TODAY’S S&P 500 SET-UP – November 25, 2014

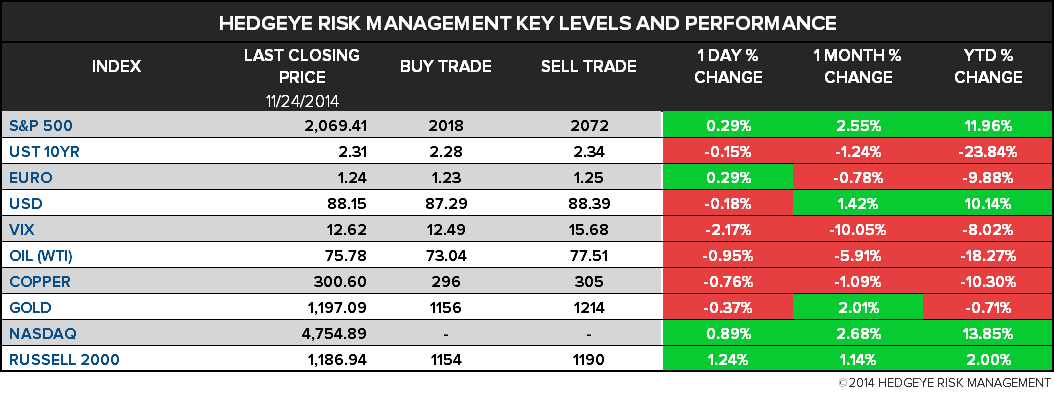

As we look at today's setup for the S&P 500, the range is 54 points or 2.48% downside to 2018 and 0.13% upside to 2072.

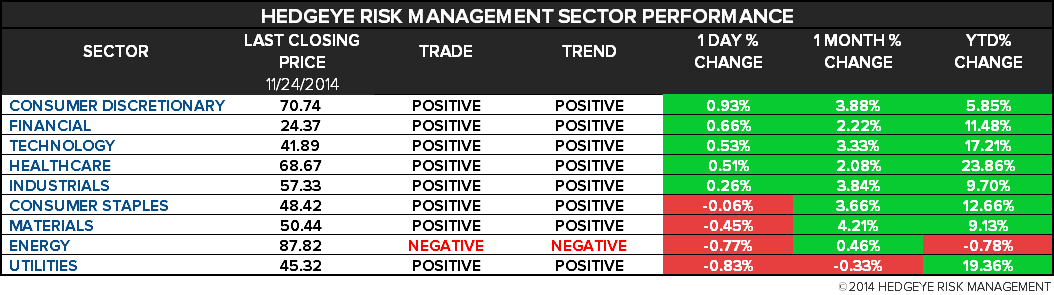

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.81 from 1.81

- VIX closed at 12.62 1 day percent change of -2.17%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: ICSC weekly sales

- 8:30am: GDP, 3Q, est. 3.3% (prior 3.5%)

- 8:55am: Redbook weekly sales

- 9am: FHFA House Price Index, Sept., est. 0.4% (prior 0.5%)

- 9am: S&P/Case-Shiller 20 City Comp y/y Sept, est. 4.6% (prior 5.6%)

- 10am: Consumer Confidence Index, Nov., est. 96.0 (prior 94.5)

- 10am: Richmond Fed Mfg Index, Nov., est. 16 (prior 20)

- 11:30am: U.S. to sell $13b 2Y FRN in reopening, $40b 4W bills

- 1pm: U.S. to sell $35b 5Y notes

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- House, Senate out of session

- Obama travels to Chicago to talk with community leaders

- 10am: FDIC Chairman Martin Gruenberg holds briefing on bank, thrift industry earnings for Q3 of 2014, followed by Q&A

WHAT TO WATCH:

- Ferguson Explodes in Protests After Officer Avoids Charges

- Honda May Face Record Fine for Underreporting U.S. Claims

- Bayer Said to Weigh Diabetes Unit Sale for Up to $2.5 Billion

- Lew Says Tax-Break Extension Plan in Congress Is Irresponsible

- Caesars Lenders Said to Agree on Making Unit a Real Estate Firm

- Glencore-Rio Merger Will Happen, Banker Hannam Tells Funds

- FDA to Release More Labeling Rules on Calorie Counts

- Universal Pictures Picks Up Steve Jobs Film Project From Sony

- CME’s Market Surveillance Found Lacking by Its Chief Regulator

- ‘Frozen’ Overtakes Barbie as Holiday Season’s Most Popular Toy

- U.S. Prosecutors to Interview London FX Traders: Reuters

- Wal-Mart Chief Merchandising Officer Set to Leave, WSJ Reports

AM EARNS:

