Investor DAY HIGHLIGHTS

- COURT THE PASSIVE VISITOR: TWTR gets a lot more passive traffic than its MAU metrics suggest. Visitors get routed to twitter when clicking a twitter-related link while on another site, but most of these visitors do not interact with twitter past that point. TWTR is looking to court the passive user by presenting them with a timeline of tweets when that occurs, hoping it will boost their registrations & MAU metrics.

- EXPAND PRODUCT PORTFOLIO: There was a greater emphasis on enhancing private chat options. TWTR also wants to introduce new products to expand its product portfolio, suggesting a greater emphasis on Vine, but no other detail regarding other potential ideas.

- ENHANCE DEVELOPER FUNCTIONALITY: TWTR wants to make it easier for developers to interact with the twitter platform. The rationales is that if developers can build and monetize their third-party applications, TWTR could reach a broader audience.

TAKEAWAYS

- LONG ON PROMISE, SHORT ON DETAIL: The only real detail came on its efforts to court the passive user. Outside of that, nothing material. Remember that FB also experimented with private chat options (Facebook Messenger), then wound up acquiring WhatsApp. In terms of additional products, we suspect that means acquisitions (TWTR just raised $1.7B in new capital). Expanding third-party application efforts could have the perverse effect of routing TWTR users away from the platform (same as Tweetdeck did before TWTR acquired it). In short, we wouldn’t get too excited.

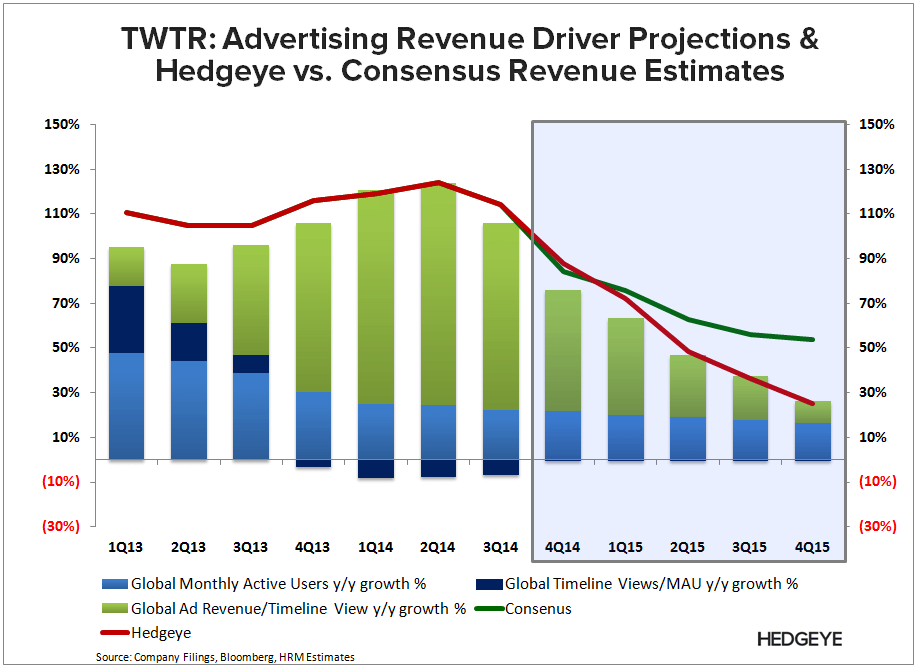

- THE BIGGER ISSUES REMAIN: TWTR’s strength over the LTM has been driven primarily by monetization, which we estimate has been driven by surging ad load more than anything else. We suspect there is a perverse relationship between ad engagements (monetization) and user growth, which suggests that its surging ad load strategy is pressuring user retention. This relationship creates a tug of war between user and revenue growth; if TWTR experiences any weakness on either front, the street will hammer the stock for it.

For more detail on our short thesis, see link to our most recent note below. Let us know if you have any questions, or would like to discuss in more detail.

TWTR: The Story Has Changed

10/28/14 07:13 AM EDT

http://app.hedgeye.com/feed_items/38904

Hesham Shaaban, CFA

@HedgeyeInternet