“We should burn what wagons we have, on order that our cattle not be our generals.”

-Xenophon

According to ancient Greek #history, that’s what an emerging Athenian leader, Xenophon, told his men they should do as they marched against their Persian King. “Moreover, let us also abandon other superfluous baggage, except what we have for war or for food.” (Xenophon: The Anabasis of Cyrus, pg 108)

Yep. That’s the stuff I am reading these days. If you want to call it my confirmation bias in being bearish against central planning overlords (i.e. that this will not end well), I’m cool with that.

Buying the Long Bond (TLT) is as close as I am going to get to war with US and global growth bulls. And I probably won’t stop riding this bearish growth view, until the US elects to burn the yield chasing wagons – letting rates rise.

Back to the Global Macro Grind…

In case you didn’t know that one of the only ways out of this centrally planned Liquidity Trap (Total US Equity Market Volume was -29% versus its YTD avg yesterday) is to stop doing what didn’t work, now you know. Or at least the bond market does…

BREAKING (updated growth “survey” from Hedgeye): US 10yr Treasury Yield is ticking down to a fresh November low of 2.29% this morning and the Yield Spread (10yr minus 2yr yield) has compressed towards its 2014 YTD lows of 176 basis points this morning.

These are clean cut #GrowthSlowing signals. But you already know that.

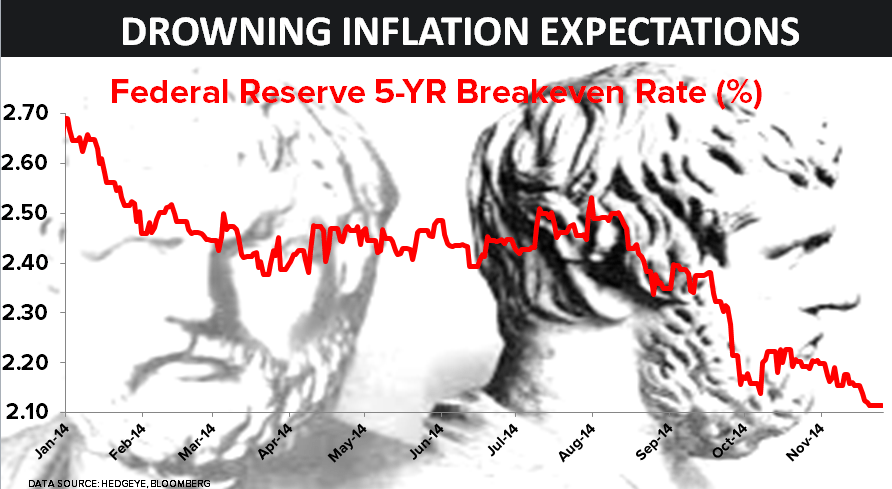

What you also know is that at this stage of the central planning war, equity markets going up really has nothing to do with real-growth anyway. It has everything to do with Japan, Europe, USA, China, etc. trying to resuscitate drowning inflation expectations.

On that real-time score, as you can see in today’s Chart of The Day (US TIPS, 5 year Breakevens), so far… no good.

While the 2 day China rate cut “pop” in everything inflation expectations that’s been dropping was fun to watch, it didn’t change #Quad4 Deflation expectations. Both global growth and inflation expectations are still slowing, at the same time.

Other than one of the Fed’s preferred ways to monitor #deflation expectations (Breakevens), here’s what else I’m looking at:

1. US Dollar Index vs both Burning Yens and Euros = +10% YTD

2. CRB Commodities Index -0.7% yesterday to -4.6% YTD

3. WTI Oil flattish this morning at $76.01, down -17% YTD

4. Copper flat this morning at $3.01/lb, down -10% YTD

5. Russian Stocks (RTSI) -1.2% this morning to -23.3% YTD

6. Energy Stocks (XLE) down (again) -0.8% yesterday to -0.8% YTD

Then, of course, you can look at some late-cycle stuff like US wage Inflation… where 2/3 of the country has seen real wages deflate since the Fed undertook their unprecedented Policy To Inflate (see Federal Reserve’s own papers on the matter for details).

Or you can just find a “survey” that tells you something that has been the complete opposite of the wage deflation and no-capex cycle data. And say that the “market is up” on something like that.

But when you say “market” don’t forget that my preferred risk adjusted market to be long in 2014 (Long Term Treasuries) has had a much higher absolute return on much lower realized volatility than US small/mid cap stocks have.

Even if the July to October +160% ramp in the VIX is forgotten (for now), that doesn’t mean that the non-linear and interconnected economic risks associated with #Deflation Expectations Rising cease to exist.

What also exists as of this week is non-survey computed options positioning in Global Macro (non-commercial CFTC futures and options consensus positioning):

1. SP500 (Index + Emini) has moved to its biggest net LONG position since late SEP at +29,110 contracts

2. Long Bond (10yr Treasury) hit its biggest net SHORT position of 2014 at -128,032 contracts

3. Oil still has a net LONG position of +276,213 contracts, only down -12,971 week-over-week

“So”, what does that tell us?

1. After shorting the OCT lows, hedge funds have covered their shorts and are chasing the bull run in SPY (again)

2. Consensus Macro continues to think the risk in interest rates is to the upside (we reiterate downside!)

3. Perpetual expectations for another central plan (OPEC) remain for a non $65 oil price

Since Consensus Macro is not my expectations general, I say you burn the groupthink wagons and do the exact opposite of where those options are positioned: BUY Long Bond (TLT, EDV, etc.), and SHORT SP500 (SPY), Oil, and its related stocks and bonds.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.28-2.34%

SPX 2018-2072

RUT 1154-1190

EUR/USD 1.23-1.25

Yen 117.03-119.16

WTI Oil 73.04-77.51

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer