Below are Hedgeye analysts’ latest updates on our seven current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

*Please note we added HCA on Friday. We will be sending out a brief report outlining our bullish rationale in the upcoming week.

*We also feature two pieces of content from our research team at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

#BurningCurrency

This central planning currency burning party is going to get really ugly.

IDEAS UPDATES

TLT | EDV | XLP | MUB

Bonds Finish a Tough Week Like Champs

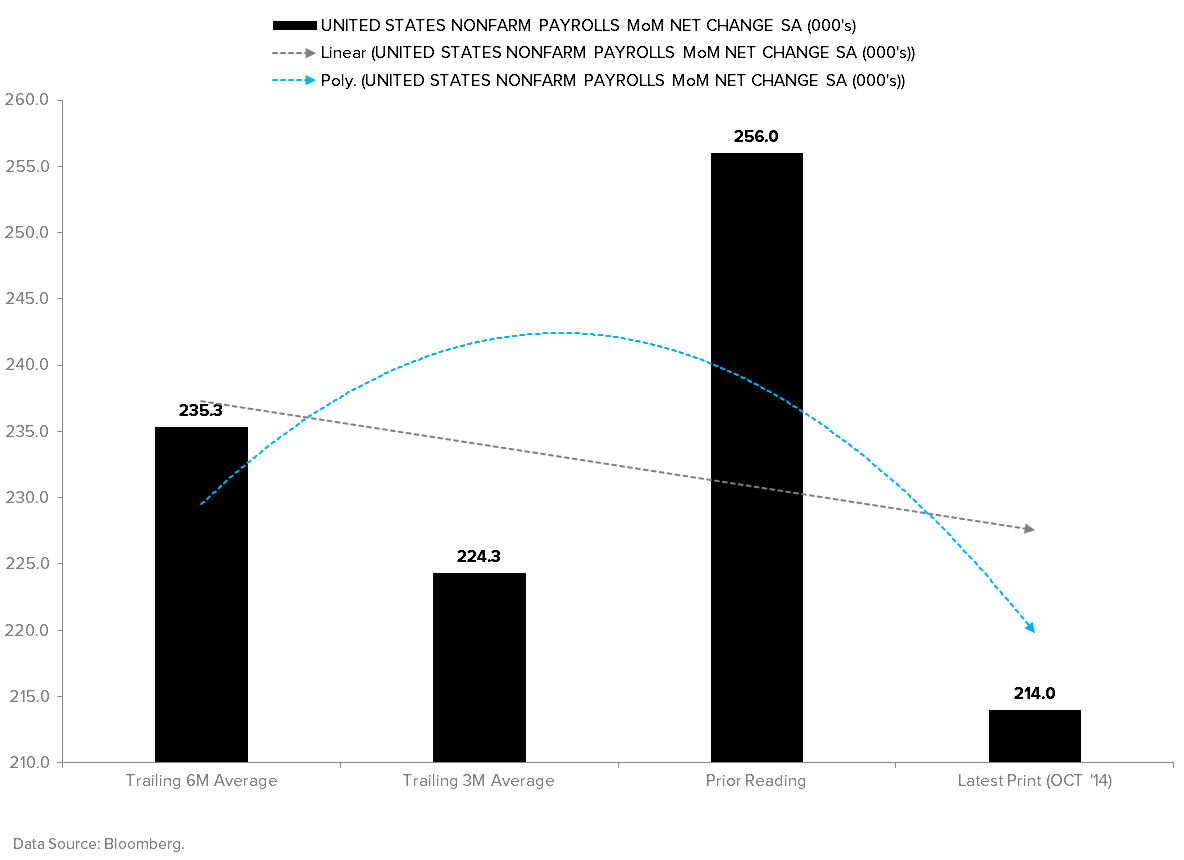

Thank goodness the midterm election came and went; fortuitously for bond investors, this allowed the government to finally stop fudging the growth data. Today was the most important day in that regard, with the OCT Jobs Report being the key economic release:

- Net payroll gains slowed sequentially to +214k MoM from an upwardly revised +256k in SEP… Good number, but has the trend of improvement inflected?

- The YoY growth rate was essentially flat at +1.9% and holding at the peak level seen in the last cycle… Is this as good as it gets? Is the economic cycle cresting?

- Private payrolls slowed sequentially to +209k MoM from an upwardly revised +244k in SEP... Much like the headline number, growth in private payrolls slowed on a 3MMA and 6MMA basis as well.

As it relates to the timing of an interest rate hike out of the FOMC – which we all know may never actually occur – the only thing that spooks the Fed into pushing out its “dots” more quickly than a -10% draw-down in the SPY is a deteriorating labor market. It’s important to contextualize the labor market properly in this regard (per Christian Drake, our senior U.S. economist):

- The unemployment rate ticked down to 5.8% and the U-6 rate declined to 11.5%, dropping the most in 7-months.

- Alongside the decline in the U-6 rate, the share of ST unemployed continues to rise, the trend in NFIB’s Jobs Hard to Fill and Compensation Indices remain positive, and available workers per job opening is back to pre-recession averages.

- The employment-to-population ratio for 25-34 year olds ticked up again as employment growth for the cohort accelerated +70bps to +3.2% YoY – the fastest rate of growth since well before the start of the Great Recession.

- Does a sequential slowdown in NFP signal a negative inflection in the domestic labor market – particularly given a negative birth-death drag, squirrely seasonals, a hard comp, declining slack and improving household survey metrics? I don’t know, but that feels like a stretched read-through on a single month of data.

Conclusion: The labor market, which is the most lagging of all economic indicators is pretty darn strong.

If for no other reason than the combination of duration (65 months into expansion) and slowing consumption growth, our work says we’re nearing the peak of the economic cycle and the Fed Funds Rate could be stuck at ZERO percent by the time the next recession rolls around.

So what do you do with that?

You buy bonds (TLT, EDV, MUB) and stocks that resemble bonds (XLP). All year, the bond market has sniffed this out and today was a continuation of that trend – after a difficult week performance-wise, nonetheless:

- TLT: +1.2% DoD; -1% WoW

- EDV: +1.3% DoD; -0.7% WoW

- MUB: +0.2% DoD; -0.4% WoW

- XLP: +0.4% DoD; +2.5% WoW

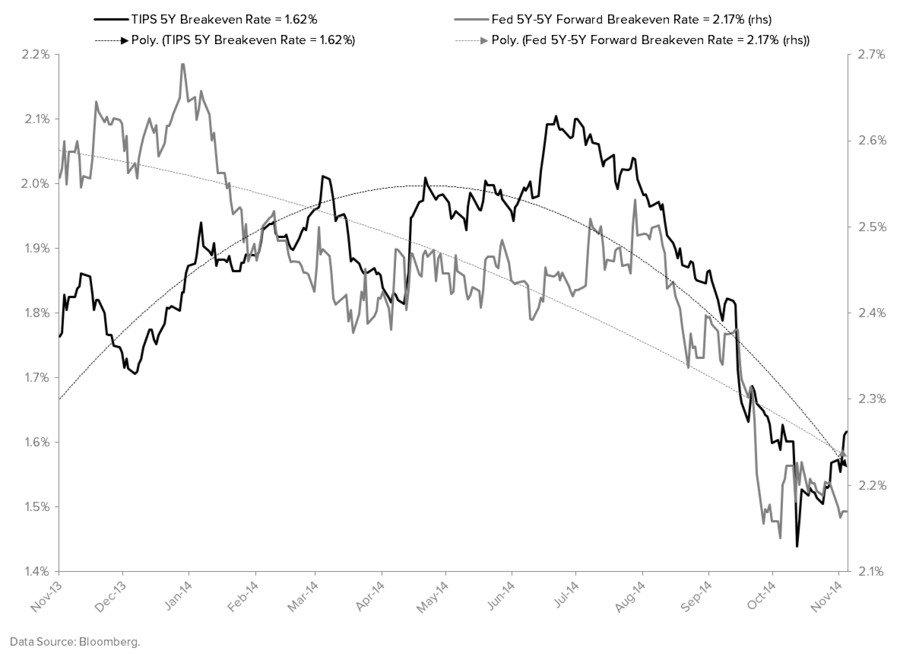

And, oh yeah, crashing oil prices aren’t exactly helping the Fed achieve its +2% “price stability” mandate either:

GLD

The follow-through from Friday’s jobs report is evidence of the market’s expectation with each growth slowing data point (Bad # = Bullish because there may be more monetary "cowbell." Everybody is doing it.)

- October Non-Farm Payrolls miss: +214K vs. +248K prior (+235K expected)

- 10-Yr -7bps back down to 2.31%

- Gold +2%

- Energy +1.3%

Real-time prices moved in a short-sighted manner with one data point moving prices in QUAD#3 fashion (GROWTH SLOWING, INFLATION ACCELERATING) manner like the first half of 2014.

As Hedgeye's U.S. macro analyst Christian Drake pointed out in his note post-report, one data point does not make a trend, and we are still positioned in a #QUAD4 deflationary set-up despite the pop in yield chasing asset classes on Friday (bonds, energy, gold):

“Does a sequential slowdown in NFP signal a negative inflection in the domestic labor market – particularly given a negative birth-death drag, squirrely seasonals, a hard comp, declining slack and improving household survey metrics?

I don’t know, but that feels like a stretched read-through on a single month of data.”

With the labor market showing continued signs of modest improvement as a whole, we expect a continuation in similar trends to support the Fed’s current policy path.

We look at activity in every market over multiple durations, and Gold is no different. The intermediate-term deflationary environment domestically is certainly bad for commodities and bullish for the U.S. dollar, but we have no question monetary policy could turn right back down devaluation road over the intermediate and long-term if it was data-supported.

From a quantitative perspective gold looks exhausted to the downside and found support at the low-end of the risk range Friday. We’ll watch the follow-through into next week.

RH

Restoration Hardware is on track to open the first Full Line Design Gallery in Atlanta on November 21st. At 45,000 selling sq. ft. (with an additional 20,000 sq. ft.) of outdoor selling space, it will be the biggest RH store to date. The new 6 story store will have an increased SKU count across it’s traditional categories and two dedicated floors, one to Small Spaces and the other to Baby and Child.

Product diversification is key to the RH story, as new categories generally experience a 50%-150% lift in sales across channels (both in stores and online) when displayed within a company’s retail locations.

But this isn’t just about the top line. One of the key components of the real estate transformation is the occupancy leverage the company realizes as it moves into spaces 6x-8x the size of its legacy stores at rent terms just 25% of the current rate per square foot. This is the big driver behind the Gross Margin expansion we should see over the next 5 years.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

CAT: 5 Reasons to Stay Bearish into 2015

"There are more than five reasons (on Caterpillar)," writes Hedgeye Industrials analyst Jay Van Sciver. "But we will start with these."

Putin on the brink? Top Russia Insider Discusses developments, what may occur next in moscow

Our Macro Team hosted a special “Behind the Curtain” conference call with Michael McFaul, one of the world’s foremost experts on Russia and Vladimir Putin. Until earlier this year, McFaul was the U.S. Ambassador to Russia and held closed-door meetings with Putin and his top lieutenants before finally stepping down out of concern for his family and his own safety.