Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email

------

European Financial CDS - Swaps mostly widened in Europe last week, although the median change was only 2.3%. Portugal's Banco Espirot Santo swaps led the rise, gaining 48 bps to end the week at 500 bps. Sberbank of Russia and Austria's Erste Group Bank followed, gaining 33 bps and 10 bps respectively.

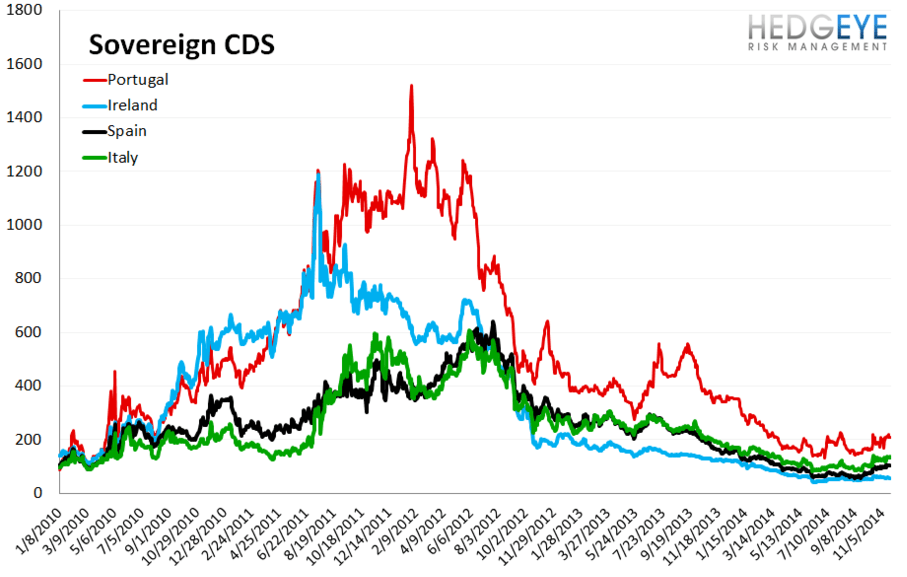

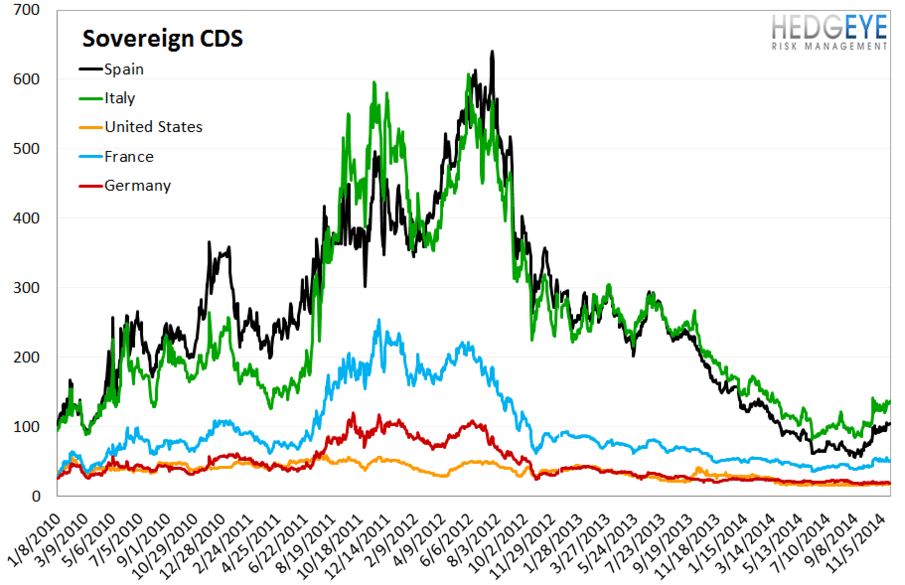

Sovereign CDS – Sovereign swaps mostly tightened over last week. German sovereign swaps tightened by -6.8% (-1 bps to 19 ) and Italian sovereign swaps widened by 0.8% (1 bps to 138). Japanese CDS widened by 10.7% (+6 bps to 60) on news that Japan is in recession and Prime Minister Shinzo Abe will delay a tax hike by one year. The delay has caused investors to worry about the country's solvency.

Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 1 bps to 9 bps.

Matthew Hedrick

Associate

Ben Ryan

Analyst