Handicapping Tomorrow

Two months ago we published a report (link) in conjunction with our Macro Team that looked at the predictive power of the ADP report at handicapping the NFP report. In a nutshell, roughly two-thirds of the time the directional move in ADP (i.e. better or worse sequentially) predicts the directional move in NFP. This creates an interesting opportunity in months when ADP goes one way and expectations are for NFP to go the other way. Tomorrow's NFP report represents such a set-up. ADP rose to 230k this month from 213k last month. Meanwhile, expectations are for NFP to shrink from 248k last month to 240k this month. Given that the move in ADP wasn't huge and the expectations for sequential deceleration in NFP aren't profound we wouldn't make too much of the divergence, but given how sensitive Financials are to labor figures, we feel it's worth pointing out.

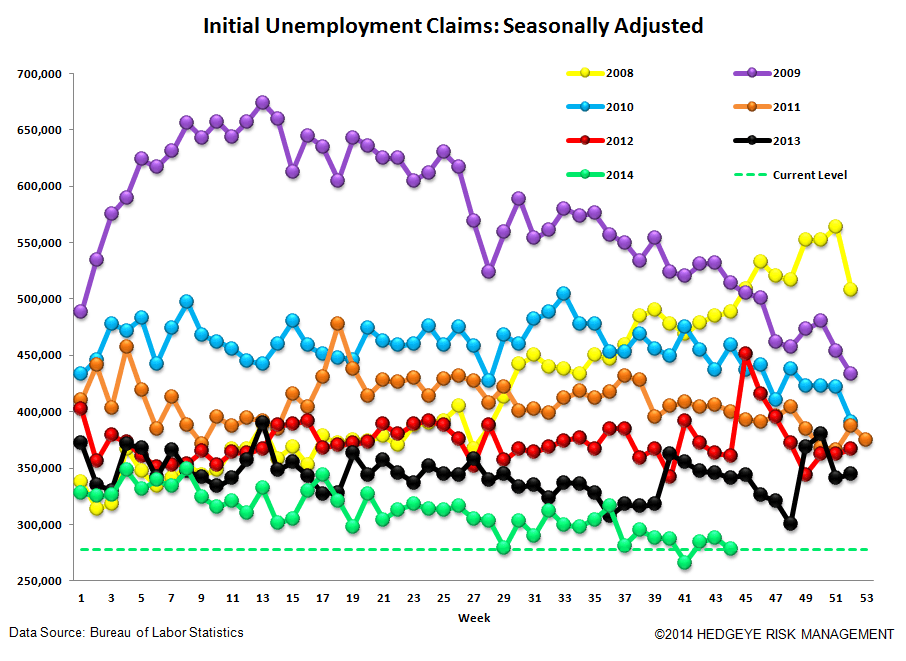

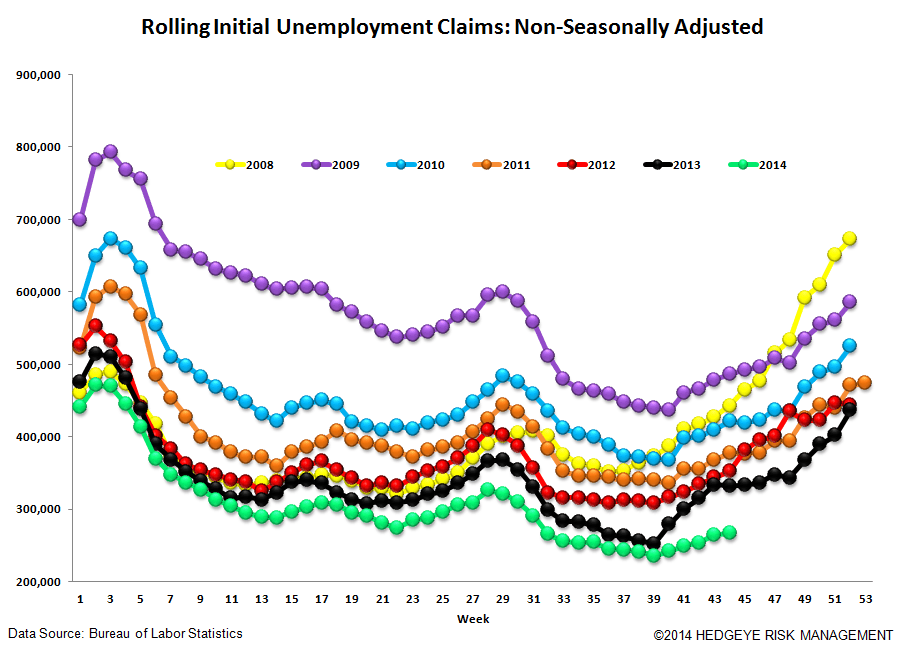

In other news, initial jobless claims remains a juggernaut of sorts. Claims continue to put in new lows and are now at levels below those seen at the apex of the 2005/2006 economic expansion.

We'll leave you with the chart below, which shows both how strong the environment is today but also how risky.

The Data

Prior to revision, initial jobless claims fell 9k to 278k from 287k WoW, as the prior week's number was revised up by 1k to 288k.

The headline (unrevised) number shows claims were lower by 10k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -2.25k WoW to 279k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -19.8% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -20.6%

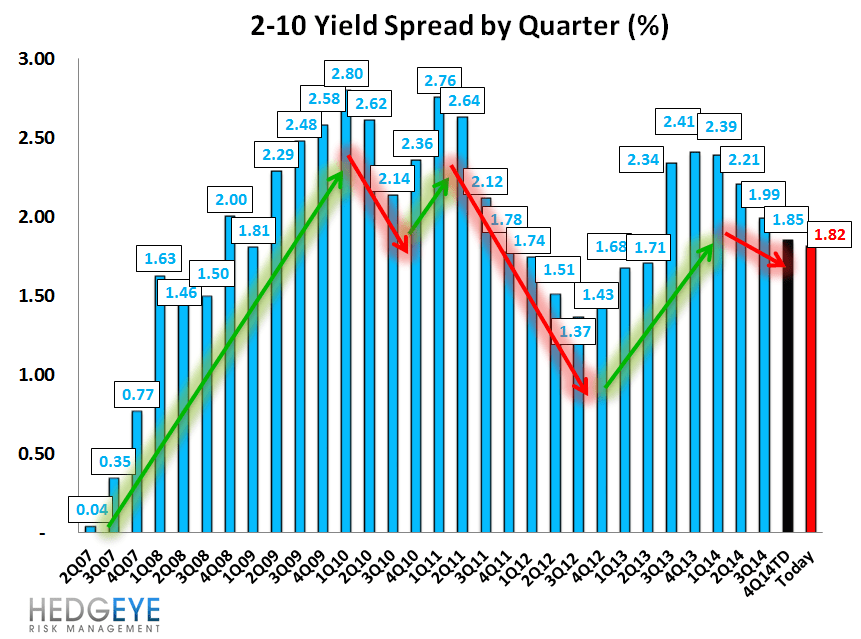

Yield Spreads

The 2-10 spread fell -1 basis points WoW to 182 bps. 4Q14TD, the 2-10 spread is averaging 185 bps, which is lower by -14 bps relative to 3Q14.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT