Below are Hedgeye analysts’ latest updates on our six current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

*We also feature two pieces of content from our research team at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

IDEAS UPDATES

TLT | EDV | XLP | MUB

More #Quad4 Confirmation

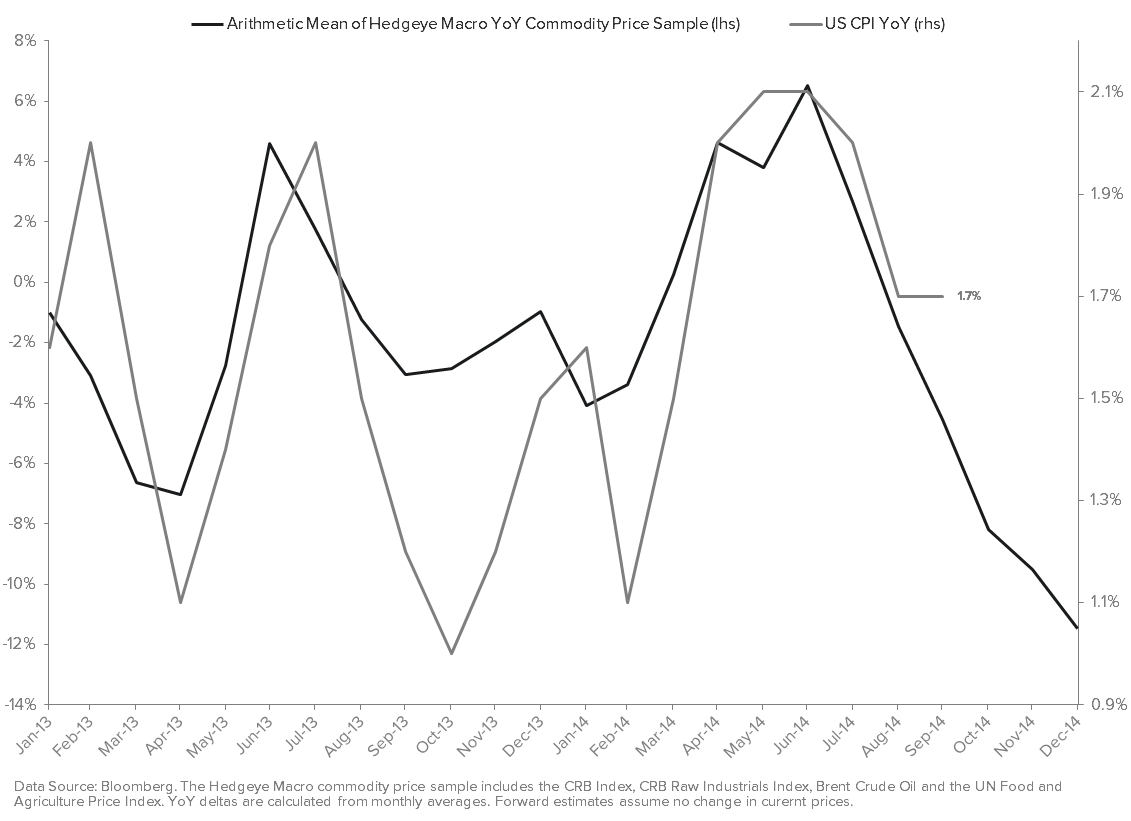

- #Deflation Risk, Revisited: With respect to our CPI model (CLICK HERE to review that methodology), we continue to anticipate disinflation in headline CPI readings over the intermediate term. This would be the case even if commodity prices stopped going down today and remained flat, due to the comparative base effects of #InflationAccelerating in 1H14. Of course, additional commodity price deflation – which our TACRM model continues to imply – would only perpetuate downward concavity in reported inflation; sub-1% YoY CPI readings are very probable over the intermediate term. Since the start of 2008, the CRB Index has declined by a cumulative -43% on a 1-week forward basis when TACRM is generating a “DECREASE Exposure” signal for Commodities as a primary asset class like it is currently.

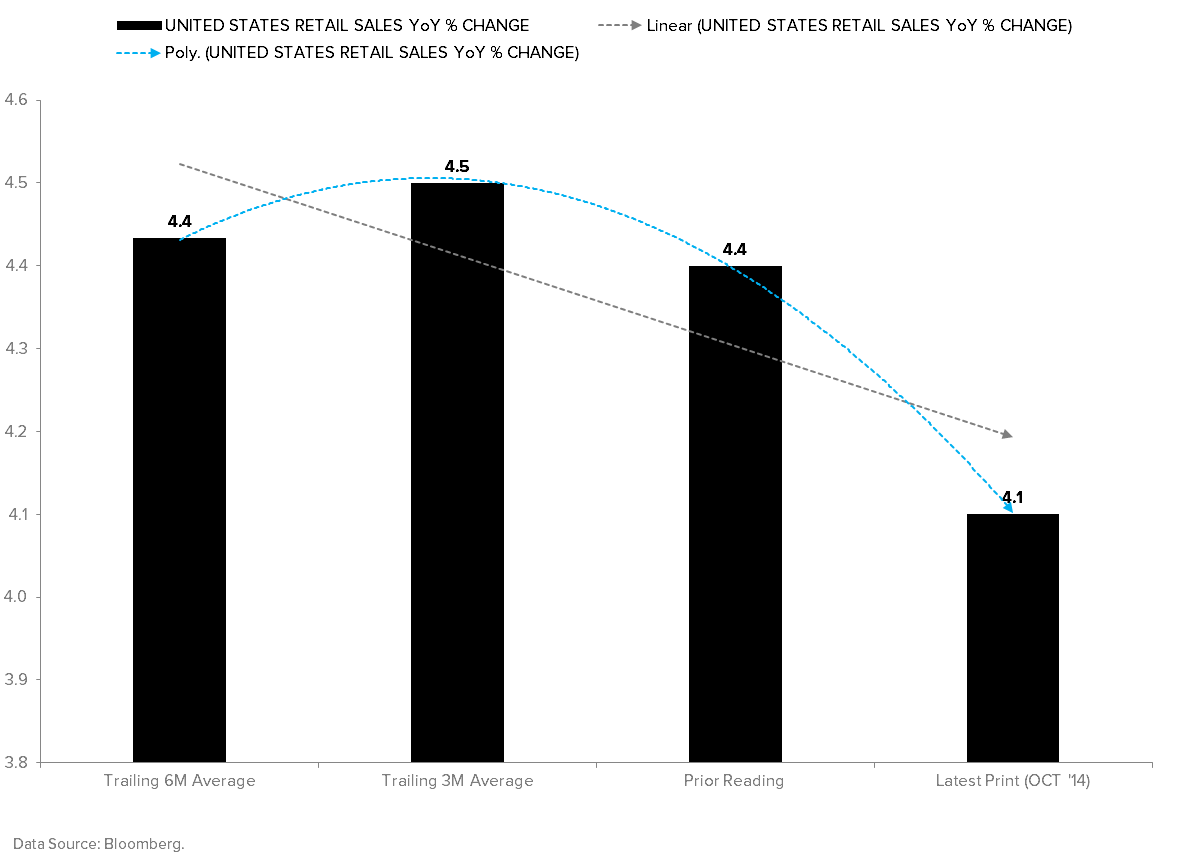

- #ConsumerSlowing, Confirmed: Speaking of developing downward concavity, how about domestic consumption growth? Lost amid the perma-bull storytelling about lower gas prices is the fact that Retail Sales growth continues to slow on a trending basis, decelerating from +4.4% YoY in SEP to +4.1% YoY in OCT! Retail Sales accounts for roughly 1/3rd of PCE, which is ~70% of GDP, so as U.S. consumption growth goes, U.S. economic growth goes – in this case, lower!

All told, with both growth and inflation slowing, we reiterate our #Quad4 asset allocation of long TLT, MUB, EDV and XLP. We see downside to 1.7% on the 10Y Treasury bond yield over the intermediate term.

HCA

We sent out a report explaining our position on Friday. Click here to read.

RH

There’s only one thing that matters right now with Restoration Hardware – and that is next week’s Grand Opening of the new Restoration Hardware Design Gallery in Atlanta.

The store, which is in the Buckhead section of Atlanta, was constructed in space formerly occupied by ESPN Zone. It is about 3x the size of existing design galleries, and 7x larger than legacy stores. While one store will not make or break this company, the anecdotes about productivity that come out in the ensuing weeks will be a major focal point for Wall Street.

The company reports earnings in the second week of December, and will have quantitative insight as to how the store is performing. They set expectations for $650/square foot once the store is up and running, but we think it will come in well ahead of that.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

mcdonald's: weak

We continue to stay on the sidelines here... with a bearish bias.

oil: supply, supply, supply

After a heavy week of data, both the fundamental picture and behavioral market activity suggest continued downside pressure.