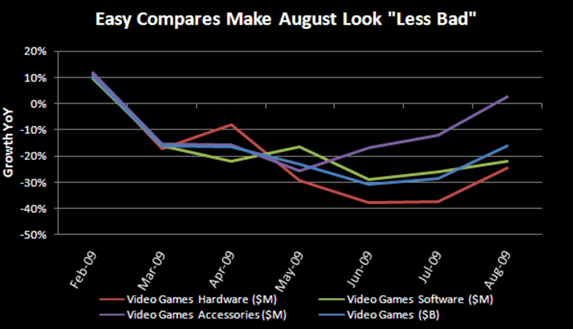

NPD released August Video Gaming results on Friday and the data looks less bad. To this I ask, "Is the consumer spending more or are easy compares providing a mirage of health that doesn't really exist?" Unfortunately, it is the later not the former and as we head into 4Q09/2010 consumer-based headwinds only get worse.

Last year, August was the slowest month of the year in terms of absolute sales data captured by NPD - $1.08Bn. This year, August data improved sequentially but it still trailed last year by a solid margin at just $0.91Bn. August marks the 3rd month this year that consumers spent less than $1Bn on the sector. The bears are claiming victory while bulls hide in their offices or point to "it's always this bad right before the cycle turns".

Where do we go from here? Frankly, I am torn. On the one hand, console price cuts are already driving some elasticity in the market and that should continue to help between now and year end. On the other, I can't help but worry about a toxic set-up that increasingly looks likely to pressure consumer spending over coming months and years.

My colleagues are among the best I've had the opportunity to work with and below are relevant excerpts from their work over the last few days. Their points are valid and surely technology-based consumer spending is not immune to these factors. Taken in this vein, it is hard to imagine that console price cuts are going to be enough to counter the mounting pressures that exist.

First, from Andrew Barber - a great post on Consumer Spending headwinds:

Keith likes to remind us that everything that matters in macro happens on the margin – and that being good at what we do means being vigilant for signs of change and that, while we invest in the present we must keep an eye on the horizon at all times. The horizon for US consumer spending looks bleak based on multiple overlapping demographic factors.

In the charts below I have illustrated two potentially peaking long-term drivers for consumer spending. In the first chart, we see the age breakout of the work force estimated by the Department of Labor. The imprint of the baby boom is clearly seen, cresting in successive peaks roughly a decade apart.

The second chart shows the long term view of US consumer leverage. The Federal Reserve reported Tuesday that consumer credit declined in July by a larger-than-anticipated $21.6 billion from June, the most on records dating to 1943. In the midst of the great recession it’s clear that consumers are accessing fewer loans (whether by design or because of reluctant lenders) and spending less.

Taken in unison, the two illustrations indicate an easy to understand trend for the coming years: the number of people in the US labor force who are at optimal earning age has peaked and will be steadily decreasing while, simultaneously, consumer credit is declining. If you combine this long tails data with the points we hammered on in our unemployment post on Wednesday (“Stagflation: Where the Pain is”) in which we discussed how current unemployment trends were being felt most heavily by the oldest and youngest components of the work force, the picture becomes increasingly grim. Not only are there fewer young people entering the work force, they are having difficulty finding employment and when laid off are taking much longer to find new positions.

As Todd Jordan pointed out in a recent post on gaming industry trends, prior to the consumer downturn beginning in the fall 2008 personal consumption expenditures were on a steep twenty-year incline. With consumer spending accounting for roughly 70% of GDP the implication is clear: the higher one goes, the more pertinent gravity becomes and keeping rates at zero or buying clunkers can only delay the inevitable. Gravity always wins.

Second, a related and especially well-written piece by Todd Jordan:

“The better part of valor is discretion”

– William Shakespeare

Thanks Bill, and the better or necessary part of consumer spending is the staples. Necessity is why staples are also called non-discretionary. With their discretion, will consumers be so valorous as to empty their wallets for things they want, rather than need? The almost vertical trajectory of discretionary consumer stocks suggests yes. On the contrary, sound analysis indicates that consumers face an almost impenetrable ceiling, triple fortified by the Three S’s: Savings rate, Stagflation, and Share of wallet. I’d add consumer credit (bad) to the mix but it doesn’t begin with an S, we like 3s, and our macro team will be addressing this topic shortly.

So while Geithner may say that “things are better than 3 months ago, 6 months ago, before this recession began”, I would ask two questions: By what metric and for whom? Geithner’s preferred metric lately, it appears, is the rate of change or the “less bad” thesis that Research Edge was espousing when everyone else thought the world was falling apart (March 9th ring a bell?). The stock market has already discounted “less bad”, then “stability”, and now is viewing the consumer as in “recovery” mode. This is what scares me.

“Recovery mode” implies, well…recovery. I’m certainly not seeing it in the consumer discretionary sectors of gaming, lodging, and leisure that comprise my analytical vertical. Is business less bad? Maybe, but I think the comparisons are just getting easier. The consumer is not necessarily getting stronger.

“Recovery mode” also implies some lasting duration. We are very worried about Q4 from a macro and consumer perspective. The threat of stagflation is real, maybe coming as soon as Q4. Stagflation is a consumer killer. In a stagflation environment, fewer consumers have jobs and the ones that do can’t buy as much as before. Will you take credit for that too, Mr. Geithner, when it happens? Your policies and your predecessor’s policies (as well as the Bernanke constant) have created a fertile environment for potentially massive inflation, yet unemployment continues to grow. Sure unemployment is growing at a slower rate (10% but it could’ve been 10.5%!). Congratulations - pop the champagne – at least the French consumer discretionary industry will benefit.

So if I’m out of work (thankfully I’m not) and my purchasing power begins to decline at an accelerating rate (rate of change cuts both ways Tim), am I really going to buy that 2nd boat, 8th Coach bag, or book that 3rd cruise this year, or will I feed my family. Want versus need.

This also gets us to the share of the wallet question. In an inflationary economy, a larger part of consumer spending will go to non-discretionary items. With stagflation, the size of the wallet shrinks. One of my industries has a third problem: even within the consumer discretionary segment, casino spending is shrinking as a % of Personal Consumption Expenditures (PCE) for the first time in 25 years. Now that’s a triple whammy!

So what do we do? Be careful and manage risk. We can’t ignore the warning signs just because the stock market and consumer stocks are going up. Timing, as always, is critical. This is where I defer to our timing tutor, Keith McCullough.

Conclusion: Both of these pieces are thoughtful and proactive given recent stock market performance. As bullish as I am on Technology, consumer-based headwinds are not something to ignore. And as it relates to video-gaming spend in particular, I like the secular shifts transforming the group, but even I must admit that spending on games is pure want versus need.