Tax efficiency may not be Steve Wynn’s main incentive but it sure makes this IPO look attractive. If it weren’t for all those corporate/branding fees the IPO pricing, would be downright cheap.

From an investor’s perspective, we like the Wynn Macau IPO and would try and get as much stock as possible even at the high end of the stated range.

Not all EBITDA streams are created equal. Buying into WYNN’s Macau operations at the same multiple at which WYNN is trading is a deal in our opinion. The main reason? Macau has a 5 year corporate income tax holiday on gaming profits, which is likely to get extended in perpetuity. In the US, taxes are assessed at 35% of net income. That’s a big difference.

Presently the US only taxes repatriated income but over the long term, if one holds WYNN stock, the tax differential will come into play. President Obama and many democrats controlling Congress would like to tax ALL income at the US rate regardless of where earned or whether repatriated or not. That’s a subject for another post but it seems likely WYNN, LVS and many other US companies with significant international operations would domicile overseas in that case.

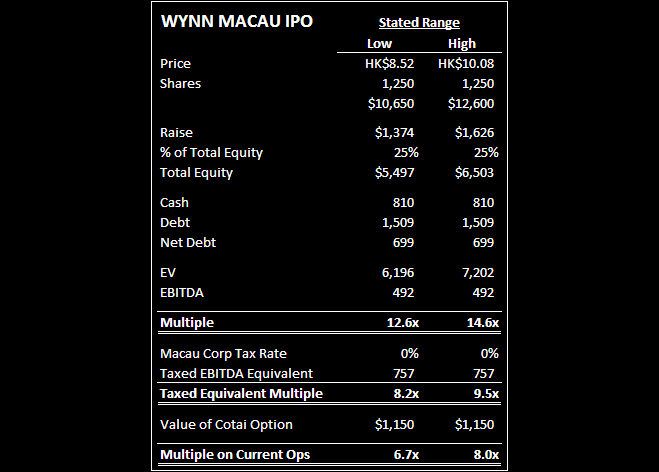

The following table attempts to equate taxable and non-taxable EBITDA streams to provide a better comparison. At HK$10.08 per share, the high end of the range, we calculate an EV/EBITDA multiple of 14.6x (EBITDA includes a full year of Encore). However, adjusting for the tax advantage, the multiple falls to 9.5x. On top of a 9.5x tax equivalent multiple of current operations, Macau IPO investors would also receive a free option on a Cotai development, worth $1.2bn in our opinion. Excluding this from the enterprise value yields an even lower multiple of 8x. Think how cheap it would be if WYNN wasn't charging the new entity over $60 million in branding fees on top of the $46 million in coporate allocations, design, marketing, and employment fees!

We can argue about whether there is a better way to account for the tax efficiency (free cash flow – see below) but there is no doubt that, all things held equal, buying into a Wynn Macau IPO is more attractive at the same multiple than buying WYNN in the US.

On a free cash flow basis, we calculate a yield of 6.7%. After adjusting the equity value for the Cotai option value, we estimate a “true” yield of 8.1% which is pretty attractive.

We’re hearing that they may close the books tonight with a 10/1 pricing. The IPO is oversubscribed and Hong Kong tycoons and long only funds are in the driver's seat. We think it will be a successful IPO and may even be worth a look when the stock commences trading.