European Financial CDS - Swaps mostly tightened in Europe last week though were little changed on balance. In fact, on both a w/w and m/m basis EU bank swaps show little change at the moment. The stocks have been a bit more volatile as the average (and median) stock price change was down 3% for the week.

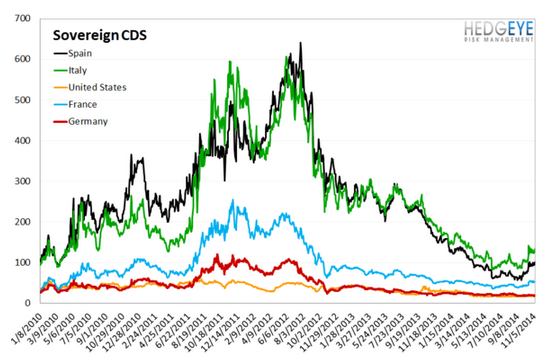

Sovereign CDS – Sovereign swaps were mixed on the week with Portuguese swaps tightening 40 bps to 169 bps while Spanish swaps widened by 7 bps to 101 bps.

Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 2 bps to 11 bps.

Matthew Hedrick

Associate

Ben Ryan

Analyst