TODAY’S S&P 500 SET-UP – November 13, 2014

As we look at today's setup for the S&P 500, the range is 59 points or 2.47% downside to 1988 and 0.43% upside to 2047.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.83 from 1.83

- VIX closed at 13.02 1 day percent change of 0.77%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Initial Jobless Claims, Nov. 8, est. 280k (pr 278k)

- Continuing Claims, Nov. 1, est. 2.346m (prior 2.348m)

- 8:45am: Bloomberg U.S. Economic Survey, Nov.

- 9:45am: Bloomberg Consumer Comfort, Nov. 9 (prior 38.1)

- 10am: JOLTS Job Openings, Sept., est. 4.8m (prior 4.835m)

- 10am: Freddie Mac mortgage rates

- 11am: DOE Energy Inventories

- 11am: U.S. to announce auctions of 3M/6M bills, 10Y TIPS

- 1pm: U.S. to sell $16b 30Y bonds

- 12:30pm: Fed’s Plosser speaks in Philadelphia

- 12:45pm: Fed’s Yellen speaks in Washington

- 2pm: Monthly Budget Stmt, Oct., est. $117b (pr -$90.584b)

- 3:30pm: Fed’s Kocherlakota speaks in Stanford, Calif.

GOVERNMENT:

- President Obama in Myanmar, attending East Asia Summit meeting, holding meetings with Vietnamese Prime Minister Nguyen Tan Dung, President Thein Sein of Myanmar

- Senate Republicans, Democrats; House Republicans hold leadership elections

- House votes on bill to approve Keystone XL pipeline

- 10am: House Armed Services Cmte hears from Defense Sec. Chuck Hagel, Joint Chiefs Chairman Martin Dempsey on administration’s strategy on Islamic State

- 10am: House Financial Services Cmte hearing on terrorist financing and Islamic State

- 10am: House Foreign Affairs Cmte hearing on combating Ebola in West Africa

WHAT TO WATCH:

- Takata Subpoenaed by Federal Grand Jury as Chairman Apologizes

- Barclays Pressed by New York’s Bank Regulator in Currency Probe

- Hasbro Said in Talks to Buy ‘Shrek’ Studio DreamWorks Animation

- Five Ways the U.S. Airwaves Auction May Change Mobile Service

- Cisco Sales Forecast Misses Estimates as Carriers Cut Spending

- Verizon Said to Plan to Cut About 1,000 Jobs Through Buyouts

- China Industrial Output, Investment Growth Weakens Amid Eco. Slowdown

- Dow Says Corning Is Seeking to Exit 71-Yr-Old Silicone Venture

- J.C. Penney’s Sales Unexpectedly Drop Amid Warmer Fall Weather

- SABMiller Says Conditions to Remain Challenging as Growth Misses

- Gorman Says Morgan Stanley Pays ‘Competitively’ After Turnaround

- Salesforce to Buy San Francisco Office Tower for $640 Million

- Microsoft Said to Have Agreed to Buy Israeli Aorato, WSJ Reports

- Motorola Mobility Flat-Panel Cartel Case Tests Antitrust Reach

- ING to Cut Voya Stake to 19% in $1.38 Billion Stock Offering

AM EARNS:

- CDK Global (CDK) Bef-Mkt, No est.

- CGI (GIB/A CN) 6:30am, C$0.73 - Preview

- Finning Intl (FTT CN) 9am, C$0.55

- Helmerich & Payne (HP) 6am, $1.67

- Kohl’s (KSS) 7am, $0.74 - Preview

- Manulife Financial (MFC CN) 5:55am, C$0.40 - Preview

- Maximus (MMS) 6:30am, $0.52

- Sally Beauty (SBH) 7:30am, $0.40

- TransDigm (TDG) 7:15am, $2.02

- Tyco Intl (TYC) 6am, $0.56 - Preview

- Viacom (VIAB) 6:55am, $1.68 - Preview

- Wal-Mart Stores (WMT) 7am, $1.12 - Preview

PM EARNS:

- Applied Materials (AMAT) 4:02pm, $0.27 - Preview

- Element Finl (EFN CN) 5:30pm, C$0.15

- Intrexon (XON) 4:30pm, ($0.21)

- Nordstrom (JWN) 4:05pm, $0.71 - Preview

- Sina (SINA) 5pm, $0.19

- Western Forest (WEF CN) 5:30pm, C$0.03

- Youku Tudou (YOKU) 6pm, ($0.45)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Demand Falls to 5-Year Low on Less Coin, Jewelry Buying

- Brent Oil Extends Drop to 4-Year Low as OPEC Seen Resisting Cuts

- Why Fewer U.S. Cows Means Higher Leather Bag Costs: Commodities

- Copper Advances Amid Speculation China Will Move to Aid Growth

- Gold Falls a Second Day as Oil Declines While Equities Advance

- Saudis Reject Talk of OPEC Market Share War as Crude Tumbles

- Cash-Burning Bets on Oil Rebound Keep Surging in U.S. ETF Market

- Sugar Harvest Seen Rising in India to Help Extend Global Surplus

- Tin Prices Seen Climbing 14% in 1Q as Indonesia Tightens Sales

- Iraq Kurds Form Oil Company Separate From Central Government

- Iron Ore Mine Closures May Lead to $70 Floor Price, ANZ Says

- Corn Rises for Fourth Day as Arctic Blast Heads for U.S. Plains

- Palm Oil Drops a Second Day as Brent Slump Cuts Biofuel Demand

- Gold Imports by India Double as Price Drop Fuels Festival Demand

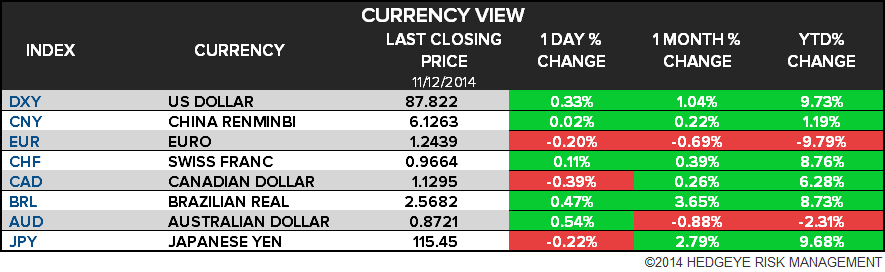

CURRENCIES

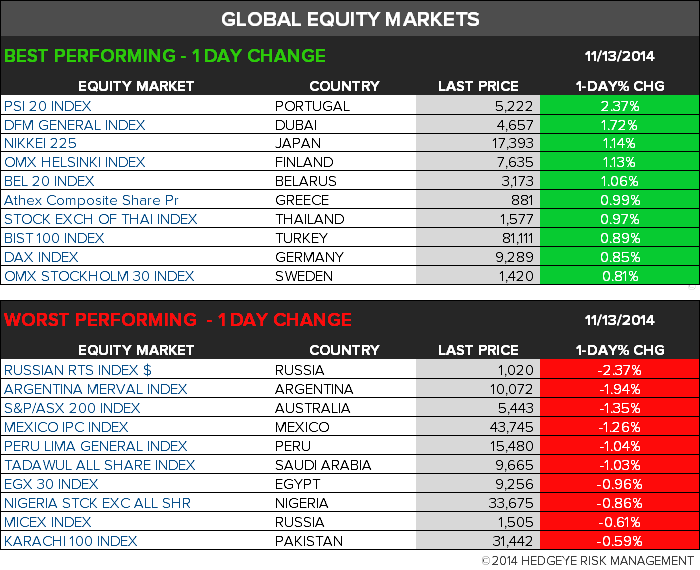

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team