Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today's Focus: October Existing Home Sales

EHS topped off three-days of strong housing data with a sequential gain of +2.5% up to 5.26M units SAAR – the third consecutive month of gains and the highest level in 13 months.

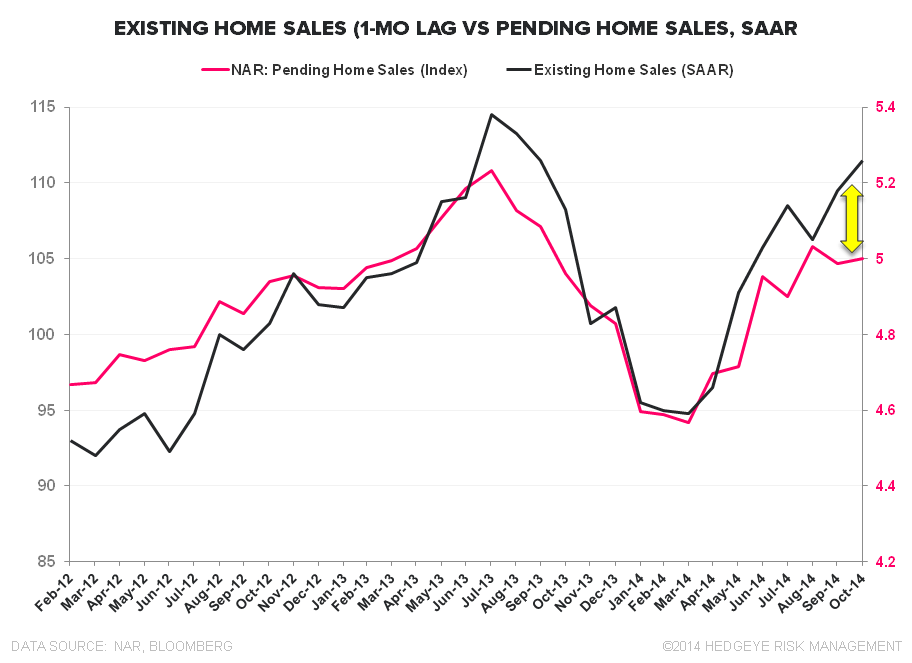

Generally, there's limited usefulness in the EHS report on the sales side since the data is well-telegraphed by the Pending Home Sales report a month earlier. However, we’ve seen EHS diverge from the more modest gains in PHS the last couple months – a trend we’re seeing on the new home side as well with New Home Starts positively diverging from Permits in Sept/Oct. The two series are tethered, so unless we see a positive revision and/or sizeable increase in PHS for October, its unlikely we see a gain of similar magnitude in existing sales next month.

Looking at the recent historical data, the direction of convergence between EHS and PHS after a period of divergence isn’t consistent. As can be seen in the 2nd chart below, EHS re-coupled to PHS to the downside in 2H13 while, conversely, PHS played catch-up to EHS mid-year this year.

TOTAL EHS: Total EHS rose +2.5% MoM to 5.26M Units SAAR, marking a third month of gains and the highest level since September of last year. Notably, sales turned positive on a YoY basis (+2.5% YoY) for the first time in 12 months. As we’ve been highlighting, we continue to expect improvement in rate of change measures on the volume side as we traverse the peak collective impact (ie. easiest comps) of weather, QM implementation and FHFA loan limit reductions into 2H15.

