Closing Best Idea Short

We added Chuy's Holdings (CHUY) to our Best Ideas list as a short on 10/28/14 at $31.31 per share. Since this time, 2015 EPS estimates have been revised down from $0.97 to $0.80 and the stock has acted accordingly (down ~30). Chuy's may still have issues hitting these revised estimates, but we believe downside from here is limited over the intermediate-term. With this update, we are removing short CHUY from our Best Ideas list.

Recent Notes

11/03/14 Monday Mashup: CHUY, SBUX and More

11/04/14 BLMN: Notable Progress, Still Bullish

11/05/14 CHUY: Look Out Below

11/05/14 BKW: Quick Recap

11/07/14 Strong Restaurant Sales, Traffic, Employment Data

Events This Week

Monday, November 10th

- MCD October Sales and Revenue Release

Thursday, November 13th

- PLKI earnings call 9:00am EST

- COSI earnings call 5:00pm EST

- FRSH earnings call 5:00pm EST

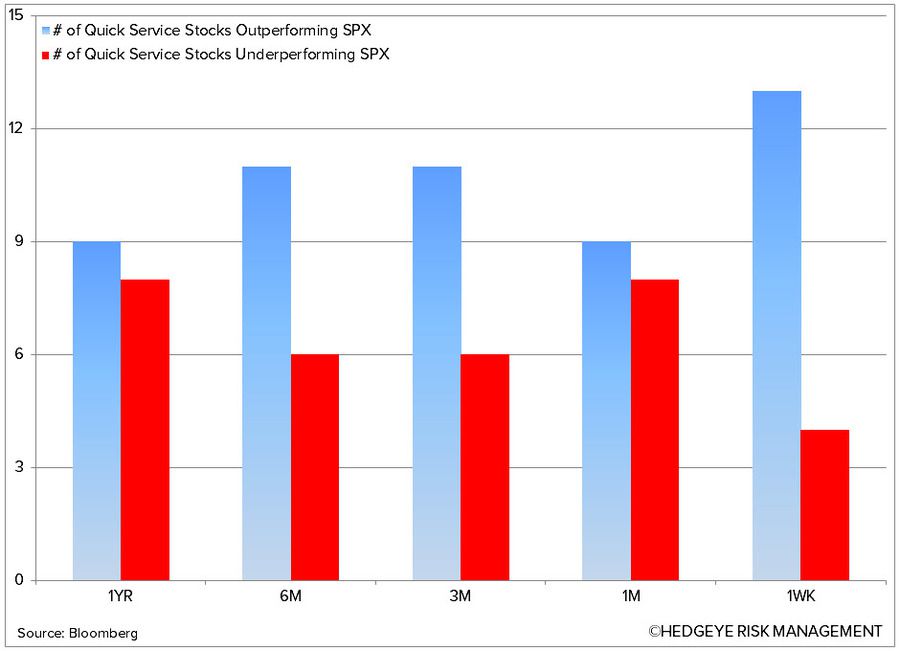

Chart of the Day

Recent News Flow

Monday, November 3rd

- SONC downgraded to neutral at Longbow Research.

- BWLD announced its selection of TBWA/Chiat/Day as its advertising agency of record.

- DFRG announced plans to open a fourth Del Frisco's Grille in North Texas in the summer 2015 and to relocate Del Frisco's Double Eagle Steak House from North Dallas to McKinney & Olive in uptown Dallas in 2016.

- JMBA entered into a new distribution agreement with Gordon Food Service in order to continue service, productivity and cost improvement.

Tuesday, November 4th

- JMBA announced an accelerating refranchising initiative in CA that will involve close to 114 Jamba Juice store locations, primarily in the San Francisco, Sacramento and San Diego markets.

- JMBA also announced a $25 million share repurchase program.

Wednesday, November 5th

- THI announced the Board of Directors declared a $0.32 dividend payable to shareholder of record as of November 20, 2014.

