Current Ideas:

This Week's Thoughts:

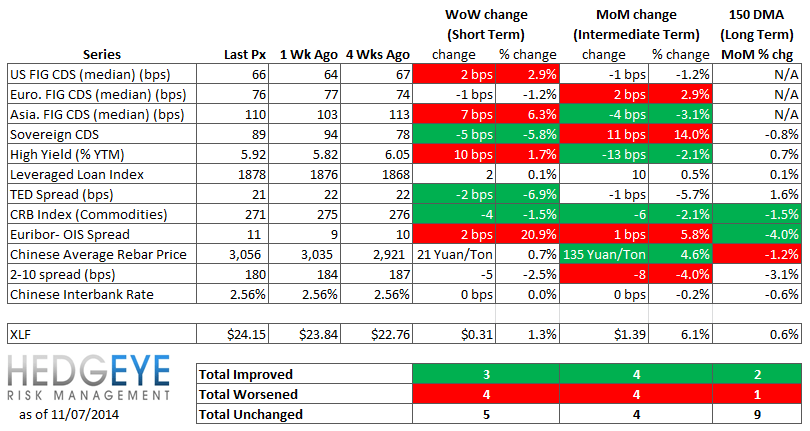

The XLF tacked on another +1.3% gain last week, bringing the month-over-month change to +6.1%. Most of the risk landscape showed little change on the week. High yield backed up 10 bps to 5.92% but remains lower on the month by 13 bps. Commodities continued their downward slide, as the CRB Index shed another 1.5% on the week. The big mover among US CDS was Genworth. Genworth swaps rose 247 bps w/w to 406 bps on the announcement that a review of its claims reserves and goodwill would result in a combined charge of over a billion dollars pre-tax.

Looking ahead, there's a roughly even mix of red/green on our heat map snapshot table below across the three different durations. On the plus side, the labor market continues to show steady progress and expectations are rising that we could finally be nearing a point where labor market slack is low enough for wage inflation to take hold. This is the factor that turns the Fed from dovish to hawkish on rates in a post-QE world. Second, the Fed just released its 4Q14 Senior Loan Officer Survey, which showed no inflection in the prevailing trends: loan spreads and underwriting standards are both still easing, on the margin, and borrowers continue to show increased loan demand. Inflections in these indicators have historically led or coincided with turning points in the credit cycle.

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 3 of 12 improved / 4 out of 12 worsened / 5 of 12 unchanged

• Intermediate-term(WoW): Negative / 4 of 12 improved / 4 out of 12 worsened / 4 of 12 unchanged

• Long-term(WoW): Positive / 2 of 12 improved / 1 out of 12 worsened / 9 of 12 unchanged

1. U.S. Financial CDS - Swaps widened for 16 out of 27 domestic financial institutions. Genworth (GNW) was the big mover on the week, where swaps rose 247 bps w/w to 406 bps. The news reflects the company's announcement that it conducted a review of its Active Life Reserves and found them to be deficient by $531mn pre-tax. On top of that, the company simultaneously revealed that a similar review of its goodwill found the need to recognize an impairment of $517mn. The stock dropped ~40% from $14 to $8.40 on the news.

Tightened the most WoW: COF, ACE, MMC

Widened the most WoW: GNW, PRU, CB

Tightened the most WoW: TRV, CB, MTG

Widened the most MoM: GNW, MET, PRU

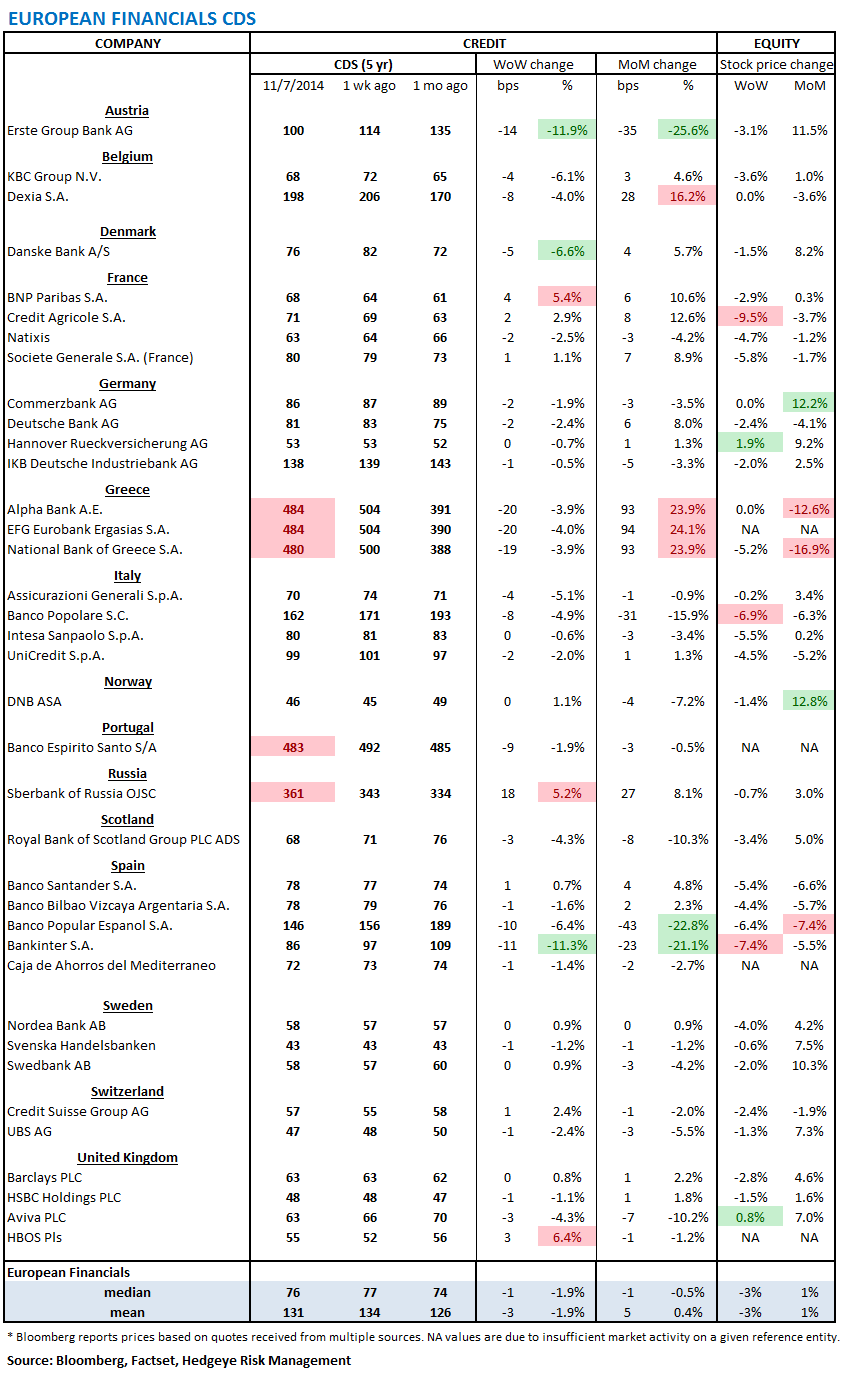

2. European Financial CDS - Swaps mostly tightened in Europe last week though were little changed on balance. In fact, on both a w/w and m/m basis EU bank swaps show little change at the moment. The stocks have been a bit more volatile as the average (and median) stock price change was down 3% for the week.

