TODAY’S S&P 500 SET-UP – November 17, 2014

As we look at today's setup for the S&P 500, the range is 55 points or 2.20% downside to 1995 and 0.50% upside to 2050.

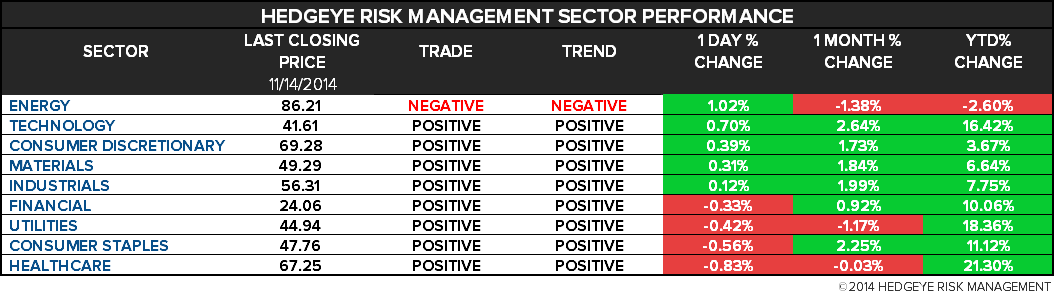

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.80 from 1.81

- VIX closed at 13.31 1 day percent change of -3.48%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Empire Manufacturing, Nov., est. 12.0 (prior 6.17)

- 9:00am: ECB’s Draghi speaks in Brussels

- 9:15am: Capacity, Oct., est. 79.3% (prior 79.3%)

- 9:15am: Industrial Production, Oct., est. 0.2% (prior 1%)

- 10am: Fed’s Evans speaks in Chicago

- 11am: U.S. announces plans for auction of 4W bills

- 11:30am: U.S. to sell $24b 3M bills, $28b 6M bills

GOVERNMENT:

- 1pm: Nuclear Regulatory Commission Chair Allison Macfarlane speaks at NPC on safe operation of nation’s more than 100 nuclear power plants

WHAT TO WATCH:

- Japan Unexpectedly Enters Recession as Abe Weighs Tax

- *Pfizer to Buy Merck KGaA Cancer Drug Rights for $850m

- ** Pfizer Cuts 2014 Reported Diluted EPS Range to $1.40-$1.49

- Actavis Said Near Deal to Buy Allergan for Over $215/Share

- Halliburton Said to Resume Merger Talks With Baker Hughes

- JPMorgan Settles Oil Rights-Owner Suit Alleging Deals

- Zoetis Adds Poison Pill as Ackman Stake Raises Takeover Chance

- Ford Expands Ranger Pickup Recall for Flawed Takata Air Bags

- Facebook Tells Marketers to Stop Trying to Post Ads for Free

- Delta Seeks to Boost Asia Hub With Plan to Triple Seattle Gates

- Carrey’s ‘Dumb & Dumber To’ Debuts as Top Box-Office Hit

- China’s Bad Loans Jump Most Since 2005 in Threat to Economy

- Putin Warns He Won’t Let Rebels Be Beaten by Ukraine Forces

- Citigroup, JPMorgan, others post monthly credit-card data

- 13-F WRAP: Alibaba Attracts Appaloosa, Paulson, Soros, Moore

EARNINGS:

- Agilent Technologies (A) 4:05pm, $0.89

- Jacobs Engineering (JEC) 9:30pm, $0.86

- Keysight Technologies (KEYS) 4pm, $0.77

- Tyson Foods (TSN) 7:30am, $0.77

- Urban Outfitters (URBN) 4pm, $0.41

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Brent Crude Drops on Growth Concerns as Japan Enters Recession

- Gold Trades Below Two-Week High Amid Signs of Physical Buying

- China to Cut Agriculture Tariffs in ‘Game Changer’ for Australia

- Hedge Funds Cut Gold Bets in Fastest Exit This Year: Commodities

- Copper Falls Amid Demand Concern as Japan Sinks Into Recession

- Australia-China Free Trade Deal to Remove Some Resources Tariffs

- Mounting Pressure on OPEC Spurs More Wagers on Oil Rally: Energy

- Osisko to Buy Virginia for $408 Million to Add Gold Royalties

- Steel Rebar Falls as Weak Demand Weighs Against Production Cuts

- China Copper, Zinc, Alumina Output Rise to Record Highs in Oct.

- Wheat Climbs Toward 11-Week High on Australia, U.S. Crop Outlook

- Arabica Trades Near 3-Week High on Brazil Dryness; Sugar Falls

- OIL DAYBOOK: Crude Down; Iran Minister Visits UAE Ahead of OPEC

- Australia Opens China’s Services Market With Free Trade Accord

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

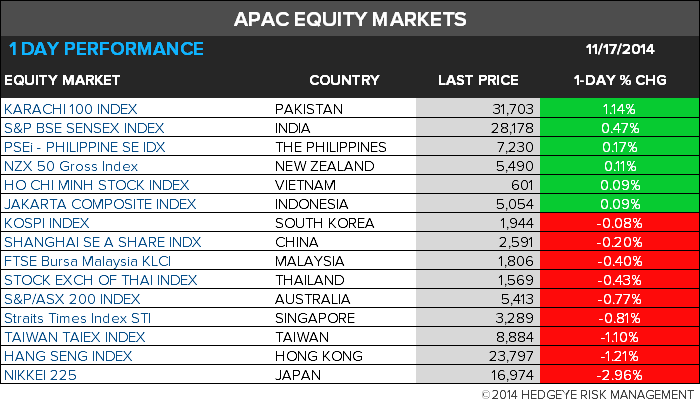

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team