- SONC announced the opening of its brand new Culinary Innovation Center, where its culinary team will test ideas, equipment, recipes and products. The facility is an important part of Sonic's overall growth strategy, which calls for the development of 1,000 new drive-ins in 10 years.

- DPZ downgraded to hold at Miller Tabak with a $90 PT.

- DFRG announced the opening of its newest Del Frisco's Grille in Tampa, Florida. It is the 15th Grille and 45th restaurant overall for Del Frisco's Group.

- DRI announced it has retained Korn Ferry, a leading global executive search team, to aid it in its recruitment of the company's next CEO. Both internal and external candidates will be considered.

- KKD announced a development agreement with Orion Group, for 20 new stores in Bangladesh over the next five years.

Sector Performance

The XLY (-0.1%) underperformed the SPX (+0.7%) last week. However, both casual dining and quick service stocks, in aggregate, outperformed the SPX.

XLY Quantitative Setup

From a quantitative setup, the sector remains bearish on an intermediate-term TREND duration.

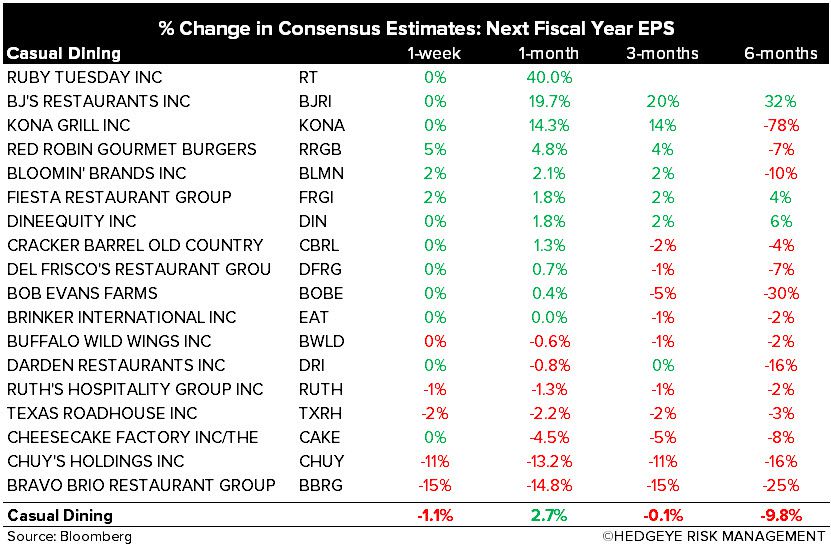

Casual Dining Restaurants

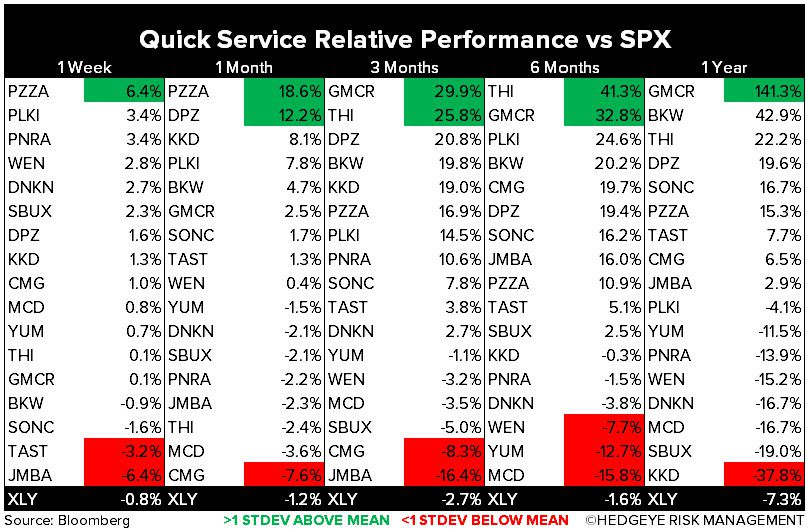

Quick Service Restaurants

Howard Penney

Managing Director

Fred Masotta

Analyst