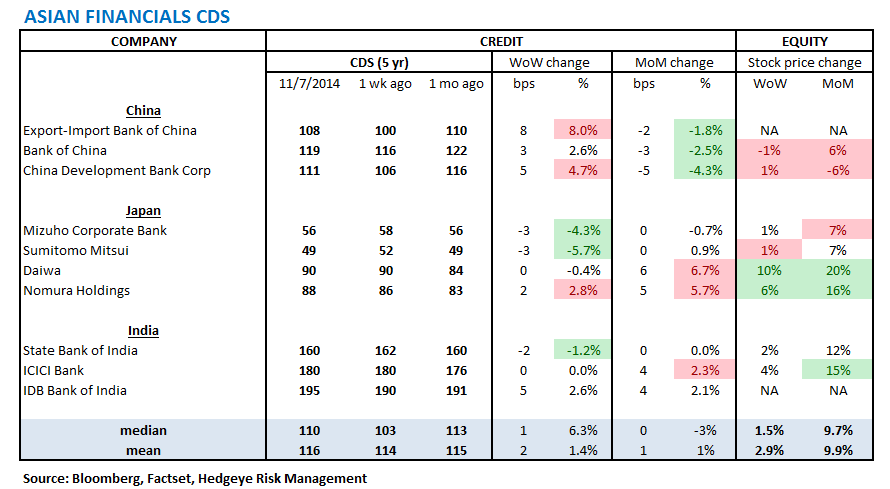

3. Asian Financial CDS - Chinese bank swaps were wider on the week by an average of 5 bps, but remain modestly tighter on a m/m basis. Elsewhere in Asia, bank swaps were little changed.

