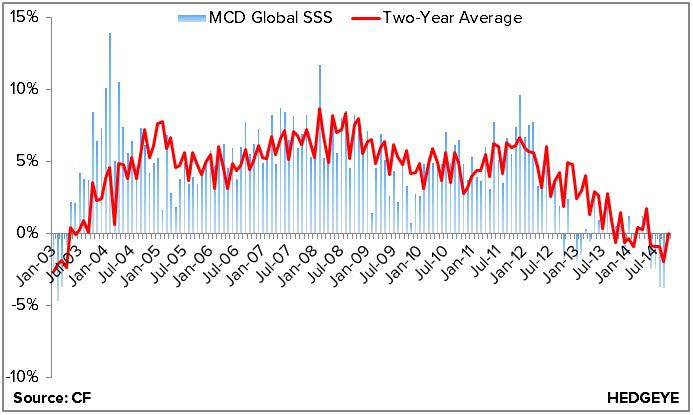

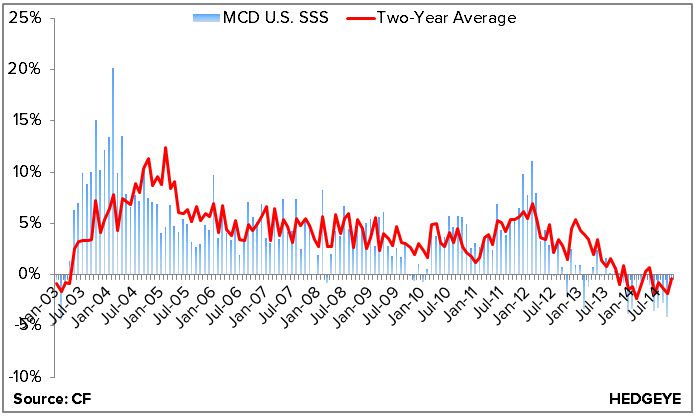

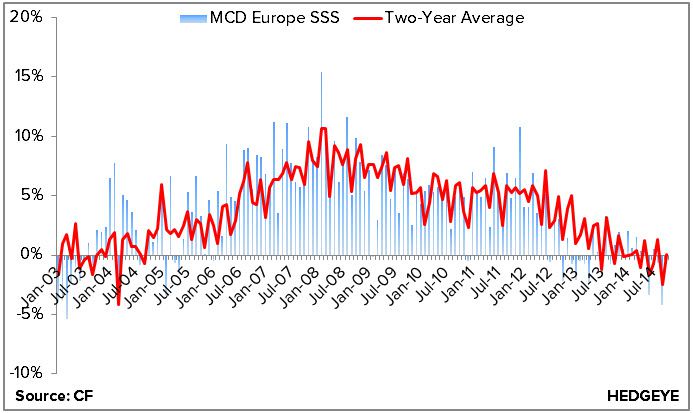

MCD reported same-store sales for the month of October this morning. Despite weak numbers across the board, they were admittedly better than feared:

- MCD Global SSS -0.5% vs -2.2% estimate

- MCD US SSS -1.0% vs -1.9% estimate

- MCD Europe SSS -0.7% vs -2% estimate

- MCD APMEA SSS -4.2% vs -6.1% estimate

Our take on October sales numbers were (1) estimates for the month were quite low after a disastrous September and (2) even after a small upside surprise this month there is no light at the end of the tunnel for a true recovery.

Global, US, Europe and APMEA comps all accelerated meaningfully in October. Comps in all four regions, however, remain negative on a two-year basis, suggesting there is still much work to be done; particularly when considering the strength we’ve seen in the industry over the past few months. MCD continues to lose market share to BKW, JACK, SONC, WEN and others.

Rhetoric showed no sign of direction, as CEO Don Thompson merely emphasized the need for change without much of a plan to get there. Some initiatives to stem the company’s multi-year decline are underway, particularly in the US where the team is changing its marketing approach, simplifying its menu and creating a new organizational structure. We expect these efforts, however, to fall short.

Despite positive results, on the margin, it is important to recognize that McDonald’s continues to face significant challenges across the globe. The US struggled during the month due to “strong competitive activity;” Europe was hampered by “very weak” results in Russia; and APMEA continued to suffer from the ongoing impact of the supplier issue.

As we’ve previously mentioned, it will be a long road to recovery for MCD and we're not convinced it is even underway. It has yet to be proven that management’s initiatives will succeed and, at 17.5x NTM P/E, is difficult for us to support this stock. We continue to stay on the sidelines here, with a bearish bias.

Feel free to call, or email, with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst