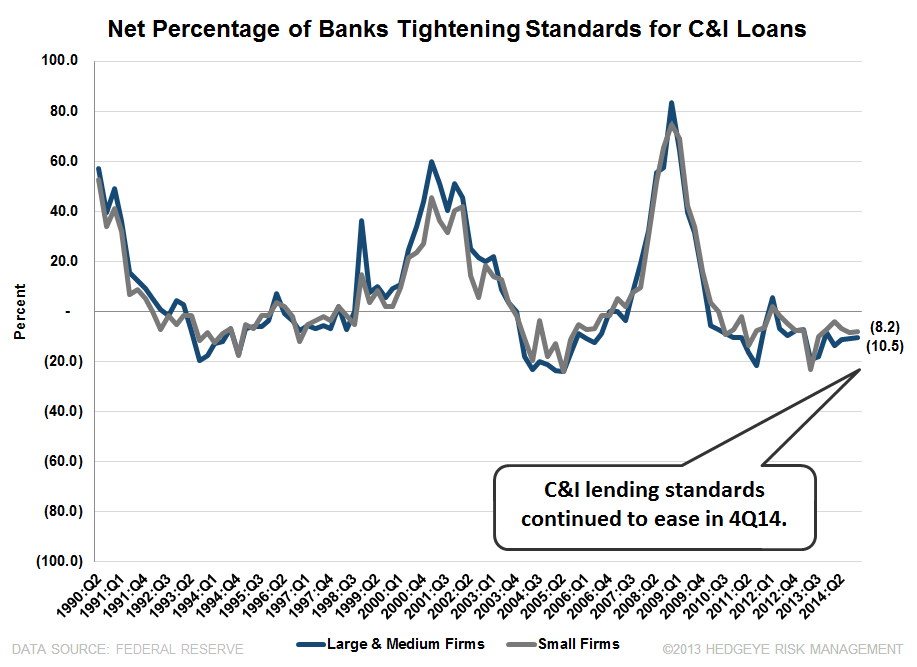

Bullish Senior Loan Officer Survey in All but One Category

The Fed released its fourth quarter Senior Loan Officer Survey yesterday afternoon. The survey covers lending standards and loan demand and was conducted between September 30th and October 14th.

Overall, the survey paints a very positive picture, though admittedly is somewhat backward looking given the survey period was 3-5 weeks ago. Across C&I and CRE loans, lending standards continued to ease while loan demand improved. On the consumer side, residential mortgage lending standards eased. Consumer non-mortgage loans saw lending standards ease again this quarter and demand strengthened again. Notably, banks willingness to make consumer loans is still increasing.

This survey suggests that the reasonably strong loan growth trends we saw from banks in 3Q14 should persist in 4Q14 barring any sharp loss of confidence intra-quarter.

Bottom Line:

The first chart below looks at the historical C&I lending standards question (LHS) juxtaposed against the price of the S&P 500 Financials subsector (RHS). C&I lending standards have historically turned tighter ahead of or coincident with peaks in Financials equity prices. We've highlighted in green the periods during which Financials stock prices are rising. in the 1 period it was clear that lending standards were tightening as early as late-1999 suggesting the top was near. In the 2003-2007 period standards were cooling steadily throughout 2006 and rolled into negative territory (i.e. standards were tightening on net) in mid-2007, about a quarter ahead of the peak in prices. As the chart shows, C&I standards are not showing any signs of rolling over through the most recent reading.

Takeaways:

There are two useful takeaways here. First, inflections in this series either lead or are coincident with turning points in Financials equity prices. Second, underwriting standards are autocorrelated, meaning they trend in the same direction for a long time before reversing. This means that once the turn begins you can ride the trend for a long time.

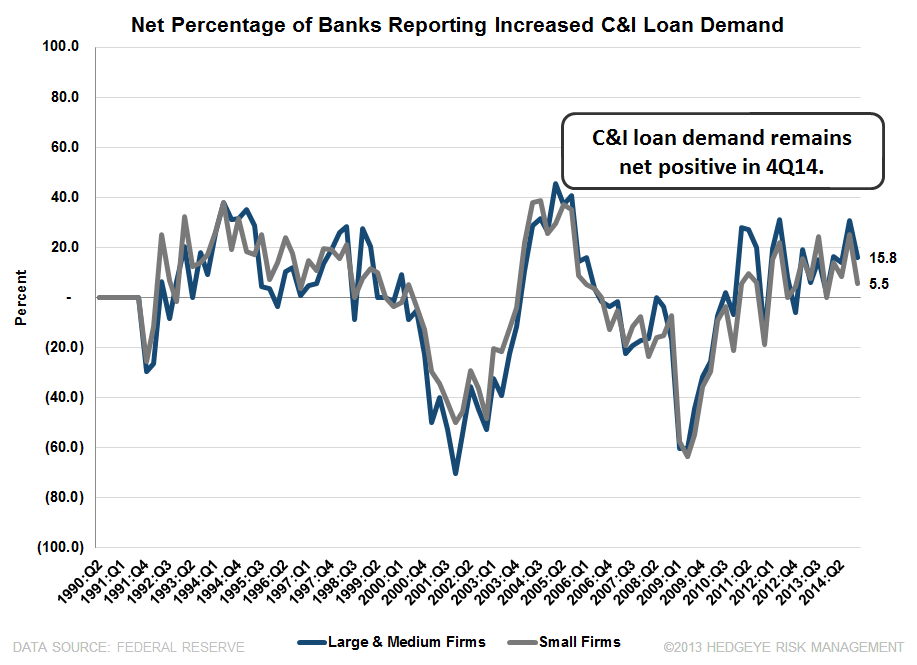

C&I Loan Tailwinds Persist: Easing Standards and Rising Demand

Demand for C&I loans continued to rise in the 4Q survey, spreads tightened, and standards continued to ease.

