Editor's note: This complimentary research was originally published November 13, 2014 at 07:33 in Financials. For more information on our services click here.

After a two month slide, taxable bonds rebounded posting their first subscription in 8 weeks.

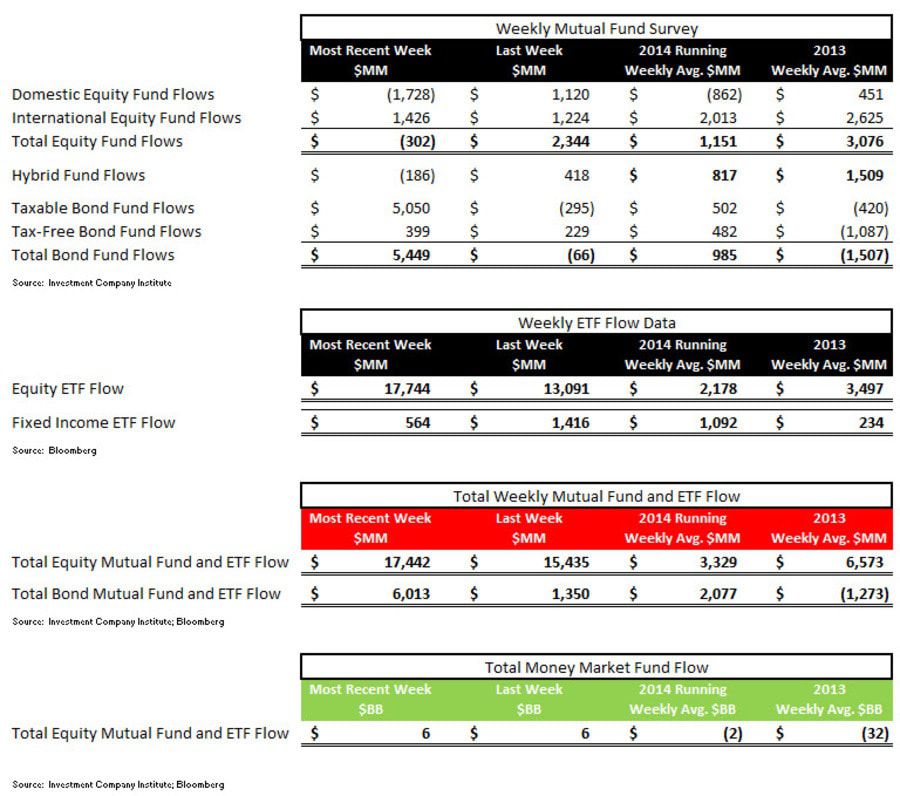

Investment Company Institute Mutual Fund Data and ETF Money Flow:

After an exciting month of October whereby over $36 billion alone spilled out from the taxable bond fund category, the latest ICI survey relayed some stability with a $5.0 billion inflow by investors, the first subscription since the week ending September 10th. A post-mortem of the beneficiaries of the October snap redemption shows that broadly bond ETFs hoovered up the most "money in motion," with several select Total Return Funds including the Metropolitan West Total Return Fund (a unit of TCW), BlackRock's flagship fund, and Jeff Gundlach's DoubleLine substantially improving assets-under-management in the month. Interestingly, but not a surprise to us, the Janus Uncontrained Bond Fund, had a very modest benefit and as a result we remain skeptical of the resulting market cap improvement of that company without the support of new assets-under-management (read our JNS research here).

In other survey data, U.S. equity mutual funds put up another worrisome $1.7 billion redemption making it 25 of the past 28 weeks with outflows. We continue to recommend underweight or short positions to those managers with outsized U.S. equities exposure (read our research here). Passive fund flows via ETFs continue to be substantial with a year-to-date high of $17.7 billion into total equity ETFs last week and another inflow into bond ETFs, the 6th straight week of fixed income subscriptions. The blood letting continued specifically in the Materials Sector SPDR with another 19% of assets-under-management alone coming out of that product over the past 5 days. Conversely there has been strength in Utilities (XLU) and the 20+ Treasury ETF (TLT) products with respective inflows improving AUM by 7% and 8% during the week.

In the most recent 5 day period ending November 5th, total equity mutual funds put up net outflows with $302 million coming out of the category according to the Investment Company Institute. The composition of the outflow was squarely the result of domestic stock fund redemptions as a $1.7 billion loss more than nullified the $1.4 billion which came into international stock funds. The two equity categories have been polar opposites all year with international stock funds having had inflow in 43 of the past 44 weeks, versus domestic trends which have been very soft with inflow in just 15 weeks of the 44 weeks thus far year-to-date. The running year-to-date weekly average for all equity fund flow continues to decline and now settles at a $1.1 billion inflow, now well below the $3.0 billion weekly average inflow from 2013.

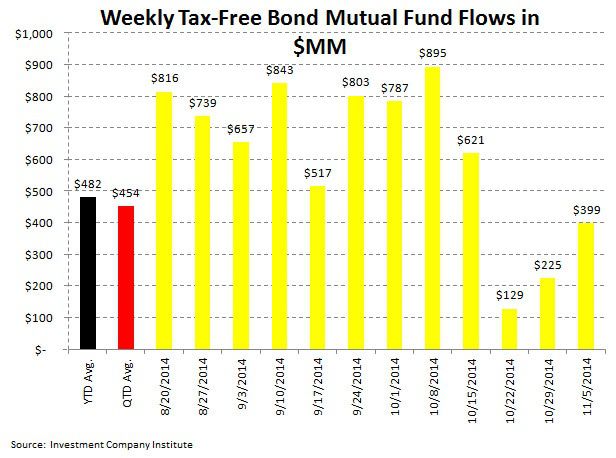

Fixed income mutual funds napped their drawdown schedule of the past 5 weeks putting up inflows in both the taxable bond fund category and also in tax-free munis. Taxable fixed income netted a fresh $5.0 billion in investor money with municipal bond funds putting up a $399 million inflow, making it 42 of 44 weeks with positive subscriptions in tax-free bonds. The 2014 weekly average for fixed income mutual funds now stands at a $985 million weekly inflow, an improvement from 2013's weekly average outflow of $1.5 billion, but still a far cry from the $5.8 billion weekly average inflow from 2012 (our view of the blow off top in bond fund inflow).

ETF results were very strong during the week with substantial inflows in equity funds and decent subscriptions into passive fixed income products. Equity ETFs put up a 2014 year-to-date high subscription with a $17.7 billion inflow which made the $564 million inflow into passive bond products look very modest. The 2014 weekly averages are now a $2.1 billion weekly inflow for equity ETFs and a $1.1 billion weekly inflow for fixed income ETFs.

Mutual fund flow data is collected weekly from the Investment Company Institute (ICI) and represents a survey of 95% of the investment management industry's mutual fund assets. Mutual fund data largely reflects the actions of retail investors. Exchange traded fund (ETF) information is extracted from Bloomberg and is matched to the same weekly reporting schedule as the ICI mutual fund data. According to industry leader Blackrock (BLK), U.S. ETF participation is 60% institutional investors and 40% retail investors.

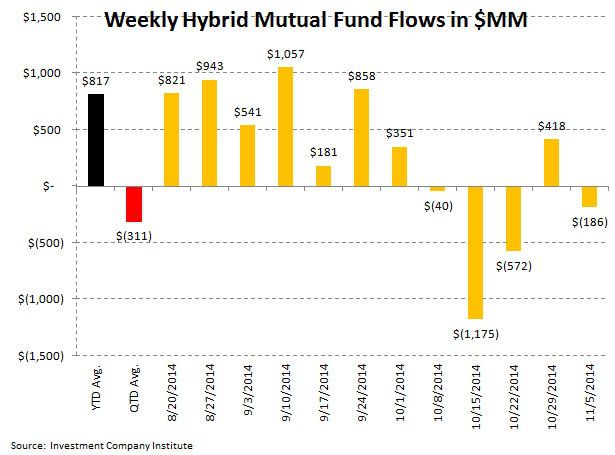

Most Recent 12 Week Flow in Millions by Mutual Fund Product: Chart data is the most recent 12 weeks from the ICI mutual fund survey and includes the running weekly year-to-date average for 2014 and the weekly quarter-to-date average for 4Q 2014:

Most Recent 12 Week Flow Within Equity and Fixed Income Exchange Traded Funds: Chart data is the most recent 12 weeks from Bloomberg's ETF database (matched to the Wednesday to Wednesday reporting format of the ICI) and the running weekly year-to-date average for 2014 and the weekly quarter-to-date average for 4Q 2014. The third table are the results of the weekly flows into and out of the major market and sector SPDRs:

Sector and Asset Class Weekly ETF and Year-to-Date Results: In specific callouts, the blood letting continued in the Materials Sector SPDR with another 19% of assets-under-management alone coming out of that product over the past 5 days. Conversely, the Utilities (XLU) and 20+ Treasury ETF (TLT) had respective inflows of 7% and 8% during the week.

Net Results:

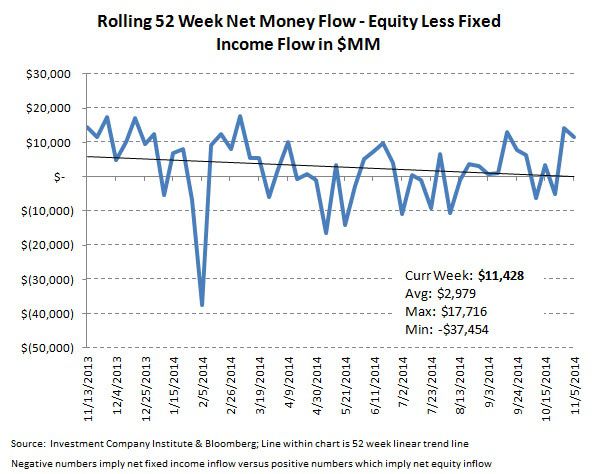

The net of total equity mutual fund and ETF trends against total bond mutual fund and ETF flows totaled a positive $11.4 billion spread for the week ($17.4 billion of total equity inflow versus the $6.0 billion inflow within fixed income; positive numbers imply greater money flow to stocks; negative numbers imply greater money flow to bonds). The 52 week moving average has been $2.9 billion (more positive money flow to equities), with a 52 week high of $17.7 billion (more positive money flow to equities) and a 52 week low of -$37.5 billion (negative numbers imply more positive money flow to bonds for the week).

Exposures: The weekly data herein is important for the public asset managers with trends in mutual funds and ETFs impacting the companies with the following estimated revenue impact:

Jonathan Casteleyn, CFA, CMT

203-562-6500

Joshua Steiner, CFA

203-562-6500