Editor's note: We added HCA to Investing Ideas last Friday 11/7. What follows below is our reasoning from our Healthcare Sector Head Tom Tobin.

HCA $90 +

We flagged the divergence between High Yield and HCA at the end of September as a reason to take profits, and did just that a week later after being up 72%.

Since then, the stock has corrected approximately -12% on the back of a few sell side downgrades despite strong Q3 earnings.

Key data points that we follow continue to show a positive fundamental environment for hospitals and HCA in particular. We view recent weakness as a buying opportunity, as our model points to continued EBITDA upside versus consensus through 2015 and a stock that can trade north of $90.

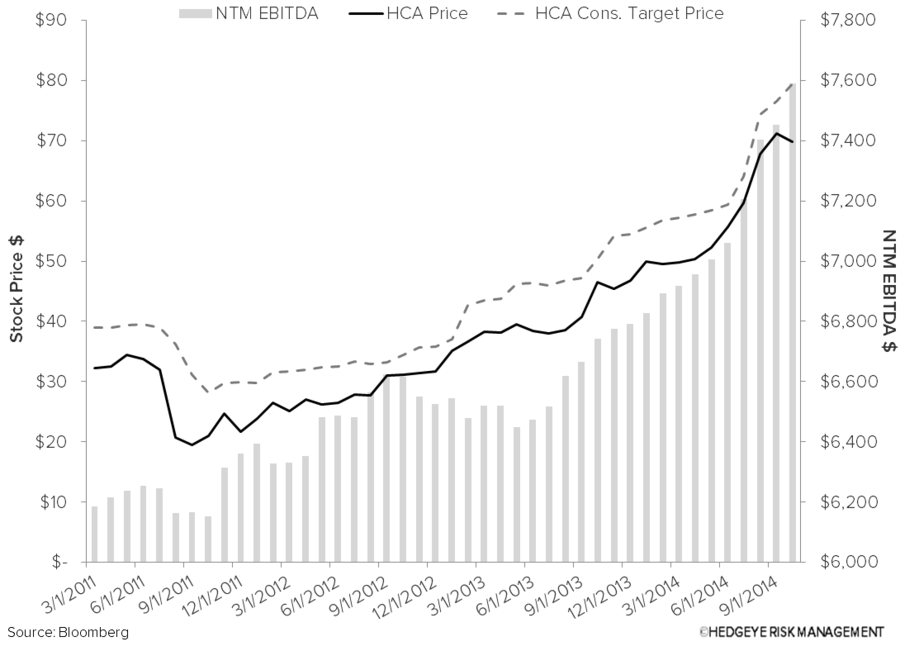

Price and Estimates Trending Higher

One of the problems we identified with HCA heading into 3Q14 earnings was the strong bias to the long side on both the buyside and sellside. With a few downgrades, incremental fear from SCOTUS, and a -12% move in the stock, we are far more excited by the name on the long side. If operating fundamentals excluding ACA continue their modest recovery, consensus EBITDA in 2015 and 2016 look way to low.

HCA Admissions Growth ex-Exchange Strong

Recent concerns among the Hospital names and HCA in particular have centered on the Supreme Court (SCOTUS) review of the legality of subsidy distribution through Federal Exchanges. We’d make 2 points:

1) Handicapping the SCOTUS outcome is close to impossible and

2) Under an adverse SCOTUS ruling scenario, the headwind would be modest