The accountability pants are fitting pretty snug for us on TGT today. We’ve been on the wrong side of a 15% spike over the past month, which is a lot for a low beta name like Target. Any time an event goes against us like this, we always step back and re-evaluate our positioning. But the way we look at it, the thesis here still holds. Consider the following…

This is one of the most expensive names in retail relative to its underlying growth. We’re looking at 20x ’15 earnings and 9x EBITDA. If you assume that Canada losses go away entirely, and that TGT gets a billion in cash for the leases, it is still trading at 16.5x EPS and 8x EBITDA. While valuation is hardly a catalyst, barring an acceleration in the US Consumer or a rebound in the Canadian business, we can’t see TGT pushing all-time highs and peak valuations when we’re in year 6 of a retail margin expansion cycle.

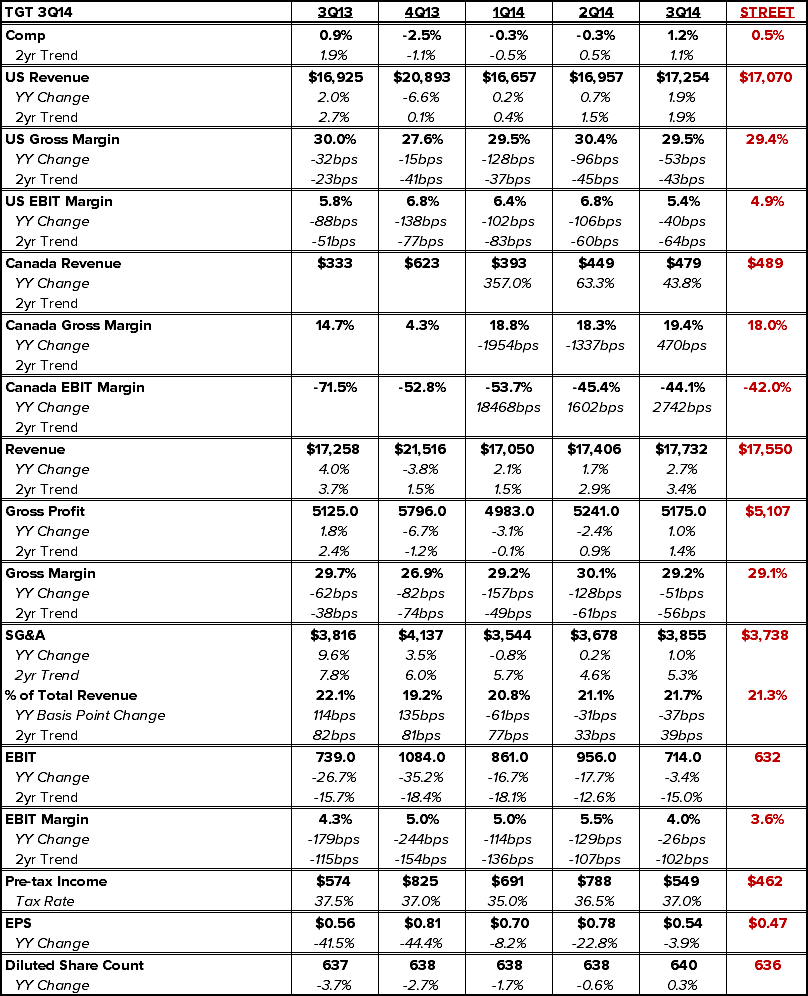

Let’s consider the dramatic change in expectations. Back in August when TGT was trading at $60, the company lowered full year guidance by $0.50 to about $3.20 for the year (midpoint). Since then, the stock has gone up by $10 (outperforming the market by 14%), the company is de-leveraging lackluster sales growth into a year/year earnings decline. Could TGT come in a nickel ahead of sandbagged guidance in 4Q? Sure. But it will still be earning $0.40 (11%) less than when the stock was $10 lower.

People like the big guide-down the company offered up three months ago as it serves as a cushion heading into the holiday for TGT to be more aggressive in discounting, offering free shipping, and ultimately taking share – even if it’s earnings dilutive. In fact, this quarter, sales were up +2.7% and yet EBIT was -3.4%, despite an improvement yy from Canada.

We think next year is key. The Street is at $3.80. TGT hasn’t given any guidance there yet. If we assume Canada gets 25% better next year (i.e. it gets back about $0.20 in earnings that it cost this year), then it suggests that the Street is looking at 12% earnings growth in the core business. With no square footage growth, a prescedent for buying comp, virtually no reason to think that gross margins will improve, and Brian Cornell likely to invest more SG&A to accelerate share gain in the outer years, we simply can’t get close to the Street’s numbers. It seems to us that Canada has returned to being the key variable in the earnings