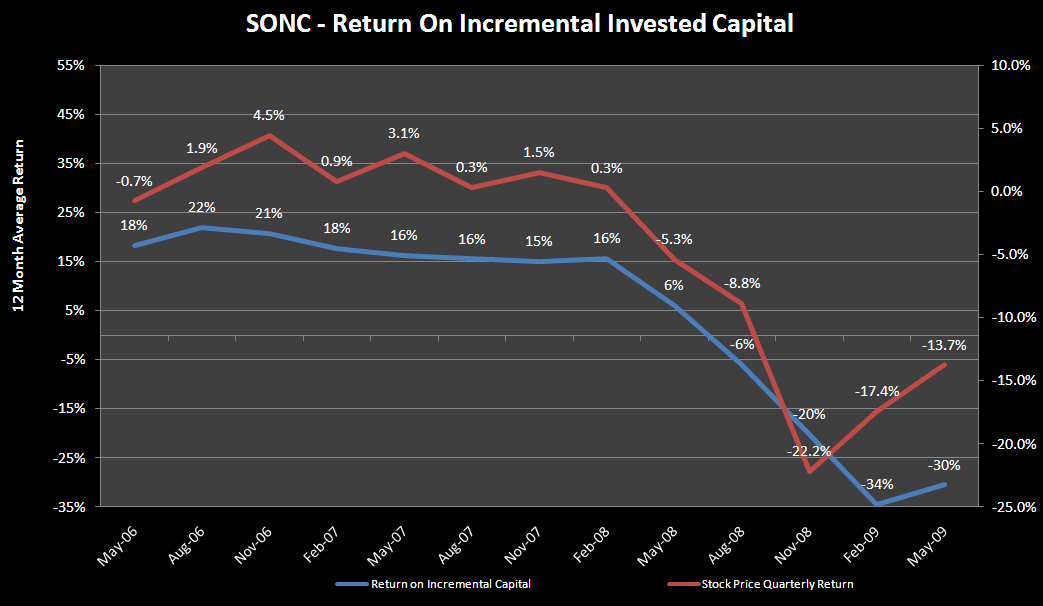

I don’t want to be out of consensus just to be out of consensus, but I like SONC. Following the cash flow has always been a great way to make money in the restaurant sector and I have used ROIIC as a successful metric to see how cash is deployed and to look deeper into the company’s long-term strategy.

For years SONC had a very enviable business model and to a certain degree, still does. Complicating the company’s operational issues is the leveraged recap done a few years back, which has handicapped the company during this difficult time. Given all that management is doing to improve operations, I see SONC as a company closer to seeing a shift on the margin toward better profitability. Competitive issues are a risk, but it could be reason not to own any restaurant company.

REFRANCHISING WILL ADD TO RETURNS - At the beginning of fiscal 2009, SONC set out to reduce the percentage of partnership drive-ins from 20% down to 12%- 14% of the total system. There are two benefits from this (1) a refocus on improving the performance of the remaining partner drive-ins more effectively and (2) it reduces both the operational and financial risk from the business model, improving overall returns. It will reduce volatility and provide a more consistent earnings stream over time. At the end of the 3Q09, SONC had already reduced the percentage of partner drive-ins from 20% to about 14%. The 177 stores sold in the third quarter netted $50.0 million in cash, bringing the cash balance to more than $100.0 million at the end of 3Q09.

SLOWING CAPITAL SPENDING WILL ADD TO RETURNS – Between 2004 and 2007, SONC’s capital spending nearly doubled from approximately $57 million to $110 million. In fiscal 2009, SONC will end up spending about $50.0 million and the company plans to take down that level of spending even further in fiscal 2010 to $30 to $40.0 million. The increased focus on the current store base and limited spending on new stores will have a positive impact on a number of line items on the P&L, boosting profitability, margins and returns.

IMPROVED PROFITABILITY? – It’s likely that SONC will see improved restaurant level margins in fiscal 2010, which would be encouraging after five reported quarters of rather significant declines. The underlying assumption for improved margins assumes flat partner drive-in same-store sales, which implies acceleration in sales trends on a 2-year average basis. Although the company is relying on the full-year benefit of its 2009 refranchising activity and lower commodity costs to drive restaurant level margins higher, we have yet to see a recovery in SONC’s 2-year average partner drive-in comparable sales trends (though they are stabilizing). And, if the value menu continues to grow as a percent of sales, it will continue to put pressure on average check and food costs as a percent of sales, offsetting some of the YOY commodity cost favorability. Operating margins should turn positive as early as 4Q09 and stay positive in fiscal 2010 even if restaurant margins remain somewhat under pressure.

There is much more to the SONC story, but clearly management is doing everything within its control to set the company down a better path. Over time the path will reward shareholders, but in the short run the MACRO environment continues to be very challenging for every restaurant operator. On the positive side, MCD’s same-store sales growth has slowed and traffic has turned negative, which implies that MCD is not taking market share anymore. The downside risk associated with MCD’s slowing sales trends is that MCD will push harder to drive traffic, leading to an increased level of discounting from the company.

As a point of comparison I have included the same ROIIC calculation for JACK.