This note was originally published at 8am on November 12, 2014 for Hedgeye subscribers.

“Any intelligent fool can make things bigger, more complex, and more violent. It takes a touch of genius —and a lot of courage —to move in the opposite direction."

-E. F. Schumacker

The most challenging thing to do as a stock market operator is to make a trade or investment against consensus. If you are wrong for any period of time, you hear about it in spades. Especially in this day and age when every Jamoke under the sun has a soapbox and/or a twitter feed. (Admittedly, though, we do applaud the democracy that Twitter has brought to the media world!)

The fact is, the harder consensus leans, the higher your probability of being right in fading that view. Conventionally speaking, one way in which this is manifested is in value investing. Now, to some, value investing is about deep dive company analysis, which we get, but on a higher level it is really about the implications of company valuation. Simply put: when a company’s valuation is high, the prospects for its future are perceived as rosier than when the valuation is low. (That is a simplification, but you get the point.)

In effect, valuation is an opinion, so when the vast majority of stock market operators give a company a low valuation, their opinion of that company is low. Ironically, or not, this consensus opinion is consistently wrong over the long run. In fact, Dreman Value Management proved this in spades in a study of “cheap” stocks:

- First, the study showed that for the period of January 1st, 1970 to December 31st, 2010, stocks in the lowest P/E quintile outperformed stocks in the highest P/E quintile by a margin of 15.4% to 8.3% in terms of annual return;

- Second, in the 52 quarters when the S&P 500 declined between 1970 – 2010, low P/E stocks outperformed the market by an average of +2.4% versus an under performance of -1.9% for high P/E stocks; and

- Finally, from 1973 to 2010 the lowest quintile P/E stocks went up +1.2% on a negative surprise versus a return of -7.4% for the highest quintile P/E stocks on a negative surprise.

Now valuation is obviously only one factor, and not always the best factor for shorter term tactical trading, but over the long run it is a great gauge of the consensus opinions of companies. And over the very long run, fading well loved “names” as based on high P/E multiples has provided enormous outperformance.

Back to the Global Macro Grind...

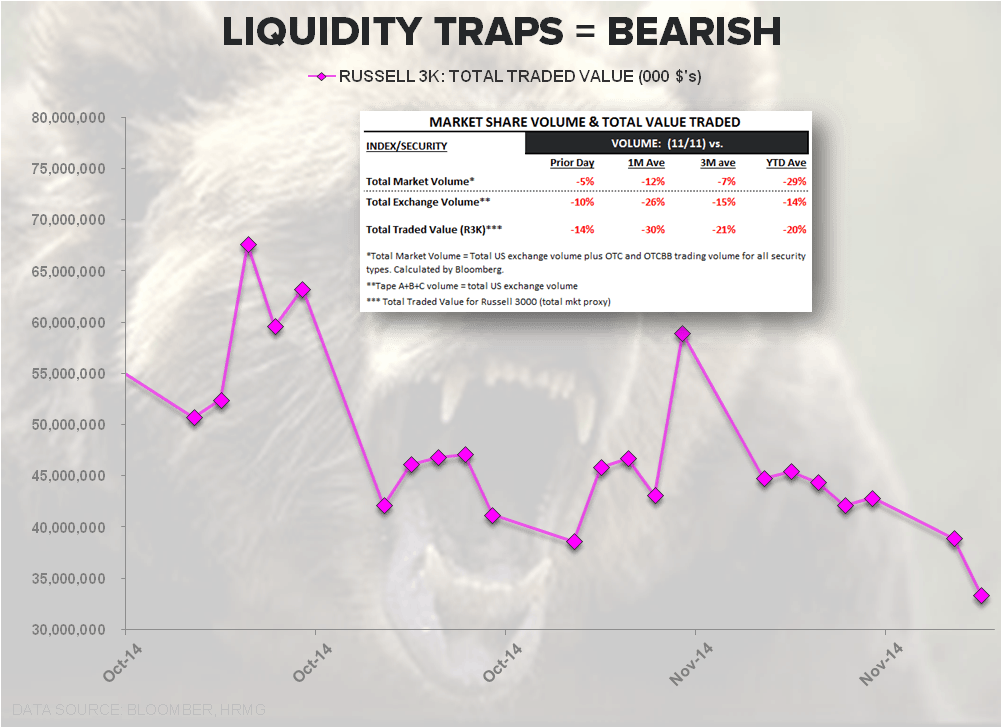

This morning it is not difficult to find the consensus view of U.S. equities. The II Bulll Bear Spread (bulls minus bears) is +99% to the bullish since October 12th. As well, Bears are tracking near all-time lows at 14.8%. If you are a lemming, of course, this makes sense. As markets go up you get more bullish and as markets go down you get more bearish. Practically speaking, as we highlight in the Chart of the Day, chasing this rally is fraught with risk given how unconvincing the volume has been.

Complacency seems to once again be setting into the view of European equity markets as well. We’ve seen a few notable chart followers suggest the turn is in for European equities and today they may have some fodder for the case with Eurozone Industrial production, which beat expectations.

Specifically, Eurozone September Industrial Production rose by +0.6% year-over-year versus the consensus view of -0.3%. This compared to the August reading, which was a -0.5% decline (also an upward revision from -1.9%). As well, the German economic minister was out this morning saying that the “German economy stabilized in Q3 after a Q2 contraction and now has slight upward momentum”. Now, of course, if this is the best the Eurozone can do, fading any rally is certainly worth considering.

Over at the Bank of England today, the honest Canadian, BOE Governor Mark Carney, is at least being forthright in saying, "it’s appropriate that markets now expect easier monetary conditions” based on the real-time growth and inflation data the BOE is seeing. The challenge with easier monetary conditions for many global central banks is that while they are not out of bullets, the bullets are increasingly ineffective.

Yesterday we hosted a call for our Institutional Macro subscribers with Professor John Taylor from Stanford on this very topic. Taylor is an outspoken advocate for rules based central banking (hence the eponymous Taylor Rule) and also highlighted in spades a point we’ve been harping on for some time, which is that the extreme QE monetary policy in the U.S. has became increasingly ineffective. As Taylor noted on QE3:

“When started 10-year Treasury was 1.7%, then rose and has remained higher

- Effects of QE on yield spreads

– 1-year vs 10-year US Treasury spread

– 2003-2008 non-QE period……1.3%.

– 2009-2013 QE period……………2.4%”

It obviously begs the question of whether the biggest no-brainer “Fade Trade” has become to fade the increasingly impotent global central banking regime? You likely already know our answer on that.

If you’d like to listen to the replay of our discussion with Professor Taylor, the replay and his presentation can be accessed below.

***Click here for Presentation Materials

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.26-2.39%

SPX 1965-2049

RUT 1135-1182

VIX 12.33-16.51

Yen 111.99-117.87

WTIC Oil 75.61-78.97

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research