Notably, a net 47% of banks reported not increasing spreads for large and mid-size firms, while a net 15% of banks reported stronger demand for C&I loans among large and mid-size borrowers.

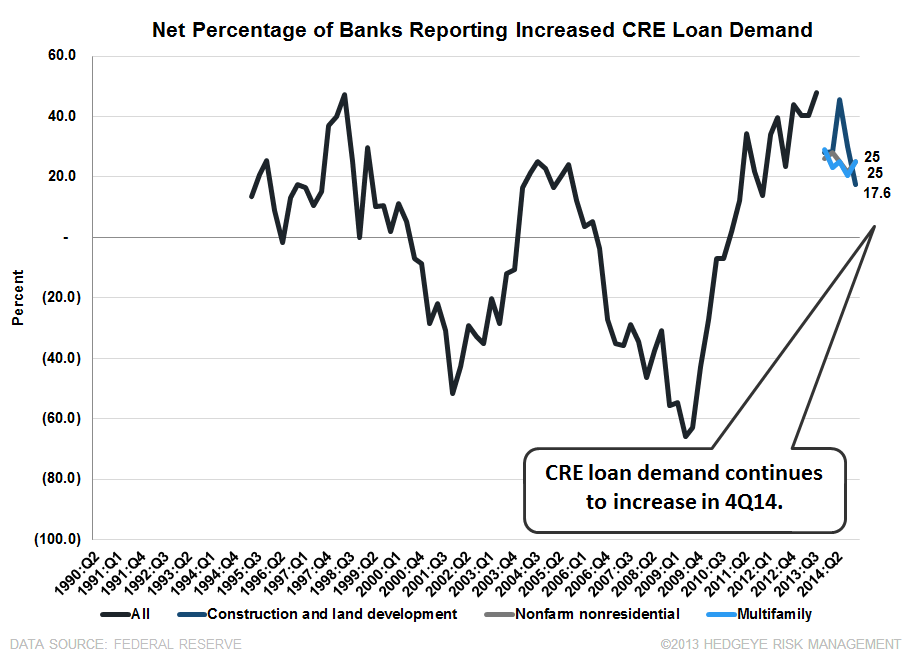

CRE Loan Demand Rises Further While Standards Continue to Ease

Commercial real estate loan demand improved in the quarter with a net 25% of banks reporting stronger demand for C&D and Nonfarm nonresidential loans. Meanwhile, a net 10.8% of banks reported easing C&D loan standards 4Q14 - the highest percentage recorded since the introduction of the C&D survey category.

Multifamily Issues

The one area of softness in the survey was that a small fraction of banks (+1.3%, net) reported tightening standards on Multifamily loans. While not a big deal in the face of all the other data, anytime a category rolls from positive to negative or the other way around we take note.

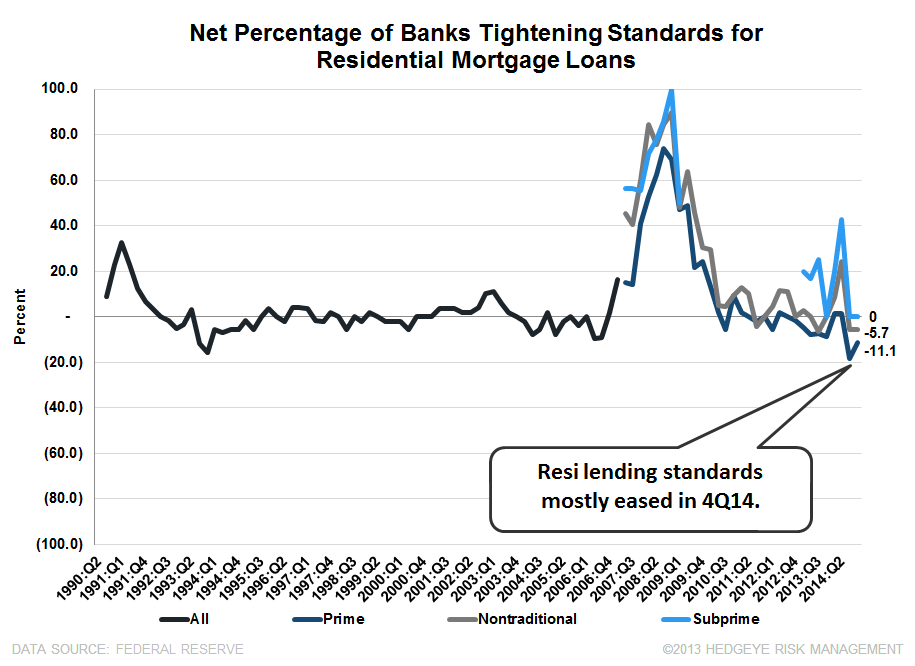

Residential Real Estate - A Mixed Picture

Residential mortgage loan standards were easier in 4Q for both prime and nontraditional borrowers. A net 11% of banks reported easing standards on prime borrowers, while a net 5% of banks reported easing standards on nontraditional borrowers.

The demand side, however, saw negative trends across the board. We consider this less meaningful because there is built-in seasonality in the purchase market (Fall/Winter home sales always drop relative to Spring/Summer) and the refi market is a direct function of rates.

Consumer Loans - Cards, Cars & Installment

Banks reported a net easing of standards for credit cards, auto loans and installment credit. This survey was roughly in-line with that of recent surveys. On the demand front, auto loans are again hot. 25% of banks, net, reported an increase in demand for auto loans. Meanwhile, demand for card and installment loans remained positive on net, but slowed a bit sequentially.

Finally, banks willingness to make consumer loans (non-mortgage loans) was a plus 8.7%, net in the fourth quarter.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT