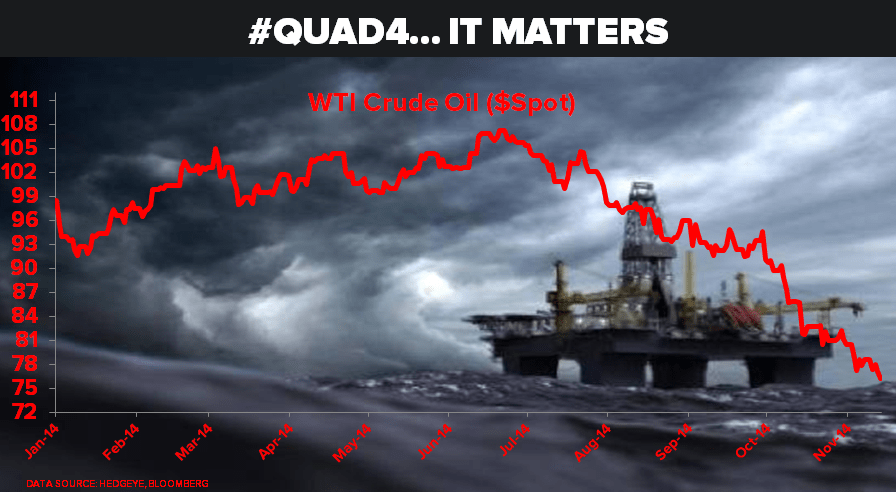

Our macro team’s #Quad 4 deflation call continues to manifest itself in both Oil prices and Energy related countries, stocks, and bonds.

In the end, this will be one of the big things that will have mattered.

Brent is seeing follow through selling after having a -2.6% down day yesterday (down a whopping -29% year-to-date) while WTIC down -0.4% to $76.85 is looking at lower-lows.

#Quad4. It matters.