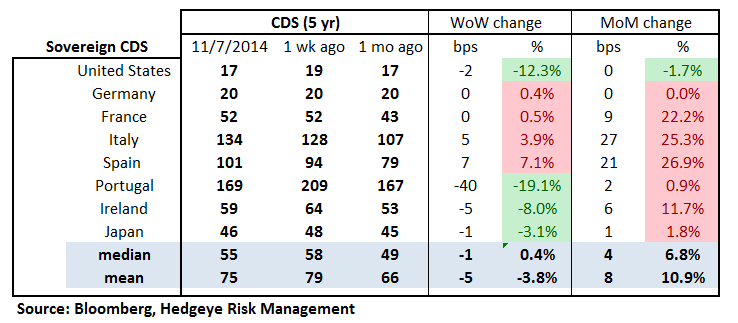

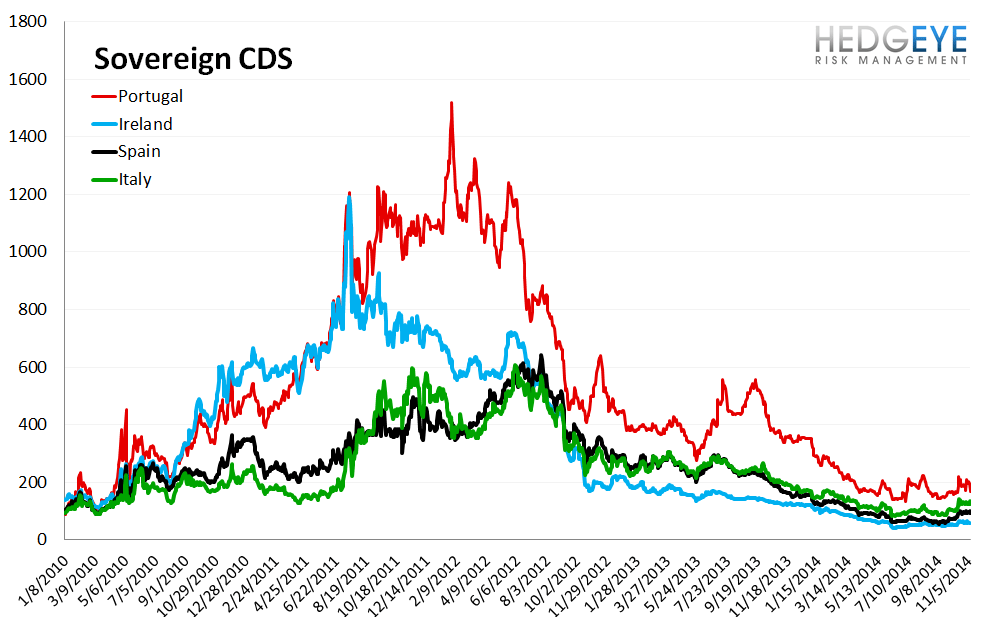

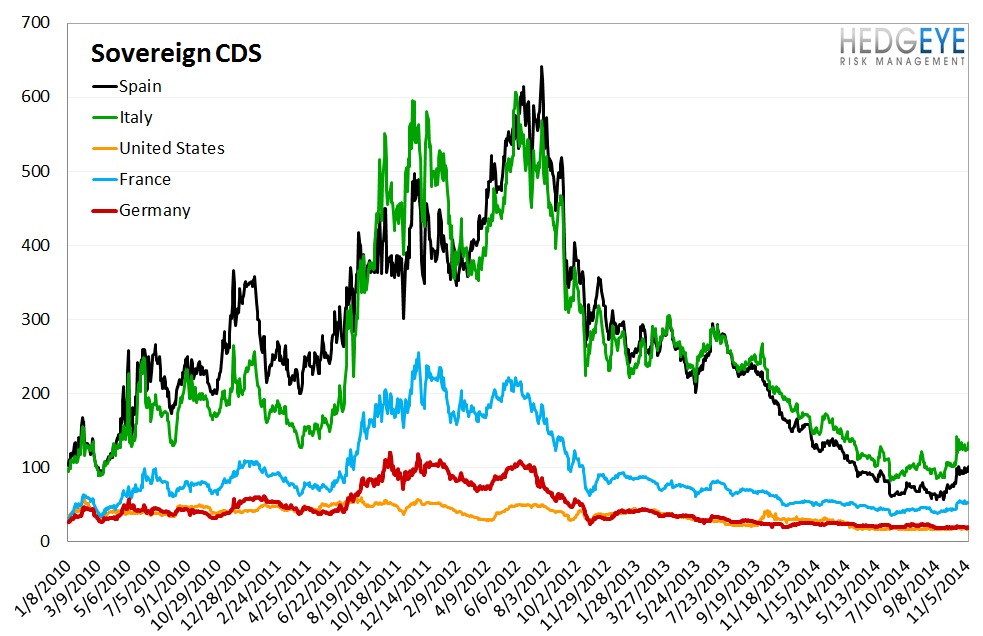

4. Sovereign CDS – Sovereign swaps were mixed on the week with Portuguese swaps tightening 40 bps to 169 bps while Spanish swaps widened by 7 bps to 101 bps.

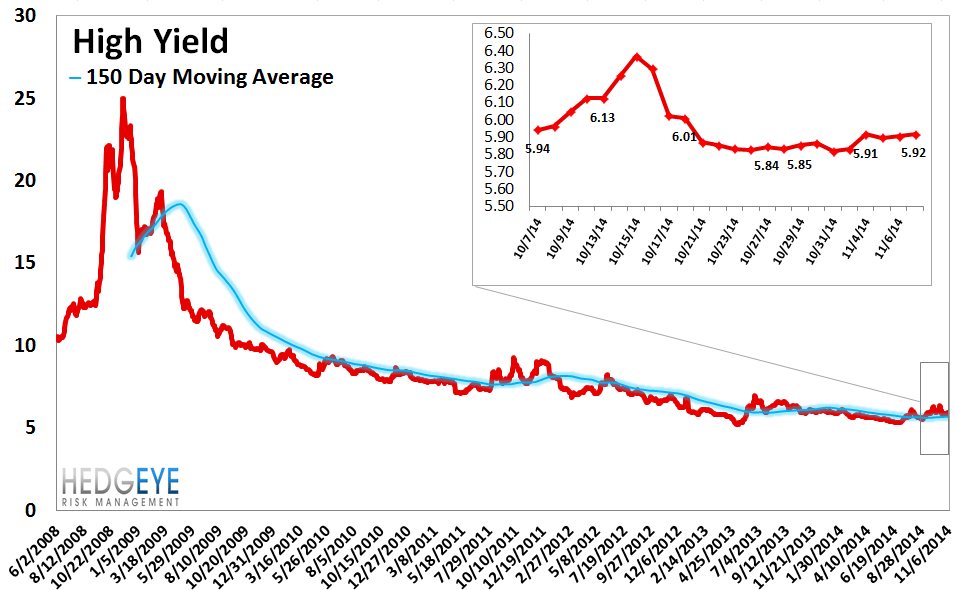

5. High Yield (YTM) Monitor – High Yield rates rose 10.1 bps last week, ending the week at 5.92% versus 5.82% the prior week.

