My tune on Nike remains the same. It’s all about duration with this name. This company is setting up to be a big winner – but not yet. The consensus is clearly negative (only 53% buy ratings – lowest in history) and estimate dispersion is at an all time high, but at the same time seems to share the view that after this quarter, Nike is back to the races (easy revenue compares, etc…). I think that the consensus is wrong not once, but twice; 1) the Street is 2-3 quarters too early in any assertion that the worst is behind NKE, and 2) based on how Nike is resetting its chessboard, I also think that the Street is not bullish enough on the financial impact when the engine restarts. Again, pick your duration wisely.

Fundamentally, there aren’t a whole heck of a lot of reasons I can point to today that make this name attractive to anyone with a duration shorter than 1 year. Growth is slowing, and despite the Street’s estimate that suggests business is turning up (even though sentiment stinks, the math does not lie), my sense is that growth might not yet have put in a bottom.

In fact, I’m at $0.95 for the quarter vs. the Street at $0.98. To be clear, Nike has not missed a quarter since May ’03 and Feb ’02 – each time it missed by a penney. This company does NOT like to lose, and does not take misses lightly – even if they themselves did not set the expectation (no guidance). Can they find wiggle room this time? Yeah, of course they can. But they’re compensated to hit annual internal targets – not quarterly Street consensus. Meaningful upside this quarter will need to come from a windfall in SG&A or non-operating income as opposed to revenue to beat my number.

For the year, I’m roughly in-line with the consensus $3.55, but barring a similar windfall, my bias is to the downside. That said, what are we talking… $3.25, $3.35??? That’s as bad as it’s gonna get. I’m pretty darn sure of that. The reality is that the company is doing what it SHOULD be doing, which is investing in its brands to take share as we come out the other end of this cycle, instead of what Wall Street WANTS it to do, which is showing outsized pre-tax income margins from cost saves. The stock won’t go up if $3.25 is a reality (suggesting 18x today), but will be a great setup for those who want to participate in the next multi-year period of wealth creation in this business.

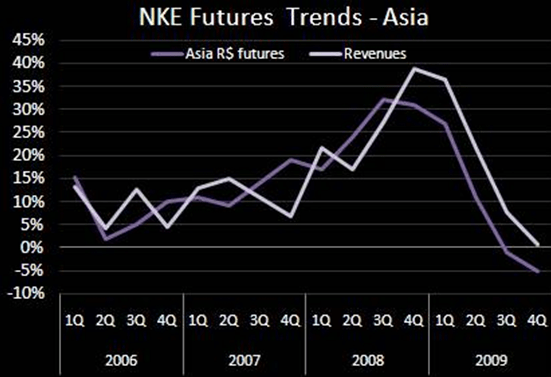

What is it setting up for? Those students of Nike history know how the company has a burst of growth, and then cools off, resets the organization, and then bursts again. This happened between EVERY stage of Nike’s evolution from a $10mm running shoe company in the 1970s, to a $19bn global powerhouse today. But each reset is incrementally more complex than the last, and therefore takes longer. We are currently 9-months in to what I think will be an 18-month reset. That’s been my call here for 2-quarters now.

We’re going to begin to see the meaningful acceleration in top line in fall of ’10. That means it shows up in futures around Spring 10. No, that’s not too far away. But until then, there will continue to be fits and starts. What do I define as a ‘fit or start’? Sales or futures shifting 2-4% in either direction. The market will fight over finding the datapoints ahead of time. But the REAL call will be there when the organization has fully reset, SG&A dollars fully allocated and amortized, capex creeps lower, customer connection strengthens, orders accelerate, revenues grow by 10%+, inventories decline by 5-10%, margins break through former peak, and the path beyond $5 in EPS becomes crystal clear. I’m certain that there is only one global brand that has this set up. If I were Nike’s competition, I’d be very afraid of the setup – very afraid.

Given that there’s still a full product development cycle between today and when I think business will pick up, I need to more heavily discount the potential for any unforeseen company or industry events. Two come to mind. I’m not trying to be alarmist here, but risk management is the key.

1) As it relates to company specific drivers, one factor I’m paying closer attention to today is the product pipeline. I’ve always thought that this portfolio can’t be disrupted by a single product, initiative, or region. But one angle is that there was a 4-month time period (Feb-May) where there was uncertainty within the organization as Nike shed 5% of its workforce. My understanding is that few people were ‘left hanging’ with a major question mark, but it was a dynamic inside the company that we can’t ignore. The development and sales window averages about 9 months, which suggests we’ll be seeing over the next few months the result of what could have been lower productivity levels 9 months back (even though they have since improved).

2) I can’t shake the ‘Ken Hicks Factor’ (new CEO of Foot Locker) from my mind. He’s due to come out with his 100 day plan (or something along those lines), and who’s to stop Foot Locker from closing a quarter of its US stores? I can make a very good case as to why it should. This will largely not impact Nike’s end-demand. But I’d argue that FL is Nike’s best off-balance sheet asset. Any store closures would be bad. Again, I’m worried about this less the closer we get to Spring ’10. But that’s a ways off…