This note was originally published at 8am on November 04, 2014 for Hedgeye subscribers.

“Write down, therefore, what you have seen, and what is happening, and what will happen afterwards.”

-Revelation 1:19

No, I’m not going all religious on you this morning. That’s the opening volley from Jim Rickards in his recent book, The Death of Money. For those of you who missed it, I had a Real Conversation @HedgeyeTV with Rickards earlier in the year that you can watch here.

Do you write it down? What is “it”? And what do you do when something macro is happening that hasn’t happened for a very long period of time (like #deflation)? Once market expectations go through a phase transition from inflation policies to deflation, what will happen afterwards?

I’ve been writing down real-time market quotes, data, research, etc. in my notebook for 15 years and I have only seen versions of what I have been writing down for the last 10 months 2x: October 2007 and October 2008. Neither were bullish historical reference points and neither were the same.

Back to the Global Macro Grind…

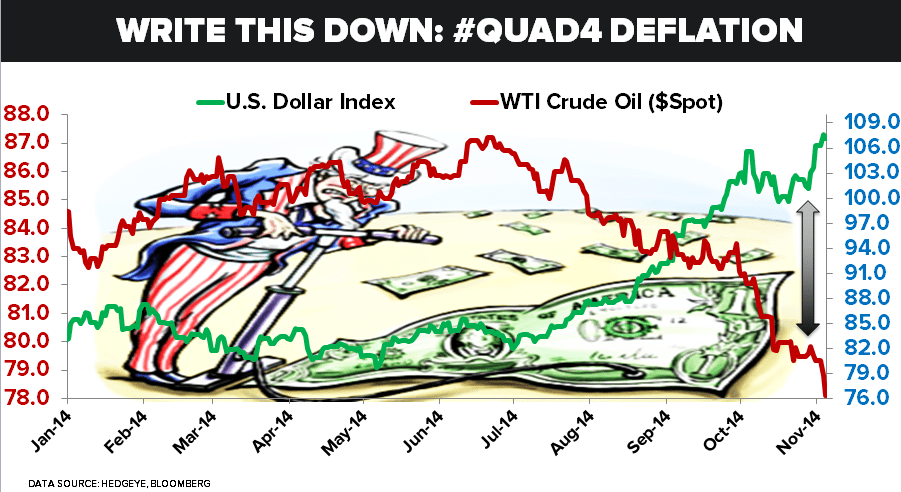

To review, what is #Quad4 Deflation? In our risk management process (rate of change) it’s when the second derivatives in both growth and inflation are slowing, at the same time. These signals are both non-linear, and dynamic.

“There has been no episode of persistent deflation in the United States since the period from 1927-1933; as a result, Americans have practically no living memory of deflation.” (The Death of Money, pg 9)

I was in LA yesterday (San Francisco today) and, to a degree, I think that’s why we’ve been getting so many moments of silence in one-on-one Institutional Investor meetings as of late. It’s really hard for objective risk managers to absorb a scenario they’ve really never had to deal with.

“Objective”? Yes, as in this is what the market told you about #Deflation expectations yesterday:

- US Dollar up +0.3% to +8.8% YTD

- WTI Crude Oil down -2.8% to #crashing -20.5% YTD

- Energy Stocks (XLE) down -1.6% to -2.8% YTD

- Basic Material Stocks (XLB) -0.7% to +3.9% YTD

- Healthcare Stocks (XLV) +0.1% to +21.5%% YTD

In other words, in stark contrast to the Dollar Up, Rates Up #Quad1 signal we gave you to be long of everything big beta US growth in 2013, this Dollar Up (going to cash), Down Rates, #Deflation move is nasty for most things that lose their pricing power.

Healthcare (XLV) and Utilities (XLU) are two of the sectors that don’t get decimated by #deflation as fast as a levered-long-crude-oil-hedgie-dude (or an upstream E&P MLP dude who depends on the “dividend” that is decided by the price of the other dude’s oil inflation expectations).

I know, #dude!

That’s why the objective investor who has been writing down the sector returns for the SP500 in 2014 has noted the following RELATIVE YTD performance:

- Healthcare (XLV) +12.3% YTD

- Utilities (XLU) +11.4% YTD

- Technology (XLK) +4.7% YTD

Vs.

- Basic Materials (XLB) -5.2% YTD

- Consumer Discretionary (XLY) -7.3% YTD

- Energy (XLE) -12.0% YTD

Yep, if all you did was express either our early-cycle slowdown calls for #ConsumerSlowing and #HousingSlowdown from the beginning of the year and/or our #Quad4 deflation call, in your S&P Sector asset allocations, you’ve crushed it.

If all that mattered to the American Consumer was “gas prices” (it actually represents only 6.4% of the median consumer’s budget) all of these rosy “surveys” you’ve been reading would have been right. Instead, in relative and sector performance terms, those narrative fallacies got you killed.

But, but, the ISM number was great yesterday. Yep, just great, another survey!

In other news, Industrials (XLI) closed down on the day on that ISM manufacturing report. I wonder if that’s because the non-survey data (US Retail Sales, Consumer Spending, Durable Goods, Construction Spending, and New Home Sales), all recently SLOWED, in actual rate of change terms!

Moving along…

If only everyone who writes in this business was forced to actually write this stuff down, every single day, consensus might be as concerned about the big beta #bubble in levered-long-and-illiquid US equity inflation expectations as I am.

But what is your catalyst, Keith?

- What I have been writing to you all year is already happening

- What I have seen (on the mid-October Russell and Bond Yield Lows) has not been forgotten

- What is most probable to happen next is more of the same

If everything that was in #crash mode on October 13-14th were to crash, literally, tomorrow… I’d write it down too – and “it” would be something that should not come as a surprise to anyone.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.21-2.37%

SPX 1967-2033

RUT 1086-1181

Italy’s MIB Index 18912-20099

Yen 109.27-113.66

WTI Oil 76.41-80.94

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer