlighted how trends across the preponderance of domestic high-frequency economic indicators were supportive of our view that both growth and inflation are slowing.

Along those lines, the preponderance of this week’s economic data was more of the same in that regard (i.e. slowing at the margins). Here are those key releases (in order of release date/time):

- Chicago Fed National Activity Index: 0.14 in OCT, down from 0.29 in SEP, which was revised down from an initial reading of 0.47

- Markit Services PMI: 56.3 in NOV, down from 57.1 in OCT

- Markit Composite PMI: 56.1 in NOV, down from 57.2 in OCT

- Real GDP: revised up +10bps to +2.4% YoY in 3Q , which was still down from +2.6% YoY in 2Q

- Case-Shiller Home Price Index: +4.9% YoY in SEP, down from +5.6% YoY in AUG

- FHFA House Price Index: +4.2% YoY, down from +4.8% YoY in AUG

- Conference Board Consumer Confidence Index: 88.7 in NOV, down from a downwardly-revised 94.1 in OCT

- MBA Mortgage Purchase Applications: -4.3% WoW, down from +4.9% WoW in the prior week

- Initial Jobless Claims: +313k WoW, up from an upwardly revised +292k WoW in the prior week; on a 4-week rolling NSA basis, the YoY rate of improvement (which implies the 1st derivative is negative) decelerated for the 5th consecutive week to -12.7%

- Core Durable Goods (ex-Defense & ex-Aircraft): +5.8% YoY in OCT, down from 6.8% YoY in SEP

- Core Capital Goods (ex-Defense & ex-Aircraft): +8.2% YoY in OCT, up slightly from +8.1% YoY in SEP

- Real PCE: +2.2% YoY in OCT, down slightly from +2.3% YoY in SEP

- University of Michigan Consumer Confidence: 88.8 in NOV, down from a preliminary NOV reading of 89.4

- Pending Home Sales: +2.2% YoY in OCT, down from an upwardly revised +3.4% YoY in SEP

- New Home Sales: +1.8% YoY in OCT, down from +14% YoY in SEP

Got #GrowthSlowing?

We know why most investors like surveys such as the [regional] Philly Fed Business Outlook or, worse, an “independent” research provider’s proprietary (READ: fabricated) assessment – they’re almost always bullish and they don’t require any work to interpret (i.e. no rate-of-change calculus, trend amalgamation, etc.)!

From our perspective, however, being lazy about the economic cycle at the all-time highs in the stock market seems like a risky proposition. We don’t get paid to be lazy and neither do you.

But, again, what the heck do we know? We’re just the guys that told you to Sell ‘Em in early-2008 and early-2011 too.

All told, long-term Treasury bond yields should continue to fall. And as rates fall, we want you to remain long of the long bond and defensive large-cap equities that resemble the long bond.

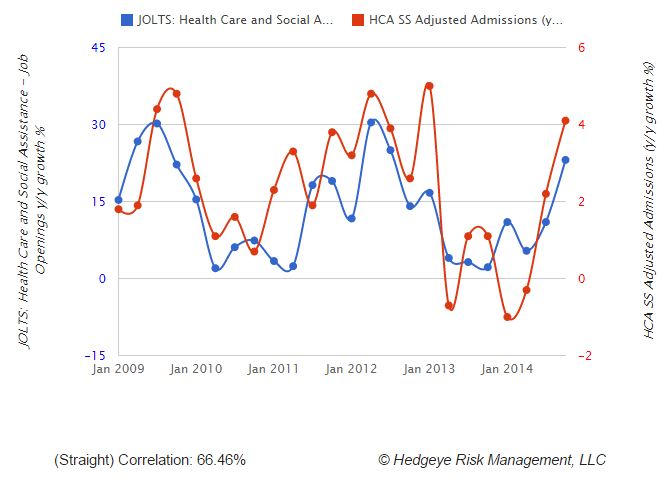

HCA

We spoke to HCA earlier this week and came away feeling good with our long position. We noted with interest a new slide in their recent presentation at CSFB (see below). We’re happy to see HCA using “macro” to talk to their buisness trends. Better still, the company said they were getting good interest from the buyside, which is more than we get.

