This note was originally published at 8am on October 24, 2014 for Hedgeye subscribers.

“The problem with the big focus on making capital cheaper… is it’s akin to fighting fire with fire.”

-Dan Alpert

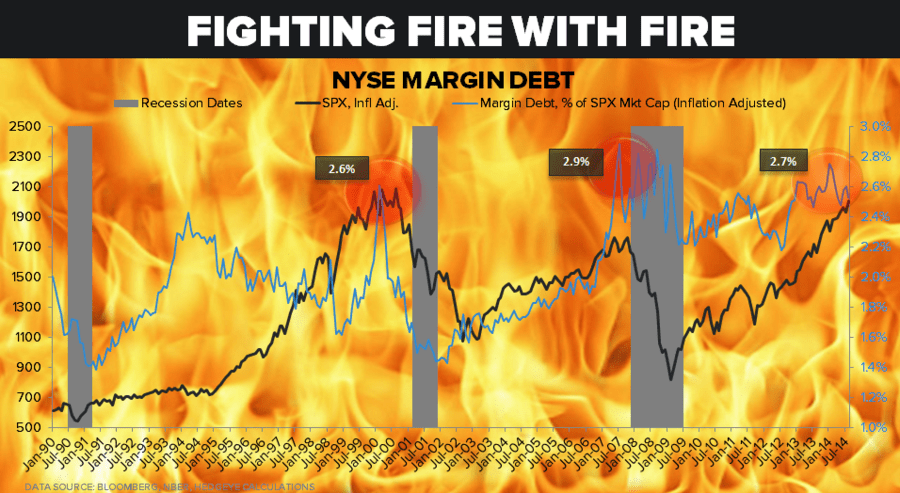

That’s a quote from the beginning of chapter 6 of The Age of Oversupply, by Dan Alpert. The chapter was a good one titled “The Empty Toolbox” and it focuses on why central planners “can’t fix the economy.” #agreed

Whether you are looking at the US economy or global one slowing right now, it’s important to keep these v-bottom moves in equity markets in context. Where are they v-bottoming from? Oh, and why did they go down so hard so that they could v-bottom to begin with?

Our call throughout the year has been very consistent on the why – growth is slowing. And when early-cycle growth slows from multi-year highs, you short the most illiquid form of beta chasing (small cap stocks) and you buy the Long Bond.

Back to the Global Macro Grind…

I was at a dinner meeting in Maine last night and an entrepreneurial CEO asked me a question I’ve been asked by hundreds of non-Wall Street people in 2014: “What do you think I should do with my money right now?”

I’m not the beat-around-the-bush-type, so I told her exactly what I have been telling people all year:

- Sell stocks

- Buy bonds

- Raise Cash

As basic as this advice has been is as hard as it’s been for people to just execute on it. But, with the total return of the Long Bond (TLT) at almost +19% for 2014 (vs. the Russell 2000 down -4%), why is that?

A: It’s not what “everyone” is saying people should be doing.

That’s it. From New Hampshire to California and everywhere I’ve been this year in between. That pretty much sums it up. The response is always the same: “but can’t interest rates go up? Aren’t bonds expensive?”

What’s been really expensive is believing that central planners can bend gravity and deliver +3-4% economic growth. If they deliver 0-2%, “expensive” bonds are going to get more expensive, and really expensive growth stocks (think Amazon at 112x earnings) are going to continue to crash.

But, but… “Keith, this bounce is crazy – why can’t it keep going…”

If I have some iteration of that in my inbox 100x in the last 3-4 market days, I have it 1,000x. And all I do is shake my head wondering why so many refuse to take a lesson from the risk management exercise learned as the Russell was having a -15% draw-down and the 10yr broke 2% only a week ago.

To review the #Quad4 deflation case that Mr. Market is effectively yelling right now:

- Bond Yields (10-30yr) in the US are crashing

- Oil prices are crashing

- Over 60% of stocks in the Russell 2000 are crashing

To be fair, if you didn’t have a view that all of these things would go down, you blamed ebola (and Canada) and wore them the whole way down anyway. But, if you did, you are killing it YTD and in a position to re-ramp every position you’ve had throughout the last 6 weeks of macro market volatility.

We’re deep into 2014 and at this stage of the season playing this game from a position of strength is entirely different than playing it from a position of weakness. If you’ve been winning, you don’t have to spend your entire day worrying about why the stock market is bouncing and bonds correcting.

You’ve realized that the Fed, Bank of Japan, and European Central bank have all cut to zero. You’ve also reminded yourself that 0 + 0 doesn’t equal something greater than zero – and that they can’t solve for #GrowthSlowing again.

In other words, they can’t fix this. Unfortunately, only a deflationary reset can.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets – which you can get in our Daily Trading Range product as well) are now:

UST 10yr Yield 2.11-2.32% (bearish)

SPX 1835-1963 (bearish)

RUT 1040-1127 (bearish)

Nikkei 14503-15449 (bearish)

VIX 15.06-28.49 (bullish)

USD 85.01-86.20 (bullish)

EUR/USD 1.26-1.28 (bearish)

Yen 105.36-108.31 (neutral)

WTI Oil 79.75-82.62 (bearish)

Natural Gas 3.51-3.74 (bearish)

Gold 1226-1251 (bullish)

Copper 2.95-3.05 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer