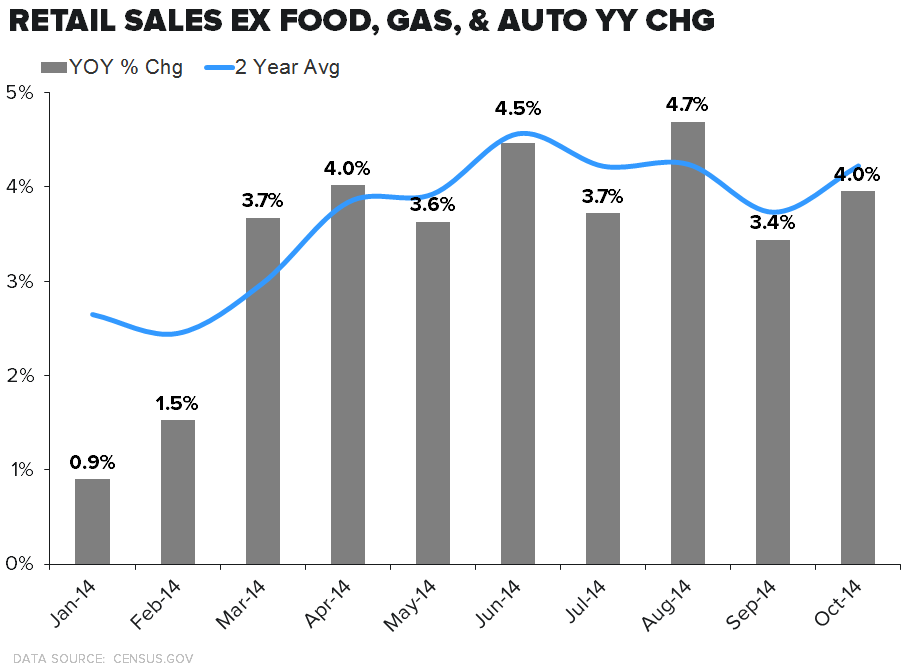

ECONOMIC DATA

Takeaway: A sequential tick up on both the 1 and 2 yr trend lines, though it wasn't reflected in the commentary we've heard from retailers over the past few days. Maybe the answer is as simple as people are buying less of what Department Stores are selling. If that answer works for M and KSS then it's good enough for us.

COMPANY HIGHLIGHTS

JWN - 3Q14 Earnings

Takeaway: The things that we like about JWN, in a space where we have an overwhelmingly negative view, all looked solid. 3.9% Revenue growth, 5% square footage growth, 22% DTC growth on the full-price banner, and 34% growth in Hautelook/Rack.com. After the week of earnings we've seen across the department store space the top line was all that mattered (+9% reported, ~+8% if you exclude the estimated Trunk Club benefit). But, the earnings algorithm was weak, 9% revenue growth translated into a 5% growth in earnings (ex. Trunk Club dilution EPS growth = 11%). The SIGMA trajectory is punk with inventories growing 15 percentage points ahead of sales and margins declining. That almost always equates to a negative margin event in the short term. We added JWN to the long bench on 10/16, but still aren't comfortable with a name operating in a space where we think 93mm square feet needs to disappear over the next 5 years.

TGT - Target Follows WMT E-comm Acquisition Playbook

(http://www.startribune.com/lifestyle/282538741.html)

- "Powered Analytics' Fabric product uses mobile technology, location data and machine learning to connect a retailer's app to the in-store shopping experience."

Takeaway: TGT taking a page out of the WalmartLabs playbook. To keep score - WMT has acquired 15 small tech startups since 2010. Everything from a streaming video service to a recipe and meal planning service. TGT's acquisition strategy has been more company focused to date, i.e. chefs.com and dermstore.com. Maybe none of WMT's deals are homeruns but it has allowed the company to build its digital acumen through the acquisition of people and technology. TGT is way behind on this front and we'd point out has one of the worst dot.com track records in all of retail over the past 8 years.

NKE - Nike warns NFLers Not To Mess With Kicks

Takeaway: We don't blame Nike for reinforcing its endorsement policy and protecting its investment. The company is shelling out $220mm per year for the NFL deal on top of what it is paying its endorsees to wear it's gloves/cleats, and pay to wear fees. Players are billboards and that strategy doesn't work if you can't see the swoosh. Maybe the answer is neon colorways à la the London Olympics or the 2014 World Cup - though we doubt the NFL would let that fly.

OTHER NEWS

KATE - Kate Spade Opens 1st West Coast Location

(http://www.retail-insider.com/retail-insider/2014/11/kate-spade)

- "Kate Spade has opened its first West Coast (Canada) store at Park Royal Shopping Centre in West Vancouver. The 2,000 square foot location is in the mall's southern component, called Park Royal South, next to the mall's new Michael Kors store."

WMT - Wal-Mart Told Store Managers to Match Online Prices With Amazon

- "Greg Foran said the directive was meant to formalize a practice already in place in many stores. 'About half of the stores were doing it anyway,'"

GPS - Old Navy Blasted for Higher Cost of Its Women’s Plus-Size Jeans

- "The petition charges Old Navy with sexism, noting that a pair of women’s plus-size jeans can cost about $15 more than regular jeans, while a pair of men’s jeans costs the same no matter the size."

LULU - Lululemon pushing menswear, expansion

(http://www.fierceretail.com/story/lululemon-pushing-menswear-expansion/2014-11-13)

- "In an effort to boost its menswear sales, Lululemon has begun opening more dual-sex flagship stores. And on Black Friday, the yoga apparel company will open its first men's only store in Manhattan."

BABA - Alibaba's boutique shop 11 Main opens doors on mobile

(http://www.usatoday.com/story/tech/personal/2014/11/12/alibaba-11-main-mobile-launch/18909609/)

- "The shopping site 11 Main, which opened on the Web in June, can be browsed on new smartphone apps especially designed for Apple and Android devices. An iPad app will launch this year."

AMZN - Hachette Looks Like the Winner as Its War With Amazon Ends

- "Hachette Chief Executive Michael Pietsch announced that the book publisher has reached a new multiyear agreement with Amazon.com, ending months of contentious contract negotiations. The deal, which will cover print and e-book distribution, will begin next year."