We did notice that some of the items included on HCA’s macro slide are not particularly helpful in understanding the short or intermediate term modeling, and others are interrelated. HCA’s list may be helpful thinking longer term, but for the short term, our new huckleberry is the Job Openings and Labor Turnover Survey (JOLTS) for healthcare openings (chart below). We’ll include the series when we publish our Hospital Monitor next week with the Labor report.

Bottom line? After speaking to HCA, our takeaway is that 1.5% volume and 3.5% price (still) doesn’t feel like a stretch. If true, HCA shares can and should move higher from here.

RH

Hedgeye retail sector head Brian McGough has no update on Restoration Hardware this week.

* * * * * * * * * *

Black Friday Special

The markets are clearly in the hands of the Bulls. The Bullish / Bearish sentiment indicator continues to track at all-time bullish levels – leading us to wonder who will buy their stock when they all turn bearish – and markets are fully cooperating with the spirit of the season. It’s All-Time Highs, all the time!

Here are a few key metrics:

Employment: Market boosters are pounding gleefully away at the comparative strength in the employment numbers, which remain the best in many years. While remaining well below levels in recent years, seasonally-adjusted unemployment claims rose this week, making it three weeks in a row of erosion. And non-seasonally-adjusted claims numbers continue to improve, but the 4-week rolling average has slowed for the fifth straight week, and the rate of improvement has slowed to revert to its underlying trend. Simple math indicates that phenomena almost always Revert to the Mean; experience teaches that what goes up will almost certainly come down. Today the rate of improvement is no longer improving. Tomorrow, that rate will likely dip below the mean. That’s what “mean” means (note to Janet Yellen.)

Also note that unemployment figures are being compared to relatively higher than average levels. Yes, they are lower than they were last year, but this is an easy comparison. Meanwhile the marginal slowing of the rate of improvement indicates that the car of the US economy is slowly running out of gas.

Unemployment is a lagging indicator; by the time unemployment figures reach alarming levels, the damage in the economy has already been done. Hedgeye looks at the rate of change in the current comparisons, and that rate of change is slipping. Positive, but less positive than it has been.

Income & Spending: Hedgeye Macro analyst Christian Drake calls it “the great vanishing income growth of October 2014.” Estimates for personal income were revised for the April-to-September period with total disposable personal income shaved by some $200+ billion (SAAR) vs. prior estimates.

Alongside a meaningful downward revision to the savings rate in recent months, a net effect of the revision was a complete shift in the trajectory of salary and wage growth.

Whereas, prior to revision, the slope of aggregate private sector wage growth in 2Q/3Q was one of acceleration, after the revision, it shifts to one of flat-to-modest deceleration.

The Bureau of Economic Analysis releases these figures on a two-month lag, still longer after the CPI is calculated. But the Fed treats consumer income and spending as a coincident indicator, meaning they make policy based on the assumption that this represents current reality. In case you haven’t noticed, a lot can change in the economy in two months.

A second month of soft Durable and Capital Goods spending in October is signaling an inauspicious start for domestic consumerism in 4Q and is heralding a likely moderation in consumer credit growth as well. Positive, but decelerating, income growth, goods consumption and credit growth is not an escape-velocity factor cocktail. Hedgeye’s focus is this deceleration at the margin. A negative change in the rate of change.

Reliance on simple comparisons, whether in data points or in current rates of change, perpetuates a bullish narrative. But under the hood, the trend is in clear risk of going away.

A bubble is a self-contained pocket of air. A market bubble is a self-perpetuating pocket of high prices with no solid foundation. Look no further than the weakness in volume on up days in the averages for lack of conviction behind these record highs.

Markets can’t defy gravity forever. In time, erosion in the rates of change of key indicators will turn into actual changes in key data points. Then they’ll get it and the market gurus will be calling out negative reads in key indicators.

Position yourself early. You never know how many shopping days are left until the next major correction.

It’s awful to have to say We Told You So. It’s worse to have to say that we knew, and we didn’t tell you.

Happy Thanksgiving.