This note was originally published at 8am on November 05, 2014 for Hedgeye subscribers.

Horatio: He waxes desperate with imagination.

Marcellus: Let’s follow. Tis not fit thus to obey him.

Horatio: Have after. To what issue will this come?

Marcellus: Something is rotten in the state of Denmark.

-From Shakespeare’s “Hamlet”

Undoubtedly in Republican circles there are a lot of celebrations going on today. After all, according to the scoreboard, they handed President Obama and his party a decisive loss.

In the Senate, the Republicans have already won a confirmed +7 seats and the count currently stands at 52 seats for the Republicans, 43 seats for the Democrats, and 2 seats for Independents. There are still three races that are considered undecided.

In the undecided races, it appears that Democrat Mark Warner will ultimately prevail in Virginia as he has the edge (though the margin is less than 13,000 votes and Republican Ed Gillespie has the option of a recount.) Meanwhile in Alaska, it appears that Republican Mark Begich will ultimately prevail as he has received 49% of the vote with 97% of votes having been counted. Finally, Louisiana is headed to a December run-off between incumbent Senator Mary Landrieu and Republican Bill Cassidy.

So in the Senate, Republicans will gain a minimum of +7 seats and perhaps as many as +9 seats. In the House, the Republicans have already gained a net +13 seats to solidify their majority with approximately 19 seats still considered undecided. In Governor mansions across the nation (outlined in the map below courtesy of Politico) Republicans also solidified their hold on state capitols.

According to Politico, “even optimistic Republican operatives didn’t anticipate this”, but to be fair, as we wrote yesterday in an intraday note, almost every major media outlet was predicting a decisive Republican victory. And decisive it was. In large part this victory can be attributed to the fact that exit polls showed President Obama’s approval rating at a dismal 41%.

In our view, the bigger story from the election is really how despondent Americans have become about the future of America. According to the exit polls, 2/3s of voters think the country is on the wrong track, a mere 22% believe their children will be better off than them, and more than 72% worry about a terrorist attack on American soil. That is just plain sad.

But, the fact that Americans are despondent about the future shouldn’t really be a surprise. This election was characterized by negative attack ads. In the 34 states with Senate seats up for grabs, there were 1 million TV ads shown and more than 46% of them were attack ads. While on one hand those ads were seemingly successful in leading the Republicans to victory, on the other hand, what was the cost?

Heading into the election, Congressional job approval was a mere +12%, with more than 80% of voters disapproving of the job that Congress is doing. As well, consistent with exit polling data above, heading into the election a mere 28% of voters believe that the country is headed in the wrong direction.

So, was this a resounding Republican victory? Perhaps, but the bigger issue we all have to deal with is that something is truly rotten in the District of Columbia.

Back to the Global Macro Grind...

As depressing as the state of U.S. politics may be this morning, there is always a bright side. The bright side is that we all live in America and can, if we set our minds to it, fix some of the endemic problems, such as distrust in our politicians. In countries like Russia, of course, the people have much, much less influence.

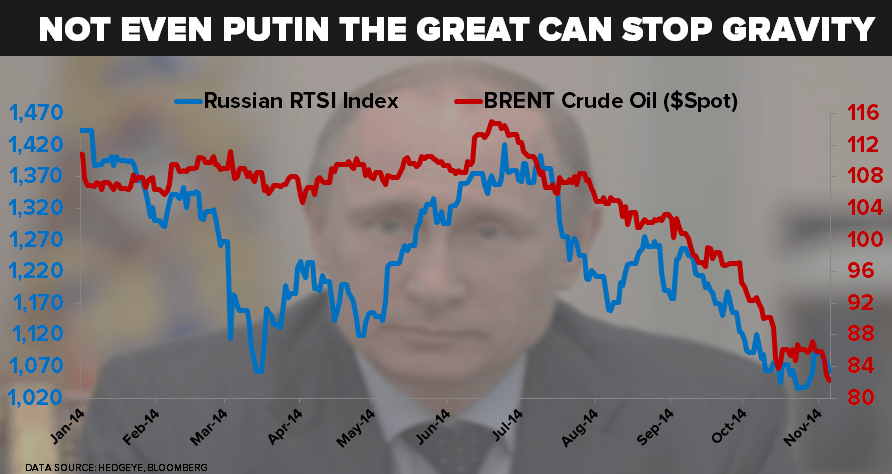

While certainly being a voter in Russia would be depressing, even more depressing would have to have been being invested in the Russian stock market this year. Specifically, for the year-to-date the benchmark Russian equity index is down -25%. Coincidentally, or not, the price of Brent crude is down right around -25% for the year-to-date as well.

As many of you know, we are big fans of looking at stock prices as leading indicators, which begs the question: what is the Russian stock market signaling? Since the market is in full on crash mode, it is truly fair to consider whether the market is signaling a somewhat imminent collapse of Putin’s Russia. While raising interest rates to strengthen the Ruble is a cute trick, the fundamentals of Russia remain highly dependent on energy exports.

According to the Energy Information Administration, in 2013 a full 68% of Russian exports, or more than $350 billion dollars, came from energy, with more than half of that from crude oil. For comparison, the United States exports no crude oil and petroleum products comprise a mere 8%. Given this dependence, it is really no surprise that in 2009, after crude oil declined by 80% in 2008, that the Russian economy shrunk by 7.8% in 2009, the most of any G20 economy.

Tomorrow at 1pm eastern we are going to be hosting a conference call for our institutional macro clients with former U.S. Ambassador to Russia Michael McFaul. (Email us at sales@hedgeye.com for details.) Mr. McFaul has been called, “the leading scholar of his generation, maybe THE leading scholar, on post-Communist Russia.” He was President Obama’s chief advisor on Russia through his first term and was a main policy architect of “Reset” in U.S. - Russian relations.

A high-profile figure during his time in Moscow, McFaul was harassed and accused of orchestrating a coup. Perhaps in light of his considerable work and reputation as an expert on anti-dictator movements and revolutions, Putin reportedly stared at McFaul across a meeting table and remarked, “We know that your Embassy is working with the opposition to undermine me.”

We hope you can join us for the call tomorrow, which will help illuminate exactly what is happening in Putin’s Russia. And remember, as depressing as some of the election exits polls, things are still worse in Russia.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.21-2.38%

SPX 1967-2033

VIX 13.41-17.80

USD 86.31-87.65

Yen 109.11-114.91

WTI Oil 76.43-80.51

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research