- Alimentation Couche-Tard (ATD/B CN) 8:42am, $0.56 - Preview

- Beacon Roofing (BECN) 8am, $0.61

- Brown Shoe (BWS) 7am, $0.68

- Campbell Soup (CPB) 7:15am, $0.72 - Preview

- Chico’s (CHS) 7:31am, $0.17

- Cracker Barrel (CBRL) 7am, $1.29

- DSW (DSW) 7am, $0.52

- Eaton Vance (EV) 9am, $0.64

- Hormel (HRL) 6:30am, $0.64

- Movado (MOV) 7am, $0.86

- Pall (PLL) 7am, $0.80

- Signet Jewelers (SIG) 7am, $0.18

- Tech Data (TECD) 6am, $1.02

- Tiffany (TIF) 7am, $0.77 - Preview

- Valspar (VAL) 7:30am, $1.15

- Yingli Green Energy (YGE) 7am, ($0.14)

PM EARNS:

- Analog Devices (ADI) 4pm, $0.68

- Cubic (CUB) 4pm, $1.14

- Hewlett-Packard (HPQ) 4:04pm, $1.06 - Preview

- Infoblox (BLOX) 4:05pm, $0.02

- Nimble Storage (NMBL) 4:01pm, ($0.16)

- Perfect World (PWRD) 5pm, $2.77

- TiVo (TIVO) 4:15pm, $0.07

- Veeva Systems (VEEV) 4:02pm, $0.08

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Talk of Russian Oil Cuts to Help OPEC Likely to Stay Just That

- Brent Crude Gains on Speculation of OPEC Output Cut; WTI Rises

- Oil Boom Triggering Cowboy Shortage Across Canada: Commodities

- China’s Gold Imports Rise for a Third Month on Jewelry Sales

- Codelco Said to Trim 2015 Copper Premium to Japan Buyers by 2.5%

- Iron Ore Drops Below $70 for First Time Since ’09 as Glut Widens

- Palm Oil Exports From Indonesia Seen Dropping From Six-Year High

- OPEC Said to Mull Sparing Iraq, Iran and Libya From Oil Cuts

- Steel Rebar Rises From Record Low on Restocking Demand Optimism

- Soybeans Rebound on Signs of Rising Demand for Record U.S. Crop

- China Cotton Imports in 2014-15 Seen at 1.3M Tons, Butler Says

- Venezuela Turmoil Signals End of Oil-for-Jeans Giveaway: Energy

- EU Parliament Unlikely to Propose Early Carbon Reserve: Sikorski

- Plunging Cotton Prices Spurring Farmers to Reduce Planting

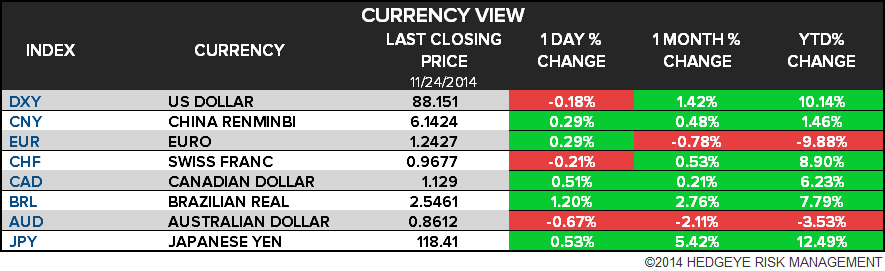

CURRENCIES

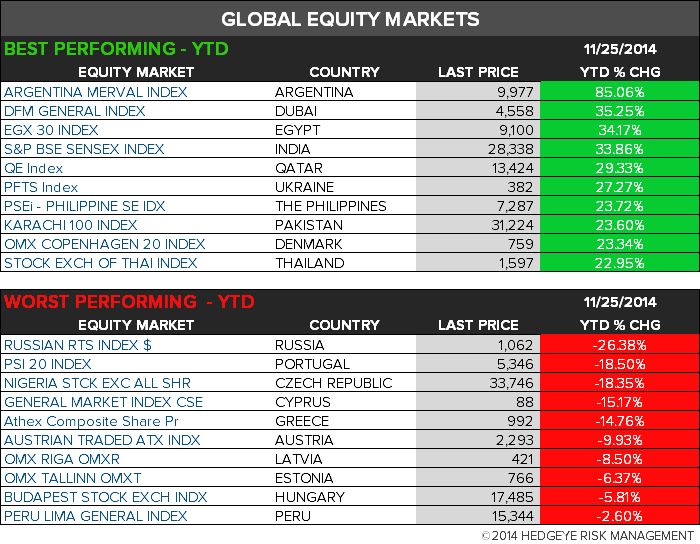

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

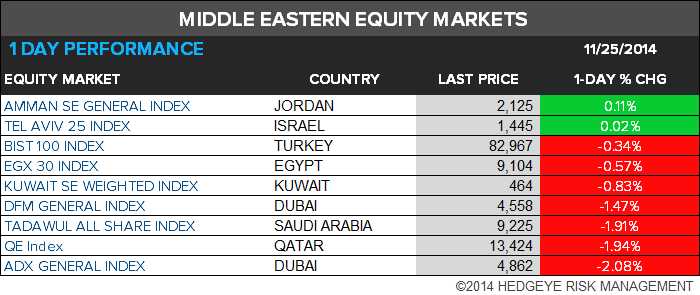

MIDDLE EAST

The Hedgeye Macro Team