Labor Conditions Take a Small Step Backward

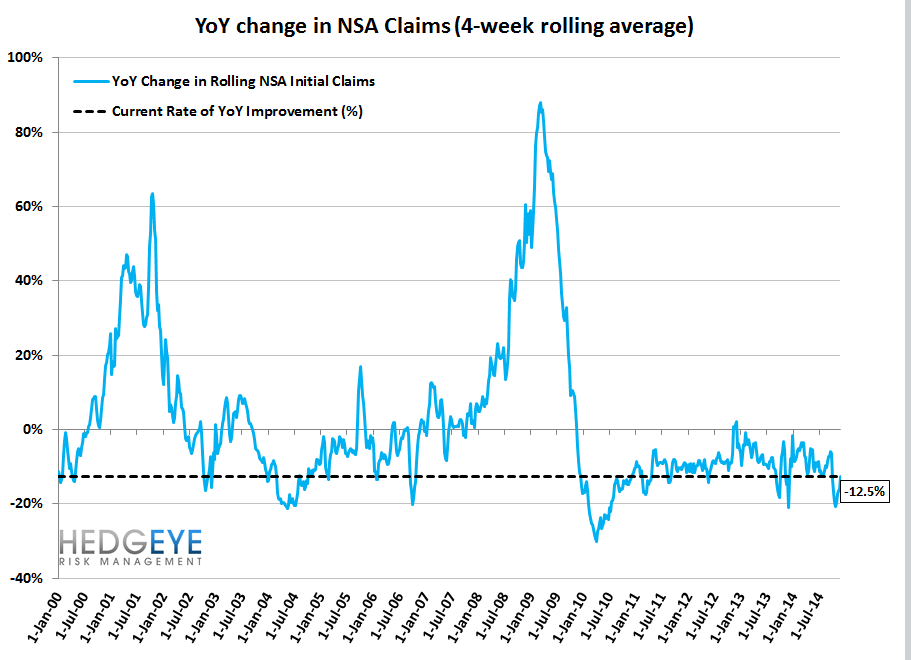

Rolling claims remain below the key 300,000 level. However, the one-week SA data shows the first peek above that level in 11 weeks. The rate of improvement slowed further this week to -12.5% y/y. The labor market remains healthy and is still improving, but at slowing pace.

The Data

Prior to revision, initial jobless claims rose 22k to 313k from 291k WoW, as the prior week's number was revised up by 1k to 292k.

The headline (unrevised) number shows claims were higher by 21k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 6.25k WoW to 294k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -12.5% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -15.9%

Yield Spreads

The 2-10 spread fell -8 basis points WoW to 173 bps. 4Q14TD, the 2-10 spread is averaging 184 bps, which is lower by -15 bps relative to 3Q14.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT