Below are Hedgeye analysts’ latest updates on our six current high-conviction long investing ideas.

We also feature two pieces of content from our research team at the bottom.

*Note: We will send CEO Keith McCullough’s updated levels for each investing idea at the beginning of this coming week.

CARTOON OF THE WEEK

IDEAS UPDATES

TLT | EDV | XLP | MUB

With the exception of a few noteworthy [bullish] housing data points and [outrageously incongruent] regional surveys, the critical economic releases from this week continue to support our view that both growth and inflation are slowing simultaneously:

- Industrial Production: +4% YoY in OCT vs. +4.2% in SEP; down -0.1% MoM vs. Bloomberg consensus expectations of a +0.2% increase

- Headline PPI: +1.5% YoY in OCT vs. +1.6% in SEP

- Headline CPI: unchanged at +1.7% YoY in OCT; for the quarter-to-date, CPI is tracking down -10bps from the 3Q average

- Markit Manufacturing PMI: 54.7 in NOV vs. 55.9 in OCT; this marks the lowest reading since JAN and down for the third consecutive month

Calling for continued disinflation is a trivial matter at this point (CLICK HERE to review why).

Growth bulls, however, will accuse us of cherry-picking #GrowthSlowing data. In the spirit of pre-empting that (we play chess, not checkers @Hedgeye), we thought we’d take this moment to highlight the trending rate of change across the broad spectrum of key economic indicators:

As you can see, the vast majority of the key economic indicators are slowing quite ardently.

When growth slows, we like the long bond (TLT, EDV, MUB) and equities that can give us a yield (i.e. XLP, XLU and XLV). With a likely [bullish] #Quad1 setup coming down the pike in 1Q15, this research recommendation of ours is admittedly long in the tooth.

That being said, however, we see no reason to back off the thesis now. Anyone who’s followed our investment advice to be long of bonds and slow-growth, yield-chasing in the equity market is clearly having a great year:

Specifically, we still expect to see the final crescendo of consensus capitulation on the short side of Treasuries in the coming weeks.

Furthermore, we think the worst thing you can do right now is sell these winners to rotate into the Consensus Macro playbook of buying early cycle stocks up here. We think you’ll get a much better opportunity to rotate in #Quad1 from lower prices in the coming weeks.

If we’re wrong on that, we’ll be wrong on that. But the process stays stick with the current playbook – especially when the data supports it!

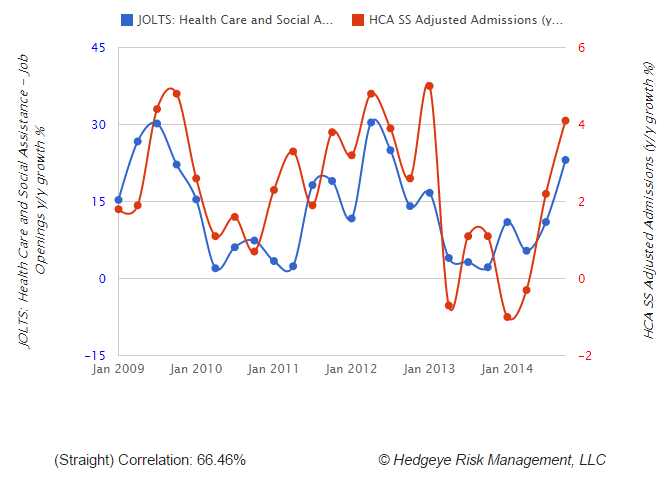

HCA

The long position in HCA comes down to two assumptions: 1-2% volume and 3-4% price. If those are reasonable assumptions, HCA is going much higher. It would seem consensus is expecting much worse.

On volume, we’ve talked previously about the importance of maternity trends to hospitals, and HCA is no exception. We assume their strong volume growth in 3Q14 was driven largely by an increase in births as well as newly insured people coming on from Health Reform. We are slightly cautious in the short term as two data series reflecting recent maternity strength are sliding toward weakness in the last few updates. We’re also seeing good patient visit trends, and within two time series we began using recently, strong hiring and capital spending among providers, both of which reflect strong demand in our view. SO maybe if maternity slows, other trends will pick up the slack. If we see orthopedic cases continue to accelerate, and a higher mix of high priced ortho cases, the positive impact on our pricing assumption will be substantial, and 3-4% price will prove to be low.

Below is a chart that shows how many jobs in healthcare remain open versus HCA’s same store volume growth. It would seem 1-2% volume is not a stretch goal.

RH

Restoration Hardware shares were up 6% this week for two reasons. 1) The bullish read-through we received this past week from the Williams-Sonoma print and 2) the RH Atlanta store opening.

1) Keep in mind that Williams-Sonoma turned out to be an excellent directional indicator for RH last quarter. WSM putting up great top line numbers augurs well for RH shares.

2) As far as Atlanta is concerned, the store opening there is more than your average store. Legacy stores are 8,000 sq ft. Design Galleries are 20,000. This one is a whopping 65,000 So, despite the fact that it's only one store on a base of 68, it's really the equivalent of adding 6 new stores.

And as it relates to size, our RH real estate deck specifically quantified why Atlanta is a market that could support a store as big as 90k ft. Translation = it's definitely not too big for this market.

ADDITIONAL RESEARCH CONTENT BELOW

* * * * * * * * * *

JAPAN: does THE "ABENOMICS TRADE" HAVE MORE ROOM TO RUN?

We’ve been dead wrong on Japan over the past month or so. With the exception of one MAJOR caveat, consensus probably has this trade right.

EMERGENT HOUSING MOJO

Existing Home Sales joins the bullish housing party, alongside NAHB (Tuesday) and Housing Starts & Mortgage Apps (Wednesday).