CHUY remains on the Hedgeye Best Ideas list as a short.

The company reported disappointing 3Q14 results yesterday after the close, as revenues and earnings fell short by 36 bps and 594 bps, respectively. Despite missing, the headline numbers were actually much stronger than the underlying fundamentals would suggest as food and labor cost pressures, in addition to select underperforming restaurants, drove restaurant level margins and operating margins lower year-over-year.

The lack of leverage in the business model is something that the street has failed to come to grips with and something we thought was blatantly obvious.

Check out the street’s prior 3Q labor cost estimate below. Estimates suggested that labor cost as a percentage of revenues would only increase 18 bps year-over-year in the quarter, after being up more than 167 bps year-over-year, on average, in the prior three quarters.

As expected, these estimates proved to be woefully misguided, as labor actually deleveraged 110 bps year-over-year in the quarter, which can be seen below.

While there was deleveraging throughout the entire P&L, labor costs were the primary reason Chuy’s missed the number in the quarter. We wanted to make this point, because it is fundamental to what drives our idea generation process. Find out where consensus is (sometimes blatantly) wrong, stress test the other line items, and then determine the ultimate impact this disconnect will have on earnings.

It’s certainly not bullet proof, but it is something that has served us extremely well. This also supports our case that Chuy’s has been the beneficiary of the Investment Banking Mafia. Take what management tells you and blindly plug it into your models.

Another issue we had heading into the quarter was the fact that the street expected underperforming restaurants in new markets to suddenly improve. This isn’t something that happens overnight. In fact, half of the restaurants in the 2013 class (which comprises 33% of the total restaurant base) continue to struggle with inefficiencies from below average AUVs.

Importantly, when you are operating a growth concept that is rapidly expanding into new markets, you need to make incremental investments in the business, meaning margins will be difficult to protect. Management has been able to leverage operating & other and general & administrative expenses in the past, but will be hard pressed to continue this trend moving forward.

As a result of the aforementioned issues, management meaningfully guided down its full-year EPS range from $0.76-0.78 to $0.67-0.69. This would imply a 4Q EPS range of $0.11-0.13, well below the street’s $0.15 estimate. Backing out the approximate $0.04 full-year accretive effect of the depreciation change management made, and probably rightfully so, apples-to-apples 2014 EPS is expected to come in between $0.63-$0.65. Chuy’s delivered $0.69 in earnings in 2013.

Before we run through bullet points of the good and the bad from the quarter, we wanted to share with you our favorite quote from the earnings call which came from CEO Steve Hislop toward the end of his prepared remarks:

“…we are working diligently to tackle what we believe are near term challenges as well as taking a thoughtful look at the evolution of our new unique model as we grow our brand nationally.”

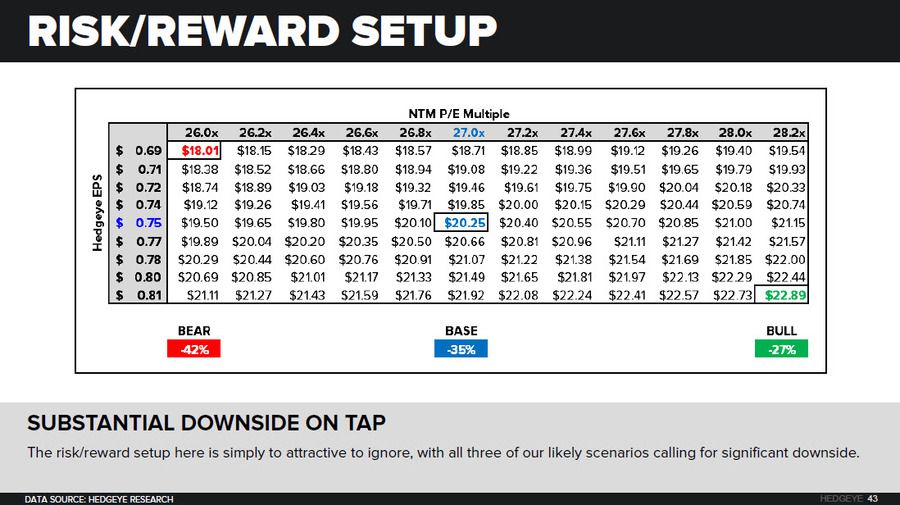

To hear this coming from the CEO of a company that is rapidly expanding nationally at a clip above 20% unit growth is concerning. At face value, at least to us, it says “we’re not ready to grow,” and the financial results of this company suggest the same. We still see significant downside to the stock and note that the company may struggle to deliver our base case $0.75 EPS next year.

The Good

- Comps +3.0% vs. +1.9% estimate; +1.3% increase in traffic; +1.7% increase in average check

- Management believes they have pricing power and could take another increase in February 2015

- Four new Chuy's restaurants opened in 3Q (2 in TX, GA, VA) and one additional in 4Q (VA); 2014 unit development is complete

- Guided up full-year comp growth from +2.3-2.6% to +2.7-2.9%

The Bad

- Guided to cost of sales as a percentage of revenue between 28.2-28.4% vs. 28.0% estimate

- Food inflation 4.5-5% for the full-year; beef, dairy, chicken, produce (lettuce, tomatoes) have been issues in 2014; chicken beginning to subside; beef, dairy likely issues in 2015 as well; only contract 25-30% of base; food cost inflation will increase, though potentially at a lower rate than in 2014

- Guided to labor costs as a percentage of revenue between 33.8-34.0% vs. 33.18% estimate

- Ongoing inefficiencies at non-comparable restaurants; comprise 33% of open restaurants

- Expect many new units to mature at lower AUVs

- New unit volumes in new markets are difficult to predict

- Guided down full-year EPS range from $0.76-0.78 to $0.67-0.69; implies a 4Q EPS range of $0.11-0.13, well below the street’s $0.15 estimate

Feel free to call, or email, with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst