HEDGEYE RETAIL IDEA LIST

This Week's Changes Hedgeye Retail Idea List

- Added Hibbett Sports to Short Bench: We don't have enough ammo to short ahead of earnings this Friday. But we have an extremely negative view on the margin implications as HIBB changes its business model to protect its market share.

- Removed JC Penney from our long bench. It became clear to us that JCP could achieve its sales goals -- but only if the economy is optimal. The problem is that we're six years into a recovery, and the liklihood of going another four is slim, in our opinion. We pick four years as the bogey because that's when JCP faces a significant $2.2bn maturity. We're not making the 'donut' call on JCP. But we think that there's just as great a chance that this stock goes to zero as it does going to $15. Not a good risk/reward by any stretch.

EVENTS TO WATCH

RH Atlanta

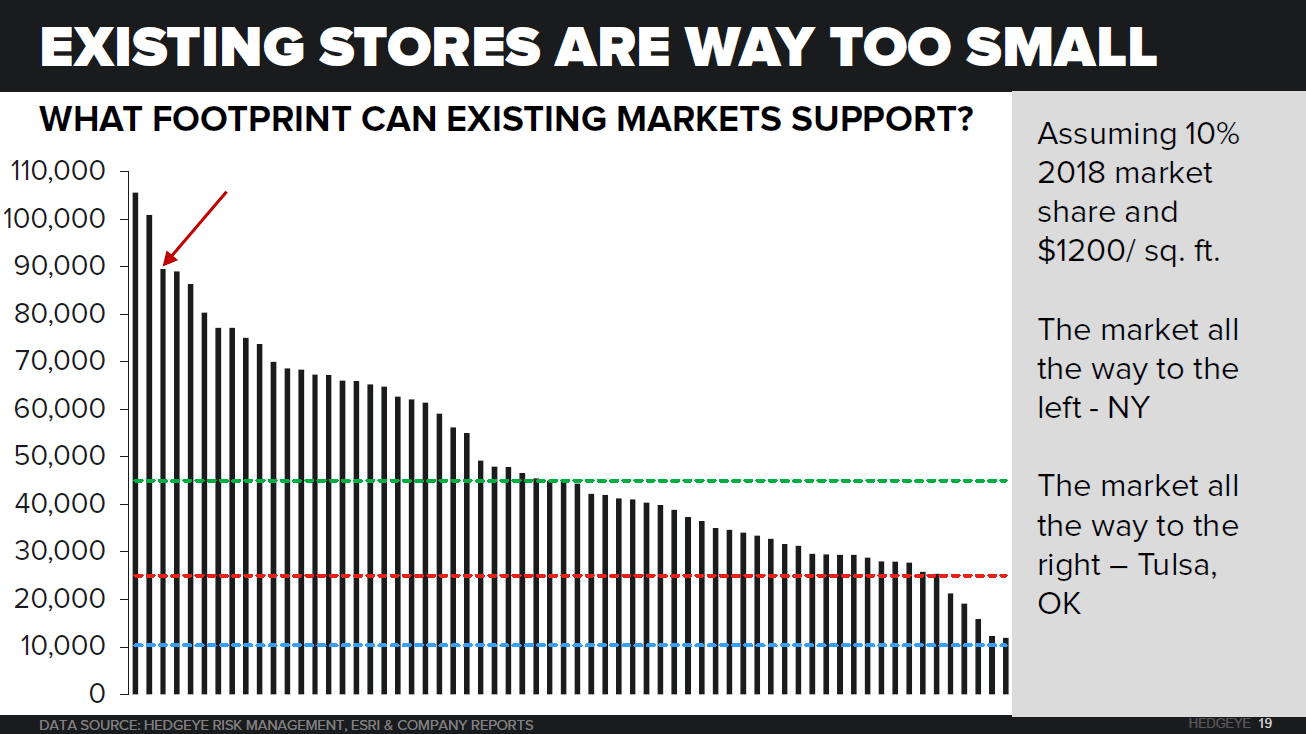

We'll be at the RH Atlanta Design Gallery Grand Opening on Thursday night. This is an important one because the store is 65,000 SqFt -- the first of the '2nd Generation' Design Galleries. Remember that the first wave of Design Galleries averaged at about 20,000 feet. The Street 'gets it' that the economics in these stores are significantly better than in the legacy 9,000 ft stores, but there are massive questions (and doubts) about the economics associated with a mega-store like what RH is building in Atlanta.

A couple of reasons why we think this store size makes sense for RH in Atlanta.

1. As we outlined in our RH Real Estate Deep Dive, you need to look at market size of every single store -- which we define as home furnishings spend for consumers earning over $100k. We did that in every single region RH operates.

2. Our math suggests that there are 22 existing RH locations that could support a store of 60,000 or greater. This assumes 2018 market share of 10%, and sales productivity of $1,200.

3. Of these 22 locations, Atlanta is #3 on the list, behind New York and Houston. Our math suggests RH could have a store size as great as 90,000 feet.

4. The rent economics work. Relative to RH's existing store in Atlanta, we think that occupancy math lines up well with the Denver store, which will open in 2015 (See math below).

RH remains our top idea in Retail.

COMPANY HIGHLIGHTS

AdiBok - ESPN Anchor Blames adidas Shoes for Derrick Rose's Injuries

H&M - October Sales +14% vs Last Year

(http://about.hm.com/content/dam/hm/about/documents/en/cision/2014/11/1428617_en.pdf)

WMT - Walmart workers plan Black Friday protests over wages

(http://www.reuters.com/article/2014/11/14/us-walmart-labor-idUSKCN0IY1RU20141114)

- "A group of Walmart employees pushing for higher wages said on Friday they were planning protests at 1,600 Walmart stores nationwide on Black Friday."

KATE - Ad of the Day: Anna Kendrick Makes Something Out of Nothing in Kate Spade's Holiday Ad

AMZN - Amazon chief Jeff Bezos takes long-term view

- "Last week, Mr Bezos gave a textbook demonstration. He abandoned a long-running and very public spat with French publisher Hachette over ebook pricing. Amazon appeared to make some big concessions. The bookseller gave up its right to sell ebooks at any price it chose – essentially the way it sells the physical product now."

KORS - Michael Kors' Instagram Adds 'Buy'

(http://www.wwd.com/media-news/digital/kors-instagram-adds-buy-8034767?module=hp-topstories)

- "Facebook and Twitter are instrumental in inspiring fans and helping in the shopping process, but finding a way to 'shop' Instagram was a necessity, the company said."

JOEZ - Joe's Jeans Defaults on Term Loan

- "Joe’s Jeans Inc. declined 21.2 percent to close at 75 cents in Nasdaq trading, after the company reported that it had fallen out of compliance with the profit requirements of its Garrison Loan Agency term loan and was seeking waivers and adjustments."