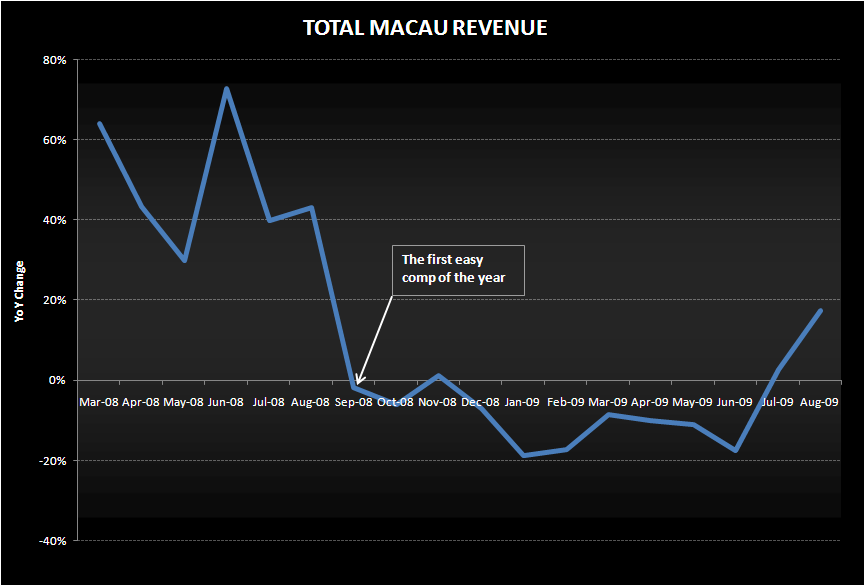

The August explosion in Macau has lifted September expectations off the charts, especially given it is the first easy comparison. Not so fast. Business has been slow so far.

My Macau guys are telling me to slow down on my September expections. Business has been surprisingly slow so far in September, nothing like August. We’re not exactly sure why yet but walk-throughs and conversations with mid-level casino employees suggest that there has been a marked slowdown in traffic, in both the Mass and VIP segments.

One explanation could be related to Hong Kong. A lot of the growth in August was from Hong Kong. You could see it at the pools which were packed in August. Chinese mainlanders don’t go to the pools. With families in back-to-school mode, the Hong Kong kicker is gone.

Another factor, as suggested by a client of mine, might be customers delaying their Macau trip until October. There are more holiday days in October of this year versus last year and, of course, the celebration of the 50th anniversary of the founding of The People's Republic of China begins October 1st.

Investor expectations are pretty high for September given the August boom, despite 40% growth last year, and the September comp is the first easy one in a long time. The volatility of the stocks to short term catalysts make this a tricky trade. September is likely to disappoint lofty expectations, but October could be a big month, although expectations are pretty high for that month already.