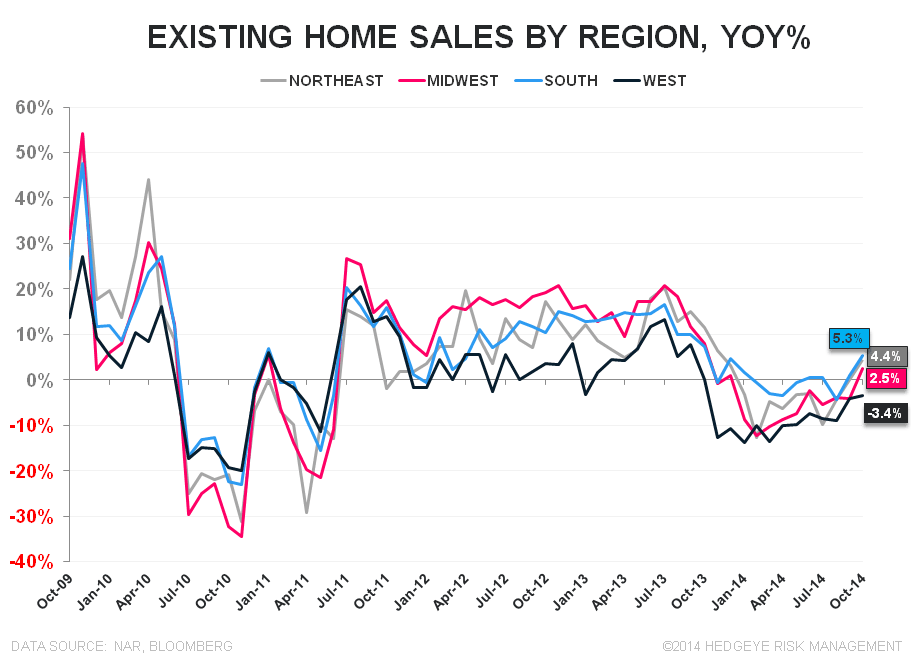

REGIONAL: All regions except the West reported both sequential gains and positive year-over-year growth in sales. All regions reported positive YoY growth in median prices with all except the Northeast registering accelerating price growth.

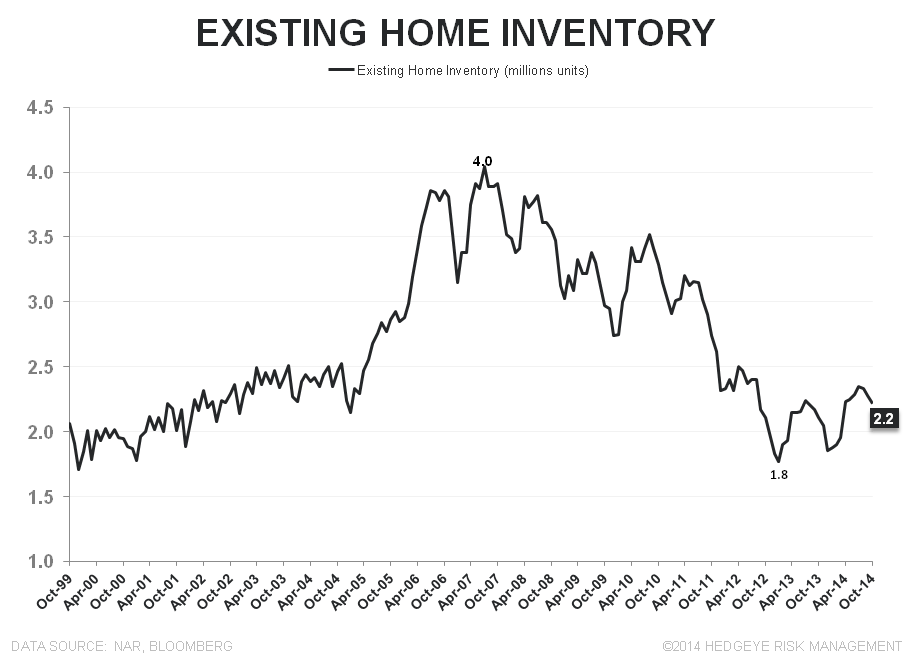

INVENTORY: Inventory remains relatively tight and should help buttress the moderation in prices. On a Unit basis, inventory declined -2.6% MoM to 2.22M, the 3rd month of decline and lowest level since March. The confluence of rising sales and lower inventory took months supply down -4.1% sequentially to 5.06 months.

DISTRESSED/CASH/1st-timers: First-time homebuyers held at 29% of sales for the 4th straight month and, on an annual basis, remain at the lowest level in three decades. All-cash sales increased to 27% from 24% prior while Distressed Sales declined to 9% vs 10% in October and 14% a year ago.

About Existing Home Sales:

The National Association of Realtors’ Existing Home Sales index measures the number of closed resales of homes, townhomes, condominiums, and co-ops. Existing home sales do not take into account the sale of newly constructed homes. Existing home sales account for 85-95% of all home sales (new home sales account for the remainder). Therefore, increases in existing home sales tend to signify increasing consumer confidence in the market. Additionally, Existing Home Sales is a lagging series, as it measures the closing of homes that were pending home sales between 1 and 2 months earlier.

Frequency:

The NAR’s Existing Home Sales index is published between the 20th and the 22nd of each month. The index covers data from the prior month.

Joshua Steiner, CFA

Christian B. Drake