EVENTS TO WATCH

COMPANY HIGHLIGHTS

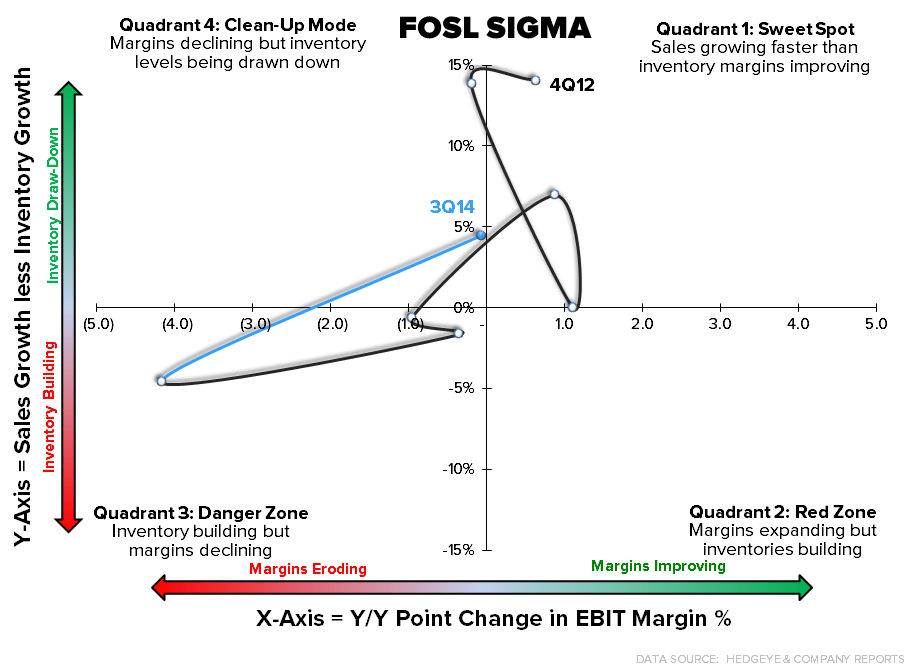

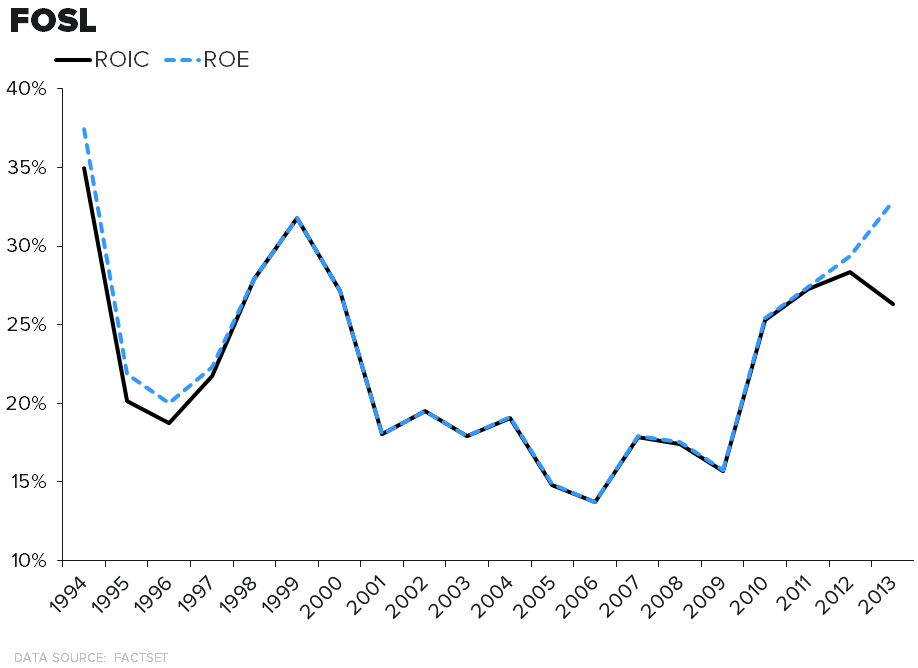

FOSL - 3Q14 Earnings

Takeaway - Fossil hit the earnings trifecta this quarter. Not only did it beat the quarter by 8%, but did so by putting up a clean algorithm of +10% sales, +15% net income, and +25% net income. Its SIGMA trajectory swung towards the upper right hand quadrant, which is bullish for gross margins in the upcoming quarter. One thing we particularly liked was how we're starting to see a meaningful diversion between ROE and ROIC for this company. Too many companies that tout improving ROIC trends leave out the fact that they're letting cash build on their balance sheets. FOSL is doing the inverse. When we see ROE trending above an upward-sloping ROIC curve, we definitely take notice. Oh, and by the way, the Michael Kors agreement -- which accounts for 22% of FOSL sales -- was renegotiated until 2024.

AMZN, EBAY - Sequential slowing for both AMZN and EBAY in ChannelAdvisor Comp Sales

Takeaway: The noticeable spread between the two companies in 2014 held in October. Sales growth slowed for both companies slowed on a 1 and 2 year trend. Ebay's +4.4% is the worst month since early 2011.

AMZN, EBAY, DKS - Golf Comps

Takeaway: Amazon golf comps put up yet another strong month. The delta between Amazon and eBay can partially be explained by the fact that eBay implemented a defect rate as part of its seller profile earlier this year, thus pressuring used product sellers to be more selective in their inventory. At the same time Amazon has added features to expand the used category. Either way, strong sales in this channel -- which is the bottom of the food chain for golf sales -- does not bode well for the category in general. The malaise that became apparent earlier this year (plaguing DKS and others) is still alive and well.

WMT - Walmart Memo Orders Stores to Improve Grocery Performance

Takeaway: The writer here clearly had an agenda from the start. Taking a confidential memo about the need for improvement in the grocery department and dovetailing that with a singular store visit is just flat out irresponsible. For starters, these types of memos get circulated all the time. We're sure if you found a disgruntled Whole Foods employee you could get your hands on something similar. Asking your employees to execute on the 'Would I Buy It?' grocery test isn't egregious. The troubling thing for WMT is the overall discontent from its employee - that's nothing new, we know that, but to have store managers tactically leak information to the press is never a good recipe. This is an employee-relations problem, not a grocery problem.

OTHER NEWS

WMT - Wal-Mart Stretches Black Friday Deals to Reach Shoppers

- "The 'New Black Friday' will include five days of sales on Walmart.com and in stores, starting at 12:01 a.m. online on Thanksgiving and running through Cyber Monday, the Bentonville, Arkansas-based company said in a statement today."

JWN - Nordstrom Rolling Out Shoes of Prey In-Store Shops

- "Nordstrom is rolling out in-store shops for Shoes of Prey, an Australia-based online firm that enables women to design their own shoes."

Cambodia to Increase Minimum Wage

- "The minimum wage in Cambodia’s garment sector will be raised to $128 beginning in 2015, a 28 percent increase over the current $100 monthly wage."

REI names its first-ever chief creative officer

(http://www.chainstoreage.com/article/rei-names-its-first-ever-chief-creative-officer)

- "Outdoor outfitter REI has added a chief creative officer slot, and hired Ben Steele to fill the position, effective Jan. 1. Steele most recently served as executive creative director at global brand firm Hornall Anderson in Seattle."

BBY - Best Buy to open 5 p.m. on Thanksgiving, one hour earlier than last year

(http://www.chainstoreage.com/article/best-buy-open-5-pm-thanksgiving-one-hour-earlier-last-year)