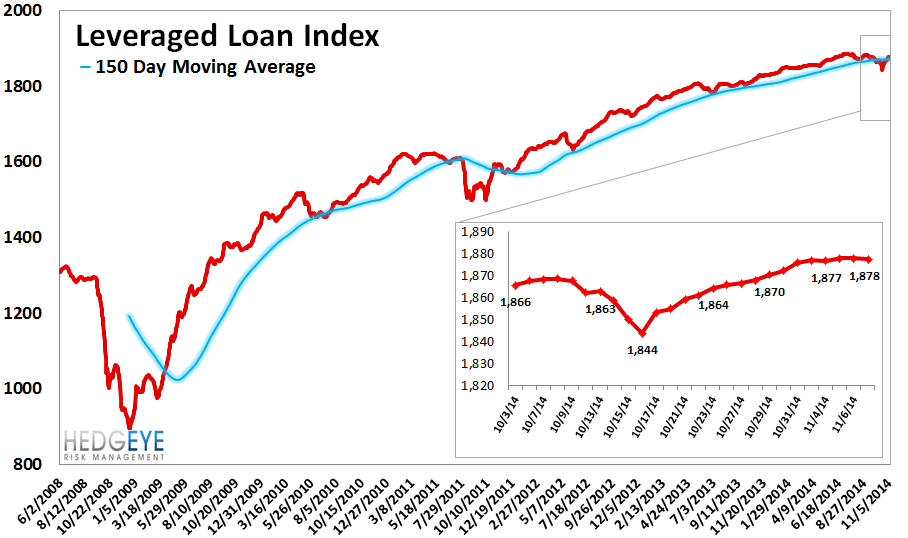

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 2.0 points last week, ending at 1878.

7. TED Spread Monitor – The TED spread fell 1.5 basis points last week, ending the week at 20.9 bps this week versus last week’s print of 22.41 bps.

8. CRB Commodity Price Index – The CRB index fell -1.5%, ending the week at 271 versus 275 the prior week. As compared with the prior month, commodity prices have decreased -2.1% We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

9. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 2 bps to 11 bps.

10. Chinese Interbank Rate (Shifon Index) – The Shifon Index was unchanged at 2.56% last week. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

11. Chinese Steel – Steel prices in China rose 0.7% last week, or 21 yuan/ton, to 3056 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

12. 2-10 Spread – Last week the 2-10 spread tightened to 180 bps, -5 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

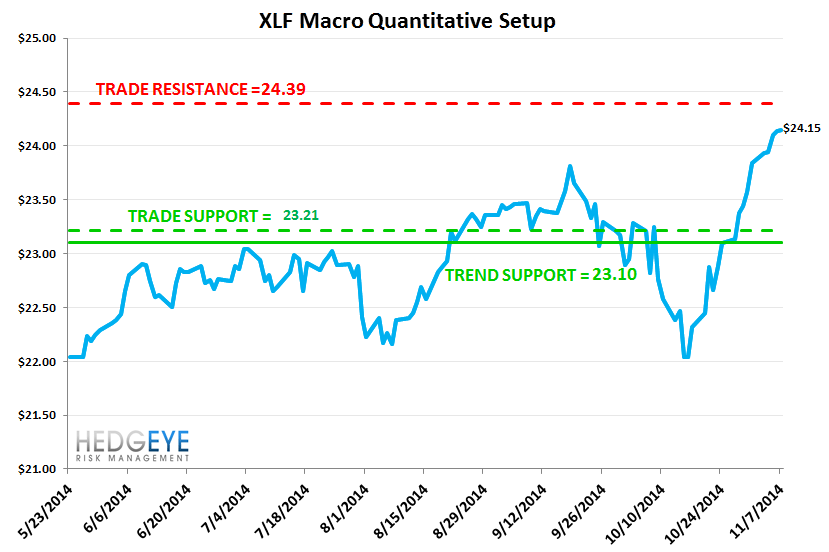

13. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 1.0% upside to TRADE resistance and 3.9% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT