We thought slow foot traffic early in the month was indicative of a softer month than Aug as Macau headed into the holiday filled October. However, VIP, high end Mass, and high hold percentages are contributing to a strong Sep.

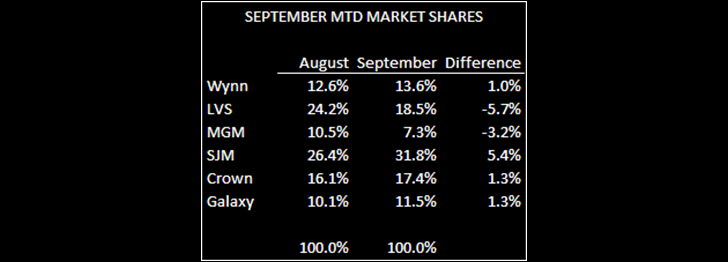

Following a casino walk through on 9/10/09, my Macau guys reported slow foot traffic. Apparently, Mass business has picked up considerably - especially over the last two weekends - while VIP has been very strong all month. Through 9/20 the month was up about 60% in year-over-year revenues according to reports out of Macau, off of an easy comparison. Mass is definitely strong but it looks like most of the gain is coming from VIP, as can be seen by our estimated market shares in the following table. We are also hearing that hold percentage is high so far versus a low hold percentage in September 2008.

SJM, Crown, and Galaxy, all VIP houses, increased market share while LVS (the bigest market share loser) and MGM lost share. The rest of the month will probably be slow given the proximity to the holidays in October, including the 60th anniversary of the communist takeover in China.